Louisville and Jefferson County KY VA-approved condo guide for Kentucky veterans and real estate agents.

Louisville Kentucky VA Approved Condos for Jefferson County KY

If you are a Kentucky veteran, active-duty service member, or eligible surviving spouse looking at a condominium in Louisville, the first thing to confirm is simple: is the condo project acceptable for VA mortgage financing?

A VA loan can be one of the strongest mortgage programs available because it may allow qualified buyers to purchase with no down payment, no monthly private mortgage insurance, and competitive loan terms. However, condos add one extra layer of due diligence. The condominium project itself must be acceptable for VA financing before the loan can move forward smoothly.

Quick answer: Louisville veterans can use a VA loan to buy a condo in Jefferson County KY, but the condo project should be checked against VA approval records before contract, appraisal, and underwriting deadlines become an issue.

Why VA Condo Approval Matters in Kentucky

Buying a single-family home with a VA loan is usually more straightforward from a property-approval standpoint. Condos are different because the financial health, insurance coverage, ownership structure, legal documents, and management of the condominium project can affect VA eligibility.

That is why Kentucky homebuyers and real estate agents should verify the condo project early. Waiting until after the offer is accepted can create avoidable delays, especially if the condo is not already listed as approved.

VA Loan Benefits for Louisville Condo Buyers

No down payment may be required when the purchase price does not exceed the appraised value and the borrower qualifies.

No monthly private mortgage insurance is required on VA loans.

Seller-paid closing costs and concessions may help reduce cash needed to close.

VA loans may be more forgiving than conventional financing for qualified veterans, depending on credit, income, residual income, and overall risk profile.

VA eligibility can be used more than once, subject to entitlement and VA guidelines.

Before writing an offer on a condo, verify the project using the VA condo report or have your lender check it for you. The official VA condo report can be accessed here: VA Condo Report Search.

The list below is based on the Jefferson County KY VA-approved condo results provided for Louisville-area VA mortgage loan research. Condo approval status should always be re-verified before contract, appraisal, or final loan approval because records can change.

Condo Name

VA Condo ID

Record Type

ANDERSON PARK CONDOMINIUM

000004

Condo

ARBOR CREEK CONDOMINIUMS

H00212

Condo

ARBOR CREEK CONDOS II

H00306

Condo

AUTUMN TRACE CONDOMINIUM

H00282

Condo

BAXTER PLACE CONDOMINIUMS

H00309

Condo

BRADFORD COMMONS CONDO

H00319

Condo

BRADFORD COMMONS CONDOS

000001

Condo

BRITTANY POINTE CONDOMINI

005775

Condo

BROWNSBORO VILLAGE COURT

H00398

Condo

CARRINGTON GREENE COURTYARD

000012

Condo

CHAMBERLAIN SQUARE CONDO

H00614

Condo

COPPERSHIRE CONDOMINIUM

005613

Condo

COTTONWOOD CONDOMINIUM

H00053

Condo

CREEKWOOD TERRACE

H00095

Condo

CRESCENT CONDOS

VAC028

Condo

CROSSINGS @ COOPER CHAPEL

H00155

Condo

DARNELL MANOR CONDOMINIUM

H00368

Condo

DONARD PARK CONDOMINIUMS

000003

Condo

DORSEY HILLS CONDOMINIUM

H00199

Condo

DORSEY VILLAGE

005601

Condo

EAST HAMPTON

H00693

Condo

EVERETT PLACE CONDOMINIUM

005724

Condo

EVERGREEN POINT CONDO

H00637

Condo

FOREST PARK CONDOS

H00096

Condo

FOX HOLLOW CONDOMINIUM

H00634

Condo

GARDENS AT BAY RUN CONDO

H00639

Condo

GLENVIEW EAST

005674

Condo

GRAYSTONE MANOR

H00070

Condo

HARRODS LANDING CONDOMINI

H00464

Condo

HAWTHORNE POINTE CONDOS

H00134

Condo

HIGHWOOD

H00211

Condo

HIKES PARK TOWNHOMES

H00066

Condo

HITE AVENUE GARDENS

005801

Condo

INDIAN RIDGE CONDOMINIUMS

H00358

Condo

LAKEVIEW

VAC010

Condo

MAGNOLIA PLACE

005597

Condo

MANNER POINTE

000013

Condo

MERCANTILE GALLERY LOFTS

000015

Condo

MOSS CREEK CONDOMINIUM

H00294

Condo

PARK CENTRAL

VAC101

Condo

PARK LANE CONDOMINIUM

H00179

Condo

PINNACLE GARDENS

H00111

Condo

REGENCY THREE CONDOMINIUM

005892

Condo

RIVER POINTE PATIO HOMES CONDO

000017

Condo

SALEM SQUARE CONDOMINIUM

H00067

Condo

SHELBY CROSSING CONDOMINI

H00344

Condo

SHELBY CROSSING CONDOMINIUMS

000006

Condo

SOUTH HALL CONDOMINIUMS

005723

Condo

SPRING DRIVE CONDO

005656

Condo

SPRINGS OF GLENMARY

H00217

Condo

SPRINGS OF GLENMARY VLLGE

005612

Condo

ST ANTHONY'S LANDING

H00194

Condo

STONEHENGE CONDO

005602

Condo

SWAN POINTE CONDOMINIUMS

H00586

Condo

THE CLIFF VIEW TERRACE CO

H00587

Condo

THE COTTAGES @ MEADOWVIEW

H00182

Condo

THE FOUNTAINS CONDOMINIUM

H00171

Condo

THE GARDENS OF GLENMARY

H00272

Condo

THE GARDENS OF MONTICELLO

H00609

Condo

THE PARKVIEW CONDOMINIUMS

H00258

Condo

THE VILLAGE @ WILDWOOD

H00088

Condo

THE VILLAGE @INDIAN FALLS

H00143

Condo

THE VILLAGE OF WHITE OAKS

H00531

Condo

THE VILLAS OF STONY FARM

H00288

Condo

THE WOODS OF CRESCENT HIL

H00031

Condo

THE WOODS OF CRESCENT HIL

H00030

Condo

TIMBERWOOD II

000005

Condo

TREIS CONDOMINIUMS

H00058

Condo

VALHALLA VISTA CONDOMINIUMS

000024

Condo

VALLEY FARMS PATIO HOMES

000021

Condo

VILLAGE AT PRESTON CROSSI

H00504

Condo

VILLAGE AT WILDWOOD

H00125

Condo

WEMBERLY HILL GARDEN HOME

VAC143

Condo

WESTPORT GARDENS

000008

Condo

WESTPORT RIDGE CONDO

H00629

Condo

WINDSOR GATE CONDOMINIUM

H00262

Condo

WISTERIA LANDING CONDO

H00535

Condo

WOODMONT

H00156

Condo

WOODRIDGE LAKE PATIO HMS

H00092

Condo

WOODRIDGE LAKE TOWNHOMES

H00093

Condo

WOODS OF ST. ANDREWS

H00139

Condo

WOODSPOINTE

VAC074

Condo

WORTHINGTON GLEN CONDOS

H00162

Condo

WYNDEMERE

H00213

Condo

WYSTERIA LANDING CONDOMIN

H00351

Condo

YORKWOOD CONDO I

VAC013

Condo

YORKWOOD CONDO II

VAC016

Condo

How to Use This VA Condo List

Find the condo project name in the list.

Confirm the condo ID and project status in the VA condo report.

Ask the listing agent or HOA for current condo documentation if needed.

Have the lender verify borrower eligibility, residual income, credit, assets, and occupancy.

Do not order the VA appraisal until the condo eligibility path is clear.

What If the Louisville Condo Is Not on the VA Approved List?

If a condo project is not showing as VA approved, it does not automatically mean the buyer is dead in the water. It does mean the deal needs to be reviewed carefully before you assume VA financing will work. The lender may need to determine whether the project can be submitted for VA review and whether the timeline still works for the buyer, seller, agents, and closing date.

The practical reality is simple: if the condo is already VA approved, the transaction is usually cleaner. If the condo is not already approved, the file may need more documentation, more time, and more cooperation from the HOA or management company.

Important Questions Before a Veteran Writes an Offer on a Condo

Is the condo project currently VA approved?

Does the condo name match exactly in the VA condo report?

Is the project in Jefferson County, Louisville, or another Kentucky county?

Are there pending lawsuits, insurance issues, budget problems, or high delinquency rates?

Will the HOA or management company provide documents quickly?

Does the buyer qualify for the VA loan based on income, credit, residual income, and debts?

Is the unit intended as the buyer’s primary residence?

Topical Kentucky VA Loan Resources

For more Kentucky mortgage guidance, review these related resources:

Need Help Buying a VA-Approved Condo in Louisville KY?

