I have successfully originated over 200 VA Home loans in Kentucky. Put my experience to work for you. Call or text me today at 502-905-3708 or email me at Kentuckyloan@gmail.com-This website is not affiliated with the VA or any other government agency. NMLS #57916 Equal Housing Lender. Same Day Approvals, Fast Closings, and a Local Veteran offering VA Home Loans in Kentucky. Free Credit Report and Pre-Approvals NMLS# 57916 Joel Lobb Loan Originator, Company NMLS ID 1738461 . Equal Housing Lender

Louisville Kentucky VA Approved Condos for Jefferson County KY

Louisville and Jefferson County KY VA-approved condo guide for Kentucky veterans and real estate agents.

Louisville Kentucky VA Approved Condos for Jefferson County KY

If you are a Kentucky veteran, active-duty service member, or eligible surviving spouse looking at a condominium in Louisville, the first thing to confirm is simple: is the condo project acceptable for VA mortgage financing?

A VA loan can be one of the strongest mortgage programs available because it may allow qualified buyers to purchase with no down payment, no monthly private mortgage insurance, and competitive loan terms. However, condos add one extra layer of due diligence. The condominium project itself must be acceptable for VA financing before the loan can move forward smoothly.

Quick answer: Louisville veterans can use a VA loan to buy a condo in Jefferson County KY, but the condo project should be checked against VA approval records before contract, appraisal, and underwriting deadlines become an issue.

Why VA Condo Approval Matters in Kentucky

Buying a single-family home with a VA loan is usually more straightforward from a property-approval standpoint. Condos are different because the financial health, insurance coverage, ownership structure, legal documents, and management of the condominium project can affect VA eligibility.

That is why Kentucky homebuyers and real estate agents should verify the condo project early. Waiting until after the offer is accepted can create avoidable delays, especially if the condo is not already listed as approved.

VA Loan Benefits for Louisville Condo Buyers

No down payment may be required when the purchase price does not exceed the appraised value and the borrower qualifies.

No monthly private mortgage insurance is required on VA loans.

Seller-paid closing costs and concessions may help reduce cash needed to close.

VA loans may be more forgiving than conventional financing for qualified veterans, depending on credit, income, residual income, and overall risk profile.

VA eligibility can be used more than once, subject to entitlement and VA guidelines.