If you are a Kentucky veteran looking at a condo in Louisville or Jefferson County, get the condo checked before you waste time, money, or appraisal fees. I can review the condo project, your VA eligibility, credit, income, and cash-to-close numbers before you write the offer.

Frequently Asked Questions About VA Approved Condos in Louisville KY

Can I buy a condo in Louisville with a VA loan?

Yes. Eligible veterans, service members, and qualifying surviving spouses may use a VA mortgage loan to buy a condo when the borrower qualifies and the condo project is acceptable for VA financing.

Does a Louisville condo have to be VA approved?

The condo project should be checked through VA resources before relying on VA financing. If the project already appears as approved, that can help reduce the risk of loan delays.

Are FHA-approved condos automatically VA approved?

No. FHA condo approval and VA condo approval are not the same. Always verify the project through VA resources before assuming it works for a VA loan.

What are the biggest VA loan benefits for Kentucky condo buyers?

Major VA loan benefits may include no down payment, no monthly private mortgage insurance, competitive loan terms, and limited closing costs. Borrowers must still meet VA and lender requirements.

Who should verify the VA condo status?

The lender should verify the VA condo status early. Real estate agents should also confirm the project name and HOA contact information as soon as the buyer shows interest in a condo.

Joel Lobb, Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae. EVO Mortgage. Helping Kentucky Homebuyers Since 2001. NMLS #57916 | Company NMLS #1738461.

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval, VA eligibility, property approval, underwriting, and program requirements. This site is not endorsed by or affiliated with FHA, VA, USDA, KHC, or any government agency.

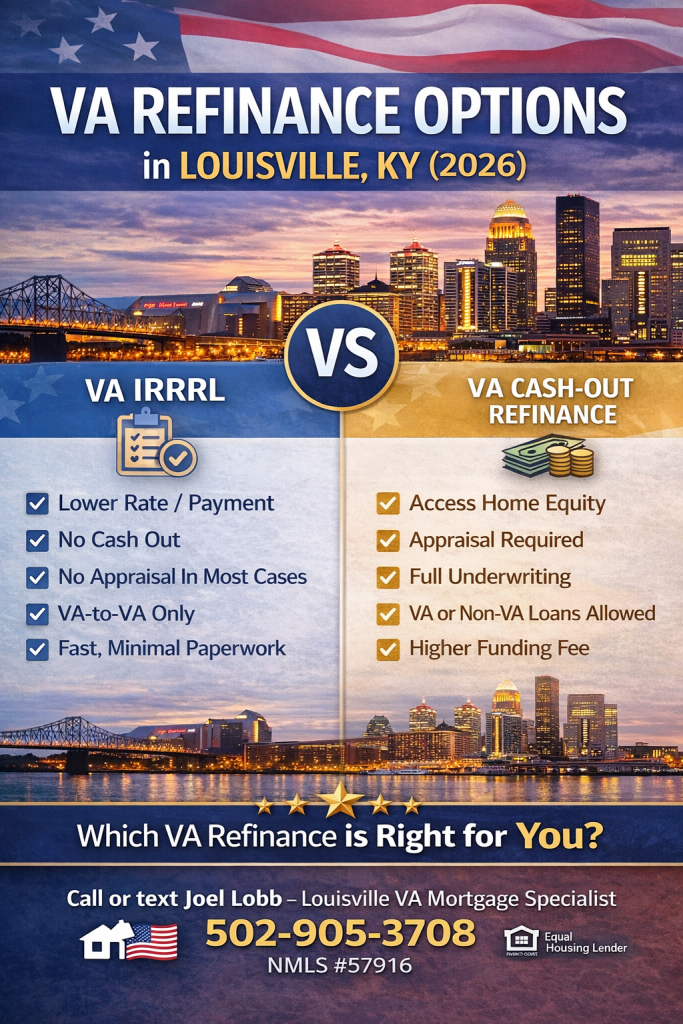

VA Refinance in Louisville Kentucky: Complete Guide to IRRRL, Cash-Out & Rate-and-Term Options

As a Kentucky mortgage lender with over 20 years of experience, I’ve helped more than 1,300 veterans and active military members refinance their VA home loans to save money, access home equity, and achieve better loan terms. If you’re a Louisville area veteran with an existing VA mortgage, understanding your refinance options could save you thousands of dollars over the life of your loan.

This comprehensive guide covers the three main VA refinance options available to Kentucky veterans: VA Interest Rate Reduction Refinance Loans (IRRRL), cash-out refinancing, and rate-and-term refinancing.

Ready to Explore Your Refinance Options?

Get a free pre-qualification and see your refinance options today. Same-day approvals on most applications.Call or Text: 502-905-3708Email: kentuckyloan@gmail.com

What is a VA Refinance Loan?

A VA refinance loan allows veterans who already have a VA mortgage to refinance their existing home loan into new terms. Unlike traditional cash-out refinancing, VA refinancing leverages your existing VA home loan entitlement, making the process faster and more affordable.

Why refinance your VA mortgage?

Lower monthly payments through reduced interest rates

Access home equity with cash-out refinancing for home improvements, debt consolidation, or other expenses

Shorter loan terms to pay off your mortgage faster

Convert ARM to fixed-rate mortgages for payment stability

Eliminate PMI with no requirement for mortgage insurance

If you’re curious about whether refinancing makes sense for your specific situation, contact me at 502-905-3708 for a free, no-obligation consultation.

Understanding VA Loan Entitlement for Refinancing

Before exploring specific refinance programs, it’s important to understand your VA loan entitlement. Your entitlement is your “eligibility” to use the VA loan benefit.

Key entitlement facts:

The basic entitlement available to each eligible veteran is $36,000

If you’ve already used your entitlement for a previous VA purchase, you can reuse it for a refinance

A Certificate of Eligibility (COE) from the VA proves you’ve used your entitlement before

Lenders can verify entitlement status without requiring a new COE in some cases

For IRRRL refinances specifically: You only need to certify that you previously occupied the home—the occupancy requirements are different from purchase loans.

Uncertain about your entitlement status? I can help you determine your eligibility and available options at no cost. Call or text 502-905-3708 or email kentuckyloan@gmail.com.

VA IRRRL Refinance (Interest Rate Reduction Refinance Loan) – The Streamline Option

The VA Interest Rate Reduction Refinance Loan (IRRRL), also called a VA streamline refinance, is the fastest and simplest way for veterans to lower their interest rate and reduce monthly payments.

How Does a VA IRRRL Streamline Refinance Work?

The IRRRL is designed specifically to refinance an existing VA-to-VA mortgage into better terms. The VA guarantees the new loan just as it did your original mortgage, which means lenders can approve IRRRLs with minimal paperwork.

The streamline advantage:

No appraisal required

No underwriting/credit check required

No Certificate of Eligibility (COE) needed (though you can provide one)

Loan can be approved in as few as 7-10 business days

All closing costs can be rolled into the new loan amount

Minimal documentation needed

IRRRL Eligibility Requirements

To qualify for a VA IRRRL streamline refinance, you must meet these basic criteria:

You already have a VA loan – The IRRRL is only for refinancing an existing VA mortgage

VA-to-VA refinance – You’re refinancing a VA loan into another VA loan (you cannot use IRRRL to refinance into a conventional or FHA loan)

You previously occupied the home – Unlike purchase loans, you don’t need to occupy the property now; you just need to certify you did in the past

Your entitlement must be available – If you’ve used your full entitlement for another property without paying off the original loan, you may have limited options

Subordination requirement: If you have a second mortgage (home equity line of credit, second lien, etc.), the holder must agree to subordinate (place) that loan below your new VA mortgage. If they won’t, the IRRRL may not be possible.

IRRRL Closing Costs & Funding Fee

One of the biggest advantages of IRRRL refinancing is the ability to do it with “no money out of pocket” by rolling all costs into the new loan amount.

Typical IRRRL costs include:

VA funding fee (reduced for IRRRL – typically 0.55% of the loan amount)

Title insurance and title search

Recording fees and transfer taxes (varies by county)

Appraisal fee (if lender requires one, though not mandatory)

Loan origination fee

VA Funding Fee Exemptions

You do NOT pay a funding fee if you are:

A veteran receiving VA compensation for a service-connected disability

A veteran entitled to receive compensation for a service-connected disability (even if receiving military retirement pay)

A surviving spouse of a veteran who died in service or from a service-connected disability

Real-world example: On a $200,000 IRRRL refinance, a typical VA funding fee of 0.55% equals $1,100. If closing costs total $3,500, the entire amount can be rolled into your new loan, meaning zero cash at closing.

IRRRL Rate Reduction Rule – Do You Have Enough Savings?

The VA doesn’t require a minimum rate reduction for an IRRRL, but lenders do. Most lenders require a “net tangible benefit,” which typically means:

At least 0.5% rate reduction, though

1% or more is ideal to ensure meaningful monthly savings

Important warning: Some lenders promote the IRRRL as a way to reduce your loan term from 30 years to 15 years. This can dramatically increase your monthly payment, even with a lower interest rate. For example:

Current: 30-year loan at 4.5% on $200,000 = $1,013/month

Refinance: 15-year loan at 3.5% on $200,000 = $1,428/month (a $415 monthly increase!)

While you’d save interest over time, this payment increase might not be affordable. Always run the numbers carefully before pursuing a shorter loan term.

IRRRL Application Process – Timeline & Steps

Submit application – Basic loan application (NMLS Form 1003 or lender-specific form)

Verification – Lender confirms previous VA entitlement use (may contact VA directly)

Appraisal (if required) – Most lenders skip this; if needed, typically 3-5 days

Processing – Lender prepares documents and underwriting report (3-5 business days)

Approval – Clear to close, no conditions (typically days 7-10)

Closing – Sign documents and fund the loan

Funding – New loan funds and existing mortgage is paid off

Fast approval: Most IRRRLs receive approval in 7-14 days with my office.

VA Cash-Out Refinance Loans – Access Your Home Equity

A VA cash-out refinance allows you to refinance your existing VA mortgage for more than you currently owe and receive the difference in cash. This is ideal for home improvements, debt consolidation, education expenses, or other major financial needs.

How Does a VA Cash-Out Refinance Work?

When you do a cash-out refinance, your new VA loan amount includes:

The balance you owe on your existing mortgage

Plus additional funds you’re borrowing (the “cash-out” amount)

Closing costs (which can be rolled into the loan)

Example: If your home is worth $250,000 and you owe $150,000, a VA cash-out refinance could allow you to borrow up to $200,000 or more, receiving $50,000+ in cash while refinancing your original debt.

The new loan is still a VA loan with the same benefits: no down payment, no PMI, and VA guarantee protection.

VA Cash-Out Refinance Eligibility

Cash-out refinancing has slightly stricter requirements than IRRRL:

You must have a VA loan to refinance

Loan-to-Value (LTV) limits apply – Generally, lenders allow cash-out up to 80% LTV (meaning your loan can be 80% of your home’s current value)

Your home must appraise – Unlike IRRRL, appraisals are required for cash-out loans

Income verification – Full underwriting including employment verification, credit review, and income documentation

Debt-to-income ratio – Your total monthly debt (including the new mortgage) cannot typically exceed 43-50% of gross income

Home improvements – Roof repairs, additions, kitchen remodels, HVAC systems

Debt consolidation – Pay off credit cards, personal loans, or medical debt at a lower rate

Education expenses – Fund college tuition or vocational training

Emergency expenses – Major home repairs or family emergencies

Investment – Real estate investments or business opportunities

Vehicle purchase – Consolidate auto loans into one lower-rate mortgage

The math of consolidation: If you have $25,000 in credit card debt at 18% APR ($450/month), refinancing into a VA cash-out loan at 6% APR could drop your payment to $150/month while rebuilding your credit faster.

VA Cash-Out Refinance Loan Limits by County

VA doesn’t cap how much you can borrow, but lenders set limits based on:

Your VA entitlement and available entitlement

Your home’s appraised value

Your income and credit qualifications

Jefferson County (Louisville) Loan Limits: For 2026, contact me for exact loan limits in your county, as they update annually. Generally, standard VA loans have no cap on borrowing, with limits applied based on your entitlement and the property value. To maximize your borrowing without a down payment, ensure you have sufficient available entitlement.

VA Cash-Out Timeline & Process

Cash-out refinancing takes longer than IRRRL because:

Appraisal required – 7-10 days

Full underwriting – 5-10 days

Verification of employment/income – 2-5 days

Clear to close – 2-5 days

Total timeline: 21-30 days, though my office frequently closes cash-out loans in 18-21 days.

VA Rate-and-Term Refinance – Traditional Refinancing

A rate-and-term refinance is a middle ground between IRRRL and cash-out refinancing. You refinance your existing loan without borrowing additional cash, but at a better interest rate or different term.

How Does Rate-and-Term Refinancing Work?

In a rate-and-term refinance:

Your new loan amount is approximately equal to what you currently owe (plus closing costs)

You’re not taking cash out

Your loan term can change (e.g., 30 years to 20 years)

Your interest rate is refinanced at current market rates

When to use rate-and-term refinancing:

You need a better rate than IRRRL allows

You’re converting an ARM (adjustable-rate) to a fixed-rate mortgage

You want to shorten your loan term without taking cash out

You prefer not to go through full cash-out underwriting

Rate-and-Term Eligibility

Rate-and-term refinancing sits between IRRRL and cash-out in terms of underwriting:

Some lenders require simplified underwriting (not full)

Appraisals may or may not be required

Income verification typically required

Credit check is standard

Debt-to-income limits apply (usually 43-50%)

When to Choose Rate-and-Term vs. IRRRL

Factor

IRRRL

Rate-and-Term

Rate reduction required

Usually 0.5%+

Can refinance at higher rate if needed

Underwriting

Minimal – streamlined

Moderate – some verification

Timeline

7-14 days

15-25 days

Closing costs

~$2,500-3,500

~$3,500-5,000

Best for

Faster, easier refis

More flexibility, specific goals

ARM to fixed

Yes

Yes

Comparison: IRRRL vs. Cash-Out vs. Rate-and-Term

Feature

IRRRL

Cash-Out

Rate-and-Term

No appraisal

✓

✗ (required)

~ (varies)

No underwriting

✓

✗ (full)

~ (simplified)

Access cash

✗

✓

✗

Fastest approval

✓ (7-10 days)

✗ (21-30 days)

~ (15-25 days)

Best rate

✓ (usually)

~

~

Flexibility

Limited

High

Moderate

Funding fee

0.55%

0.55%+

0.55%+

Occupancy requirement

Previous only

Current property

Current property

VA Funding Fees Explained – What You’ll Pay

All VA refinances include a funding fee (unless you’re exempt due to service-connected disability):

2026 VA Funding Fee Rates for Refinancing

For IRRRL (streamline) refinances:

First-time refinancers, no down payment: 0.55% of loan amount

Subsequent refinancers, no down payment: 0.55% (same as IRRRL)

National Guard/Reserve: Slightly higher (about 0.575%)

For cash-out and rate-and-term refinances:

First-time, no down payment: 2.3% of loan amount

Subsequent users, no down payment: 3.6% of loan amount

National Guard/Reserve: Higher percentages apply

Funding Fee Example: • $200,000 IRRRL with 0.55% fee = $1,100 • $200,000 cash-out with 2.3% fee = $4,600

The good news? You can finance the funding fee into your new loan, so you don’t need to pay cash at closing.

Funding Fee Exemptions – You Might Not Pay

You’re exempt from the VA funding fee if you:

Receive VA disability compensation for a service-connected disability (any percentage)

Are entitled to receive compensation for service-connected disability but receive military retirement/active duty pay instead

Are a surviving spouse of a veteran who died in service or from service-connected disability

If you’re exempt, provide VA documentation (VA letter of eligibility, DD Form 214, or similar) to your lender.

VA Loan Entitlement & Limits for Louisville, Kentucky

Your VA entitlement determines how much you can borrow without a down payment. The basic entitlement is $36,000, but if you have significant available entitlement, you can borrow much more.

How Entitlement Works

Example: • Basic entitlement: $36,000 • If your home value is $250,000 and you’re fully qualified: • You can borrow up to 4x your available entitlement without a down payment • $36,000 × 4 = $144,000 maximum • So lenders would typically fund up to $144,000 without requiring a down payment

However, if you have a higher purchase price or the property appraises for more, you may need to put money down.

For refinancing: Your available entitlement is what matters. If you have restored entitlement (paid off a previous VA loan), you have more borrowing capacity.

Jefferson County, Kentucky Loan Limits (2026)

Contact me for exact loan limits in your county, as they update annually. Generally:

Standard VA loans: No cap on borrowing

Loan limits apply based on your entitlement and income qualification

To maximize your borrowing without a down payment, ensure you have sufficient available entitlement

Common VA Refinance Questions Answered

Do I Need a Certificate of Eligibility for an IRRRL?

No, a new Certificate of Eligibility (COE) is not required for IRRRL refinances. Your lender can verify entitlement through the VA’s online system. However, if you have your COE handy, you can provide it to speed up verification.

Can I Refinance an ARM (Adjustable-Rate Mortgage) with VA?

Yes! Converting an ARM to a fixed-rate VA mortgage is a common and smart use of IRRRL or rate-and-term refinancing. When interest rates are low, this can lock in predictable payments for 30 years.

How Much Will My Monthly Payment Drop?

The payment reduction depends on:

Interest rate reduction – Each 1% lower rate saves roughly $215/month per $100,000 borrowed

Loan term – Shorter terms = higher payments but less total interest

Loan amount – Larger loans have proportionally larger payment changes

Quick calculation: Refinancing $150,000 from 5% to 4% typically saves ~$165/month.

Can I Refinance if I Have Bad Credit?

Yes, VA refinancing is more flexible than conventional financing:

IRRRL: No credit check required

Cash-out/Rate-and-term: Minimum credit score typically 580-620

Even with recent delinquencies, many veterans qualify

If you have credit concerns, discuss them with me. I’ve helped veterans with bankruptcies, foreclosures, and late payments refinance successfully.

How Long Does Refinancing Take?

IRRRL: 7-14 days (fastest)

Rate-and-term: 15-25 days

Cash-out: 21-30 days

My office often beats these timelines with efficient processing.

What Happens to My Current Mortgage During Refinancing?

Your old mortgage remains active until the new loan funds and pays it off. Once the new loan closes:

The new lender sends funds to the old lender

Old mortgage is paid off in full

Your home title is transferred to the new lender

You begin payments on the new mortgage

There’s no gap in coverage or risk of losing your home.

VA Refinance Success Stories from Louisville Veterans

Over 20+ years, I’ve helped thousands of Kentucky veterans refinance. Here are real-world examples:

Example 1 – IRRRL Streamline Savings

Jim’s Story: Jim, a Louisville veteran, had a VA mortgage at 5.5% on $180,000. When rates dropped to 4.25%, he did an IRRRL refinance in just 10 days. His monthly payment dropped from $1,022 to $886—saving him $136/month or $1,632/year. No appraisal, no underwriting. Clean and simple.

Example 2 – Cash-Out for Home Improvement

Maria’s Story: Maria, a Fort Knox-area veteran, had $280,000 owed on her home valued at $380,000. She refinanced with a $300,000 VA cash-out loan, receiving $20,000 to renovate her kitchen and update the home’s electrical system. Her payment only increased $150/month while adding home value and equity.

Example 3 – ARM to Fixed-Rate Security

David’s Story: David’s VA ARM mortgage was set to adjust upward from 3.8% to 5.2%. Before the adjustment, he refinanced into a 30-year fixed VA loan at 4.3%, locking in stability. His payment actually decreased while eliminating the risk of rising rates.

Why Work With Me for Your VA Refinance?

I’m Joel Lobb, NMLS #57916, and I’ve spent 20+ years specializing in Kentucky VA mortgages. Here’s what sets my service apart:

✓ Local expertise – I know Louisville, Jefferson County, Fort Knox, and all 120 Kentucky counties

✓ Fast approvals – Same-day pre-approval on most applications; average close in 18-21 days

✓ Transparent guidance – I explain all options without pressure and help you choose what’s best for YOUR situation

✓ Personal service – I answer my phone and attend most closings personally

✓ 1,300+ families helped – Over two decades of proven success

✓ Free pre-qualification – No hidden fees, no commitment

✓ 24/7 accessibility – Call or text me anytime

Your Next Steps

Ready to explore your refinance options?

Call or text me at 502-905-3708 – I’ll discuss your current mortgage and goals

Send your information to kentuckyloan@gmail.com – I’ll analyze your situation and options

Complete a free pre-qualification – Same-day approvals on most applications

Lock in your rate – Secure the best rate available

No pressure. No obligation. Just honest guidance from a Kentucky veteran mortgage expert.

Ready to Start Your VA Refinance?

Get a free pre-qualification today and discover how much you could save with VA refinancing.📞 Call or Text: 502-905-3708📧 Email: kentuckyloan@gmail.com🌐 Visit: http://www.kentuckyvamortgage.com

Important Disclaimers

This website and content are not endorsed by the VA, FHA, USDA, or any government agency. They are provided for educational purposes only.

Loan qualification: All loans are subject to:

Income verification and credit approval

Property appraisal and valuation (when required)

Sufficient equity (LTV requirements)

Debt-to-income ratio limits

Final underwriting approval

Rate changes: Interest rates are subject to market conditions and change daily. Rates mentioned are examples only.

Equal Housing Opportunity: I am an Equal Housing Lender. I serve all applicants fairly regardless of race, color, national origin, religion, sex, familial status, or disability.

No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant. Equal Opportunity Lender.

Most Asked Questions About Kentucky VA Loans (2026 FAQ)

If you’re a veteran, active duty service member, or surviving spouse in Kentucky, the VA loan can be one of the strongest paths to homeownership.

This 2026 FAQ answers the questions buyers ask the most—eligibility, credit, income, entitlement, funding fee, rates, assumptions, and refinancing.

Quick Take (tell-it-like-it-is)

Eligibility means you earned the benefit. Approval means you meet lender underwriting.

VA doesn’t set a minimum credit score, but lenders often do.

VA loans are for primary residences—no rentals or vacation homes.

Funding fee applies unless you’re exempt (often due to service-connected disability).

VA loan entitlement is the portion of your VA benefit that backs (guarantees) a percentage of your mortgage for an approved lender.

The VA does not issue home loans directly—lenders do—while the Department of Veterans Affairs provides the guaranty that makes $0 down and no PMI possible.

In 2026, veterans with full entitlement are not subject to county loan limits for a primary residence, but you still must qualify based on income, credit, and the home’s appraised value.

Am I eligible as a surviving spouse?

Many surviving spouses are eligible for VA home loan benefits. Common eligibility paths include:

Unmarried surviving spouse of a veteran who died on active duty or from a service-connected disability

Surviving spouses who remarried after age 57 and on/after December 16, 2003 may remain eligible

Spouse of an active-duty service member who is MIA or POW for 90+ days may be eligible for one-time use

Surviving spouses may also be eligible for VA refinancing options in some circumstances, including VA Streamline (IRRRL).

How do I get my Certificate of Eligibility (COE)?

The COE is the official proof of your eligibility and entitlement. Most lenders can retrieve it electronically in minutes.

Veterans can also request the COE through the VA, which may take longer. Bottom line: you can’t close a VA loan without a COE.

Who is eligible for a VA loan?

You may be eligible if any one of the following is true:

90 days of active duty during wartime

181 days of active duty during peacetime

6 years in the National Guard or Reserves

Eligible surviving spouse

Eligibility vs. prequalification vs. preapproval

Eligibility confirms you earned the VA benefit. Prequalification is an initial estimate of buying power. Preapproval is the stronger, document-backed step

that real estate agents and sellers take seriously. If you’re shopping in Kentucky, aim for preapproval—not just a quick prequal—before making offers.

Entitlement & Using Your VA Loan More Than Once

How does entitlement work in 2026?

Entitlement generally has two layers (basic and bonus) that together determine the VA guaranty.

If you’ve used your VA loan before, you may still have remaining entitlement available. Prior use does not automatically block another VA purchase—structure matters.

How do I restore my VA entitlement?

Full entitlement is commonly restored when you sell the home and the VA loan is paid off. You then request restoration through the VA (typically with VA Form 26-1880),

along with documentation showing payoff. In limited cases, a one-time restoration may apply.

What is “second-tier” entitlement?

Second-tier entitlement can help veterans buy again after prior VA loan usage or even a foreclosure history.

Depending on remaining entitlement and purchase price, a down payment may be needed. This is where a lender who understands VA structure makes a difference.

Can I use a VA loan for a second home or rental property?

No. VA loans are designed for owner-occupied primary residences. You must intend to occupy the home as your primary residence within a reasonable time after closing.

Qualification: Credit, Income, DTI & Residual Income

Who sets VA loan guidelines: the VA or my lender?

The VA sets minimum standards. Lenders add overlays. VA does not publish a minimum credit score, but most lenders use a benchmark.

You must satisfy both VA requirements and the lender’s underwriting rules to get approved.

If I have bad credit, can I still get a VA loan?

Possibly. Here’s the straight answer: poor credit can be worked around in some cases, but it depends on the overall risk profile—income stability, residual income, payment history,

and how recent the credit events are. “Quick fixes” usually fail; documented improvement and a clean recent history work.

Can someone else sign on the loan with me?

VA co-borrowers are restricted. In most cases, the co-borrower must be your spouse or another eligible veteran.

Parents, friends, or significant others who are not eligible veterans typically cannot co-borrow on a VA loan.

What income can I use to qualify?

Lenders verify that you have stable, reliable income and enough residual income after housing and debts. Common income sources include:

Military base pay and allowances (including BAH, when stable and likely to continue)

Non-military employment

Retirement and disability income

Self-employment (with additional documentation)

Commissions, overtime, bonus income (typically needs a 2-year history)

Spouse’s income, alimony/child support (when documentable and expected to continue)

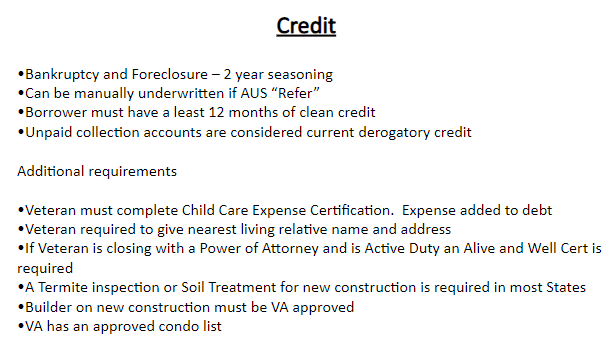

How long after bankruptcy or foreclosure can I qualify?

Bankruptcy and foreclosure do not automatically disqualify you, but timing matters. Many lenders look for about 2 years after Chapter 7 discharge or foreclosure.

Chapter 13 may be possible after 12 months of on-time plan payments with trustee approval, depending on the lender. Overlays apply—this is not one-size-fits-all.

Do I need tax returns to apply?

Not always. Many borrowers can qualify without providing tax returns, because lenders can use IRS transcripts and W-2/paystub documentation.

Self-employed or commission-heavy income usually requires tax returns and additional paperwork.

Rates, Closing Costs & the VA Funding Fee (2026)

What fees should I expect to pay?

VA limits certain charges to protect veterans from excessive lender fees. Typical costs include title/settlement fees, appraisal, credit report,

and the VA funding fee (unless you’re exempt). Sellers can contribute up to a set amount in concessions, which may help reduce your cash to close.

What is the VA funding fee?

The VA funding fee is a one-time fee that helps keep the VA loan program running and replaces monthly mortgage insurance.

The fee varies based on loan type (purchase/refi), down payment (if any), and whether it’s first-time or subsequent use.

Many veterans with service-connected disability ratings are exempt from the funding fee.

If you want, we can estimate your funding fee based on your COE status and the exact structure of the loan.

How are VA loan rates determined?

Rates are driven by broader markets (especially bonds) and by your risk profile (credit, down payment, occupancy, property type).

Rate pricing can change daily. If you’re shopping seriously, timing your lock strategy matters.

Does my credit score affect my VA loan rate?

Yes. Even with VA’s flexibility, stronger credit typically improves pricing and reduces lender conditions.

If your scores are borderline, improving them before you lock can materially reduce the total cost over time.

Does the VA loan offer adjustable rates?

Some lenders offer VA ARMs (adjustable-rate mortgages). They can make sense for short-term ownership plans (common with relocations),

but they are not the default best option for most buyers.

VA Loan Guidelines & Common Rules

Can I borrow more than the home’s value?

On purchases, VA financing is tied to the appraised value and allowable costs. Cash-back is limited on purchases.

For refinances, VA Cash-Out can allow high loan-to-value in certain scenarios, subject to lender guidelines.

Can I have more than one VA loan at a time?

Sometimes, yes—typically tied to legitimate occupancy needs (relocation, deployments, job moves).

Most veterans have one VA loan at a time, but multiple VA loans can be possible depending on remaining entitlement and circumstances.

What is the maximum VA home loan?

VA does not set a maximum loan amount for borrowers with full entitlement. Your maximum is determined by income qualification,

residual income, credit, and the property’s appraised value.

Are VA loans assumable?

Yes. VA loans are assumable, which means a qualified buyer may be able to take over the existing rate and terms.

Assumability can be a major resale advantage in higher-rate environments, but the buyer must qualify and the servicer must approve the assumption.

Can I pay off a VA loan early?

Yes. VA loans do not have a prepayment penalty. You can pay extra principal or pay off the loan early without lender penalties.

When is a VA loan NOT the best option?

VA is the strongest fit for most eligible buyers—especially those using $0 down. That said, if you have a large down payment and exceptional credit,

conventional financing can sometimes compete on pricing. The best move is a side-by-side comparison, not an assumption.

VA Refinancing (2026)

Can the VA loan help lower my monthly bills?

VA has two primary refinance options:

VA IRRRL (Streamline): Designed to reduce rate/payment on an existing VA loan with lighter documentation.

VA Cash-Out Refinance: Refinance and potentially access equity; can also refinance a non-VA loan into VA if eligible.

Streamlines can sometimes be completed without an appraisal, depending on lender policy.

Can I refinance into a VA loan if I don’t currently have one?

Yes. Eligible veterans can refinance a conventional or FHA mortgage into a VA loan using the VA Cash-Out refinance program

(even if you’re not taking cash out), subject to underwriting and lender guidelines.

What Types of Homes Can I Buy With a VA Loan?

You can typically use a VA loan in Kentucky to:

Buy a primary residence (single-family home)

Buy a VA-approved condo

Buy up to a 4-unit property (one unit must be owner-occupied)

Build a home (with additional requirements)

Buy and improve a home in certain scenarios

You cannot use a VA loan to buy a vacation home or an investment property you won’t occupy as your primary residence.

<!–

WORDPRESS.COM FIXED + CLEAN VERSION

What I changed (so it works correctly on WordPress.com):

– Added the missing and wrapper.

– Removed the global * reset and the body styling that can conflict with your theme.

– Kept styles scoped to this post only by prefixing everything with .ky-va-refi

– Left your content intact, just made it more WordPress-safe and stable.

Replace https://www.yoursite.com/apply/ with your actual application URL.

–>

If you are a veteran or active-duty homeowner in Louisville, Kentucky, and you are researching VA refinance options through Google, ChatGPT, YouTube, or other online sources, you want one thing: a refinance that improves your financial position. Lower payment, better terms, or a more stable loan. Anything else is noise.

Free Louisville VA Refinance Review

I will review your current mortgage, confirm the VA refinance option that applies, and tell you clearly whether refinancing makes sense.

Serving Louisville, Jefferson County, and statewide Kentucky.

What is a VA refinance loan in Louisville, Kentucky?

A VA refinance replaces your current mortgage with a new VA-backed loan. Depending on the program, it can reduce your interest rate, lower your monthly payment, eliminate monthly mortgage insurance, or improve long-term stability. The VA sets the baseline rules, but individual lenders often add overlays that can make the process harder than it needs to be.

Two VA refinance options for Louisville homeowners

1) VA Streamline refinance (IRRRL)

The VA Interest Rate Reduction Refinance Loan (IRRRL), commonly called a VA Streamline, is designed for borrowers who already have a VA mortgage and want a simpler refinance.

VA Streamline highlights:

Built to lower rate and payment (when the numbers work)

No VA-required appraisal

No VA-required income verification

No VA-required credit check

Typically faster than a traditional refinance

Important: some lenders add overlays (appraisal requirements, credit score minimums, etc.). Your approval path depends on the lender, even when the VA does not require it.

Closing costs apply, but they are commonly rolled into the new loan balance. VA guidelines may allow financing up to $6,000 in approved energy-efficiency improvements in certain scenarios.

2) VA Cash-Out refinance (cash out is optional)

The VA Cash-Out refinance is the flexible option. It can be used to refinance a current VA loan, or to refinance a non-VA loan into VA (such as FHA or conventional). Taking cash out is optional.

VA Cash-Out refinance is commonly used to:

Refinance FHA to VA and eliminate monthly mortgage insurance

Refinance conventional to VA and eliminate monthly mortgage insurance

Adjust your loan structure with full underwriting

Access equity if needed (optional)

This program requires a full VA underwrite: income documentation, debt-to-income analysis, and an appraisal.

Why Louisville veterans refinance VA loans

Louisville homeowners refinance for practical reasons: reduce monthly payment, move from adjustable to fixed, remove monthly mortgage insurance, or improve long-term affordability. The VA program is strong, but the refinance only makes sense if it produces a measurable benefit.

VA net tangible benefit requirement

VA guidelines require that a refinance provides a net tangible benefit to you. In plain English: the refinance has to improve your situation in a real way. If the payment does not improve or the long-term benefit is not clear, you should not refinance.

A strong VA refinance review should confirm:

Real payment savings or a clear long-term benefit

Reasonable break-even timeline

Closing costs explained upfront

The refinance meets VA net tangible benefit expectations

Global lender vs local Louisville VA refinance support

Many VA loans are serviced by large national lenders. That does not make the loan bad, but it often creates call-center communication, slow follow-up, and one-size-fits-all advice. A local Louisville VA refinance specialist typically gives you clearer accountability and Kentucky market awareness from start to finish.

YouTube: what Louisville VA borrowers should watch for

A lot of VA refinance content online is generic. When you watch YouTube videos or short clips, focus on content that explains the program rules, lender overlays, and the break-even math. If a video only sells “low rates” without addressing total cost and net benefit, it is not trustworthy guidance.

” frameborder=”0″ allow=”accelerometer; autoplay; clipboard-write; encrypted-media; gyroscope; picture-in-picture; web-share” referrerpolicy=”strict-origin-when-cross-origin” allowfullscreen>”>

Video Section Optional: Embed your YouTube VA refinance video here using the WordPress.com YouTube block.

Paste your YouTube link directly in the WordPress editor.

Louisville VA refinance FAQs

Do I need an appraisal for a VA Streamline (IRRRL)?

The VA does not require an appraisal for IRRRL in many cases, but some lenders add appraisal overlays. Your outcome depends on the lender’s requirements.

Can I refinance into a VA loan if I have FHA or conventional?

Yes. Eligible veterans can use the VA Cash-Out refinance to convert FHA or conventional into VA. Cash out is optional, but full underwriting and an appraisal are required.

Can closing costs be rolled into a VA refinance?

Often, yes. The structure depends on the program, loan terms, and lender rules. The key is confirming the final payment and the break-even timeline before moving forward.

Related Louisville and Kentucky VA refinance resources

Kentucky VA Mortgage does not have a minimum credit score requirement. When a lender requires a minimum credit score it is generally a 580-620, that is called a lender overlay. An overlay is a lender’s own underwriting guidelines above and beyond the VA guidelines.

The most common reason for a Veteran’s loan to be declined is not having a required minimum credit score per the lenders own set of guidelines above and beyond what the VA requires.

As announced by the VA in Circular 26-19-30 (which provides interim guidance on implementing “The Blue Water Navy Vietnam Veterans Act of 2019″) the conforming loan limit cap on guarantees was removed for Veterans with full entitlement. For Veterans who have previously used entitlement and the entitlement has not been restored, the maximum amount of guaranty entitlement available to the Veteran (for a loan above $144,000) is 25 percent of the conforming loan limit reduced by the amount of entitlement previously used (not restored) by the Veteran. The new guaranty requirements apply for loans closed on or after January 1, 2020.

In 1944, the Servicemen’s Readjustment Act was established in to provide veterans and their surviving spouses with a number of benefits. Among these benefits was the VA loan program. VA loans allow veterans and military to purchase homes with 100% financing, no mortgage insurance, and limited closing costs.

In order to apply for a VA loan, you need to meet eligibility requirements. Most veterans, military, and spouses of deceased military members will be eligible. Veterans can apply without any delay if minimum active duty service requirements have been met. Active duty service members on the other hand will need to complete a minimum of 6 months of service first. National Guard and reservists will need to wait 6 years before the benefit kicks in. If they are called to active duty at any point, they will become eligible after only 181 days.

Anyone who intends to apply for a VA loan will need to obtain their Certificate of Eligibility. It is important to note that the COE only proves to your lender that you have met the minimum service requirements. It is not a guarantee that you will be approved for a loan. One of the easiest ways to get your COE is through the VA’s eBenefits Portal. Whether you are looking to purchase your very first home or are looking to take advantage of the VA loan program to refinance, we can help you find a loan that meets your exact needs.

What Does Having Basic Entitlement of $36,000 Mean?

The $36,000 does not represent the maximum loan amount you can obtain through the VA Home Loan Program. The figure merely provides evidence to your lender that you have full VA entitlement.

With this entitlement and underwriter approval, you can obtain a loan,

I Now Have My COE, What Do I Do Next?

Contact any VA approved lender and start the loan process. Do note that the COE does not guarantee you a VA loan; you still must qualify based upon your income and credit.

How Do I Apply For a Loan?

VA does not do any direct lending, and as such VA does not accept loan applications from veterans. You must contact a VA approved lender in order to apply for a VA loan. For more information about VA loans, visit www.benefits.va.gov/homeloans/.

What is the VA Interest Rate?

VA does not establish interest rates or closing costs for VA loans. Rates are negotiable between you and your lender. It is advisable to obtain quotes from at least three different lenders.

What is the Minimum Credit Score Required for a VA loan?

VA has no minimum credit score requirement. However, the lender you choose to do business with may have such a requirement.

What Types of Property Does My COE Cover?

The VA Home Loan program guarantees loans for real property that is to be used by the veteran as a primary residence. The program does not cover vacation homes, vacant land, multiplexes in excess of four units, motor-homes, small business loans, or commercial buildings.

Can I Use My VA Entitlement to Refinance?

Yes. You can refinance any type of loan on your property using your VA entitlement.

Why Does My COE Reflect a Paid-in-Full Loan With No Restoration of Entitlement?

In order for entitlement to be restored, the prior VA loan must be paid in full and the property disposed of. If you no longer own the property, please state as such on your application form 26- 1880 and resubmit. Do note that you can obtain a restoration of entitlement without disposing of the property when the loan is paid in full on a one time basis

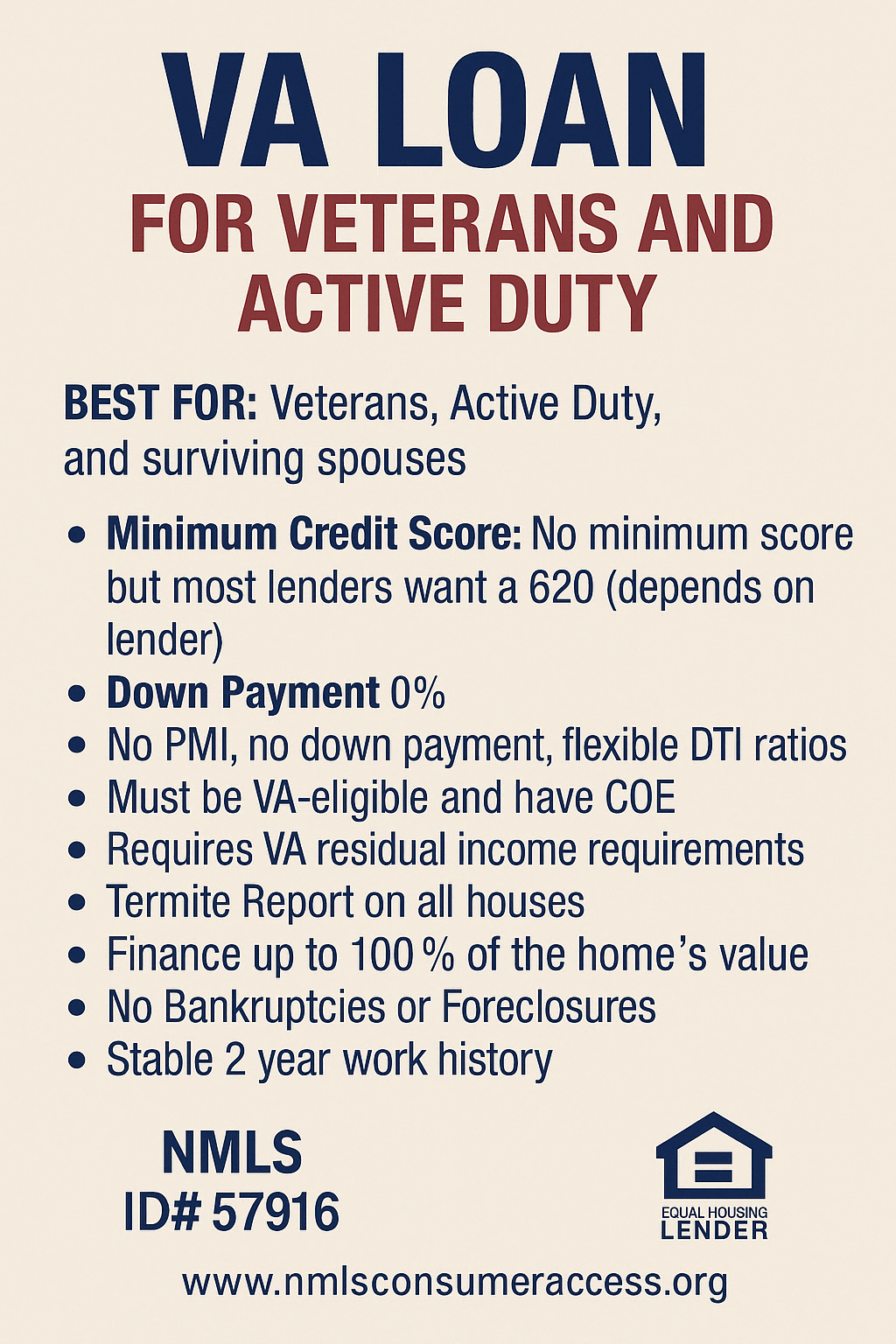

No down payment in most cases for purchase loans (up-front money toward your home purchase), and easier borrower credit requirements.

No monthly mortgage insurance premiums or private mortgage insurance (PMI).

Lower homebuyer closing costs, and limits to what borrowers can be charged.

The opportunity to roll your “VA funding fee” into your mortgage.

The ability to refinance a non-VA loan into the VA mortgage program.

The opportunity to: ask a home seller to contribute up to 4 percent of the mortgage amount to cover some of the closing costs; ask your lender to cover some of the closing costs; seek closing cost assistance through state homebuying programs created for veterans and first-time buyers.

The right to become a VA borrower for life. In most cases you can use VA mortgage programs forever, and sometimes you can have more than one VA loan.

Eligibility of financing for spouses of service-members who died in the line of duty or from a service-related disability.

You can review all types of Kentucky VA Home Loans here, including purchase mortgages, refinance mortgages (called Interest Rate Reduction Refinance Loans or IRRRLs), and cash-out refinance loans.

To qualify for a Kentucky VA Home Loan, usually a military veteran or service-member must have 90 consecutive days of active service during wartime, or 181 straight days of service during peacetime, or six years in the national guard or reserves of a particular military branch. You can find out if you’re eligible here.

Kentucky VA mortgage comes with an additional closing cost called a “VA funding fee” of between 1.4 to 3.6 percent on the amount borrowed (depending on your circumstance). This special fee that non-VA borrowers never have to pay helps partially fund the “government backed” part of the VA borrower program, and many VA borrowers can roll it into their mortgage.

VA Loan Quick Facts

0% Down

Minimum Down Payment

620 Credit

Minimum Credit Score

41% DTI

Max Debt-to-Income Ratio

What is a VA Loan?

VA Loans are designed to assist veterans purchase a home. Active duty military and veterans across the nation will enjoy the desirable loan terms and low interest rates that often come with a VA loan. Additional benefits like no down payment requirement help make home buying an affordable and cost-effective reality for those who have served and continue to serve our country.

What are the benefits of a VA Loan?

VA Loan benefits and features:

Zero down payment

Buyers may finance the funding fee into the loan

Closing costs may be covered

Buyers may use gifts and seller contributions to cover closing costs

Who may benefit from a VA Loan?

A VA Loan may the right fit for you if:

You’re an eligible veteran or active-duty military

You’re buying a first home or are a repeat homebuyer

Kentucky VA loans are typically the best solution for our honored veterans and service members. Contrary to popular belief, VA loans are fairly easy to process and tend to not be any more complicated than any other loan program that we offer.

Here are some of our favorite features of Kentucky VA loans:

No Down Payment – VA is a true 100% financing loan with no minimum investment required.

No Monthly Mortgage Insurance – VA loans do not require monthly mortgage insurance, providing significant cost savings to our Veterans. They do require an upfront Funding Fee of 0 to 3.6% that is paid directly to the VA. This funding fee is financed into the loan and may be waived for some buyers based on their scenario.

Credit scores – Interest rates and underwriting requirements are less credit score sensitive than other loan programs. In some scenarios, we are able to lend to buyers with scores in the mid-500s. Buyers without a credit score may be eligible with additional requirements.

Renovation loans – We can do purchase and refinance loans that roll the cost of minor and cosmetic repairs into the loan amount.

Property Types – VA Loans can be used on 1-4 unit properties, primary residence only. They can also be used on VA approved condominiums and qualifying manufactured homes.

VA Loans are issued by federally qualified lenders and are guaranteed by the United States Veterans Administration. VA Loans are available to military personnel and veterans, including Reservists and members of the National Guard. Surviving spouses may be eligible in specific circumstances.

VA Loan eligibility is determined using the Certificate of Eligibility (COE) document. We work directly with the VA on the buyer’s behalf to obtain this document. A buyer can take advantage of the VA loan program more than once!

How can I get a VA Mortgage loan in Kentucky in 2021?

Kentucky veterans and active duty service members are eligible. However, all veterans, active duty service members and National Guard members must meet certain requirements.

Have more than six years of service with the National Guard or Reserves

Also, Kentucky VA loans are available to the surviving spouses of military members who died in the line of duty.

How does a Kentucky VA Home Mortgage Loan Work?

The Veterans Administration guarantees the loan, but they do not make it.. VA sets forth the guidelines as far as credit, income, assets, property requirements and inspections, but the lenders use this to make a lending decision. Usually the credit, income and assets, i.e. bank statements, pay stubs and tax returns, along with credit report and credit score to get a pre-approval upfront. The appraisal report is done by VA assigned appraiser in the area and neither the lender, borrower, realtors, sellers, have no control as far as choosing the Kentucky VA appraiser. VA will typically give the VA approved appraiser 10 days to make contact, and usually get the appraisal report back within 7-10 days after inspections.

How much can I borrow with a Kentucky Mortgage VA loan?

There is no max income limit for VA loans beginning in 2021.

VA Loan Limits in Kentucky for 2021

VA does not set a cap on how much you can borrow to finance your home. However, there are limits on the amount of liability VA can assume, which usually affects the amount of money an institution will lend you. The loan limits are the amount a qualified Veteran with full entitlement may be able to borrow without making a down-payment. These loan limits vary by county, since the value of a house depends in part on its location.

The basic entitlement available to each eligible Veteran is $36,000. Lenders will generally loan up to 4 times a Veteran’s available entitlement without a down payment, provided the Veteran is income and credit qualified and the property appraises for the asking price.

For all non-IRRRL VA loans, effective with loans closed on or after January 1, 2021, we are aligning with FHFA’s increase to the county loan limits. VA does not have a maximum loan amount, but instead uses the county loan limit to determine the maximum potential entitlement available for veterans with used or compromised entitlements.

As a reminder, we require that all Kentucky VA loans conform to GNMA secondary market guidelines which include the minimum 25% coverage requirement.

What is the credit score or fico score required for a Kentucky VA Mortgage loan?

VA has issued guidelines that calls for no minimum credit score. However, most VA Kentucky lenders will want to see a credit score of at least 620 before approving the mortgage. There are two lenders we work with currently that will do down to a 500 credit score, but it is very difficult to get them approved . The best thing to do is let someone pull your credit and see where you are at and go from there. A lot of lenders you will see will want a 620 credit score, with a few going down to 580. Again, this will vary greatly from lender to lender and be based upon our automated underwriting findings (AUS) from Desktop Underwriting.

Do VA Loans Require a Down payment.

Kentucky VA home buyers do not require a down payment. It does not matter if you have a 500 credit score or 780 credit score, all VA loans offer a no down payment option to applicants. The only reason you would need a down payment is if you had to qualify for the home loan payment, or if you were borrowing with a co-applicant, that is not married to the borrower. For example, if a veteran is legally married, and his wife is not a veteran, that is fine with VA and you would not need a down payment, However, let’s say the borrower and his friend or girlfriend wanted to buy a house together, and we needed the co-borrowers income and credit to make it work, then you would need to put down 12% on the home loan since the borrower and co-borrower are not legally married.

Mortgage insurance on A VA loan?

One of the great benefits of VA loans is that have no monthly mortgage insurance premium. When you compare this to FHA, USDA mortgage loans in Kentucky, you would need to pay monthly mortgage insurance.

There is an upfront funding fee from VA , but if you are disabled, you can get this waived sometimes. See chart below

In order for VA to guarantee the home loan, there is a closing cost assessed by the VA to originate the loan called a funding fee. This fee will vary, depending upon the type of Kentucky VA loan, whether this is your first time to use your entitlement, if you are a disabled veteran, the down payment and if you served active duty or in the National Guard/Reserves.

How long does it take to close a VA Mortgage loan in Kentucky?

There’s no set-in-stone time limit for how long the Kentucky VA loan process takes, but on average, you should be able to get it done within 30 days depending on the appraisal report and home inspections

VA mortgage loans is the only Government sponsored mortgage that requires a termite inspection., so keep that in mind on your inspections when you are having them done after the accepted contract.

Can I only use a VA loan once in Kentucky?

This is a common myth with many VA eligible home buyers and homeowners. If you’re eligible for the VA loan, then you’re eligible for your entire life. Plenty of home buyers end up using the VA loan more than once, mostly because it’s arguably the best loan program out there.

Can I get a Kentucky VA Mortgage loan with a previous Bankruptcy or Foreclosure?

If the applicant has finished making all payments satisfactorily, the lender may conclude that the applicant has reestablished satisfactory credit

If the applicant is still in the repayment period, as long as 12 months’ worth of satisfactory payments have been made and the trustee or Bankruptcy Judge approves of the new credit, the lender may give favorable consideration.

If the bankruptcy was discharged within 1 to 2 years, it is probably not possible to determine that the applicant is a satisfactory credit risk unless both of the following requirements are met

The applicant has obtained credit subsequent to the bankruptcy and has made satisfactory payments over a continued period of time, and

The bankruptcy was caused by circumstances beyond the control of the applicant such as unemployment, prolonged strikes, medical bills not covered by insurance and the circumstances are verified. Divorce is not viewed as a circumstance beyond the applicants control

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Kentucky VA Loans are designated to offer long-term financing to eligible Kentucky veterans or their surviving spouses. As a ex-army tanker (19 kilo) I support our heroes with our VA financing options in all 120 counties of Kentucky. The intention of this program is to help Kentucky veterans purchase properties with no down payment and relaxed credit qualifying guidelines because a Kentucky VA Loan is less restrictive when it comes to qualifying for a mortgage loan for VA .

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

A Kentucky VA loan is issued by a private lender in Kentucky and insured by the Department of Veterans Affairs or VA . for qualified U.S. veterans, active-duty military personnel and certain surviving spouses.

You were separated from military service in a situation “other than dishonorable discharge.”

As a veteran or active military, you meet specific length-of-service requirements.

You are a reservist or a member of the National Guard.

You are a qualified surviving spouse of a deceased veteran.

In addition, there are these requirements:

The home must be your primary residence.

You must have a valid certificate of eligibility from the VA.

Although the VA has no minimum credit score requirement, most lenders do.

Kentucky VA Mortgage Loan Benefits.

A Kentucky VA loan begins with one important distinction: relaxed credit-qualifying standards in regards to credit scores, past bankruptcies and foreclosures

VA has no minimum credit score requirement, lenders often require scores of at least 580 A few lenders will approve loans with credit scores as low as 500 in some cases .2 year removed from bankruptcy and foreclosure is required too with a clear Cavirs number.

THE MAJOR BENEFITS of a Kentucky VA mortgage are as follows:

$0 down payment unless the purchase price is more than the appraised value of the property or it’s higher than the local VA loan limit.

Mortgage rates are typically lower than rates on conventional loans.

No mortgage insurance is required monthly, just upfront funding fees.

You can reuse your VA loan benefit.

You don’t have to be a first-time home buyer.

VA-backed loans can be assumable — this means they can be taken over by someone you sell the house to, even if that person isn’t a service member.

A bankruptcy discharged more than two years ago — and in some cases, within one to two years — will not preclude you from getting a VA loan.

Types of Kentucky Mortgage VA loans

Home purchase in Kentucky: A Kentucky VA loan can be used to buy an existing home or a condominium in a VA-approved development, or to build a home.

Cash-out refinance in Kentucky: A VA cash-out refi replaces your mortgage with a new loan, while tapping some of your home’s value for things like paying off debt or making home improvements. It also can be used to replace a non-VA loan with a VA loan.

Interest rate reduction refinance loan or rate and term: A VA IRRRL (which is pronounced “Earl”) is also called a streamline refinance loan. You can replace an existing VA loan with a mortgage offering a lower interest rate, or move from an adjustable-rate loan to one with a fixed interest rate. Usually no appraisal or income documentation is needed for most IRRRL Refinances saving you a lot of money and qualifying headaches on a refinance

Although mortgage insurance isn’t charged on Kentucky VA loans, a “funding fee” serves the same purpose: to help lenders defray the expenses of foreclosing on borrowers who default. The fee ranges from 1.25% to 3.3% of the loan balance, depending on your down payment, branch of the military and whether or not it’s your first time getting a VA loan.

The VA funding fee can be rolled into your total loan package, but that will likely raise your interest rate and will absolutely raise your monthly payment.

Though a down payment is not generally required, putting 5% or more down will reduce your VA funding fee. And a down payment will lower your monthly payment, too.

Childcare Expenses

Did you know that VA considers childcare expenses a debt?

VA has given guidance that Borrowers with children age 12 and under must complete and sign a “Child Care Letter”. The lender must obtain the letter from the veteran documenting the childcare expense or detailing why no expense is incurred. Ensure that the current daycare provisions will remain logical based on the location of the new home. If applicable, the name and address of the childcare provider, should be obtained. This expense should be listed under section D, line 29, “Job Related Expense (e.g., child care)” on the VA Loan Analysis.

A “VA Child Care Expense Certification” form can be found on the Fairway website under “Forms & Documents” or by clicking here: VA Child Care Expense Certification

Kentucky VA Guidelines After Bankruptcy And Foreclosure On Waiting Period After Foreclosure

Kentucky VA Loans only have a two year mandatory waiting period after foreclosure, deed in lieu of foreclosure, or short sale for a Veteran to qualify for a Kentucky VA Loan.

Kentucky VA Guidelines After Bankruptcy And Foreclosure On Waiting Period After Chapter 7 and 13

There is a two year mandatory waiting period to qualify for a VA Loan after a Chapter 7 Bankruptcy discharged date and 1 year for A Chapter 13 Bankruptcy

Kentucky VA Loan Process

A list of items needed for underwriting is provided to the buyer based on the buyer’s scenario. Based on the borrower’s scenario, the process is explained which includes the items discussed below such as the VA certificate of eligibility (COE), DD-214, income verification, and more.

How to Apply for a VA Home Loan Certificate of Eligibility (COE)

The first step in getting a VA direct or VA-backed home loan is to apply for a Certificate of Eligibility (COE). This confirms for your lender that you qualify for the VA home loan benefit. Find out how to apply for a COE. Then, choose your loan type and learn about the rest of the loan application process.

How do I prepare before starting my application?

Gather the information you’ll need to apply for your COE. Click on the description below that matches you best to find out what you’ll need:

Veteran

Servicemember

Current or former activated National Guard or Reserve member

Current member of the National Guard or Reserves who has never been activated

Discharged member of the National Guard who was never activated

Discharged member of the Reserves who was never activated

Surviving spouse of a Veteran who died on active duty or who had a service-connected disability

In some cases, you can get your COE through your lender using our Web LGY system. Ask your lender about this option.

By mail

To apply by mail, fill out a Request for a Certificate of Eligibility (VA Form 26-1880) and mail it to the address listed on the form. Please keep in mind that this may take longer than applying online or through our Web LGY system. Download VA Form 26-1880.

Next steps for getting a VA direct or VA-backed home loan

Applying for your COE is only one part of the process for getting a VA direct or VA-backed home loan. Your next steps will depend on the type of loan you’re looking to get—and on your lender (for most loans, the lender will be a private bank or mortgage company; for the Native American Direct Loan, we’ll be your lender).

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

The changes are part of the Blue Water Navy Vietnam Veterans Act of 2019, which became effective Jan. 1, 2020. Besides extending disability benefits to more Vietnam War veterans exposed to Agent Orange, the new law eliminates VA loan limits for borrowers with full entitlement to VA loans. It also increases the VA funding fee for most borrowers. (The fee decreases slightly for National Guard and Reserve members.)

VA home loans are a benefit for current and veteran service members. They have competitive interest rates and usually no down payment requirement, among other advantages. VA loan limits are the maximum loan amount the Department of Veterans Affairs can guarantee without borrowers making a down payment. VA funding fees are one-time fees borrowers pay in lieu of mortgage insurance to help cover the government’s costs for backing the loans. If a borrower defaults, the VA repays the lender a portion of the loan.

No VA home loan limits in 2020

“Removing the loan limits is huge for veteran and military buyers across the country, and it comes on the heels of another big year in VA lending,” says Chris Birk, director of education at Veterans United Home Loans. The VA guaranteed 624,544 loans in fiscal year 2019, a 2% increase over the prior fiscal year, according to data from the Department of Veterans Affairs.

“Veterans living or stationed in costlier real estate markets can stretch the zero-down buying power of their benefit in a way they never have before,” Birk says.

The removal of loan limits doesn’t mean unlimited borrowing power without a down payment. You’ll still need to have sufficient income and meet a lender’s credit requirements to qualify for the loan amount.

Loan limits will still apply in 2020 to veterans who have one or more active VA loans or have defaulted on a previous loan, Birk says.

Those VA loan limits are the same as the ones set by the Federal Housing Finance Agency on conforming loans. The limit in 2020 is $510,400 in a typical U.S. county and higher in expensive housing markets, such as San Francisco County.

If you’re subject to VA loan limits, the lender will require a down payment if the purchase price is above the loan limit. The exact down payment you will pay is determined by a formula that takes into account your entitlement and home price.

VA funding fee to increase

The VA funding fee you pay in 2020 will depend on your down payment amount and whether you’ve ever had a VA-backed loan before. If you haven’t, it’s a “first use” loan, and if you have, it’s a “subsequent use” loan. You can pay the fee upfront or roll the cost into the loan.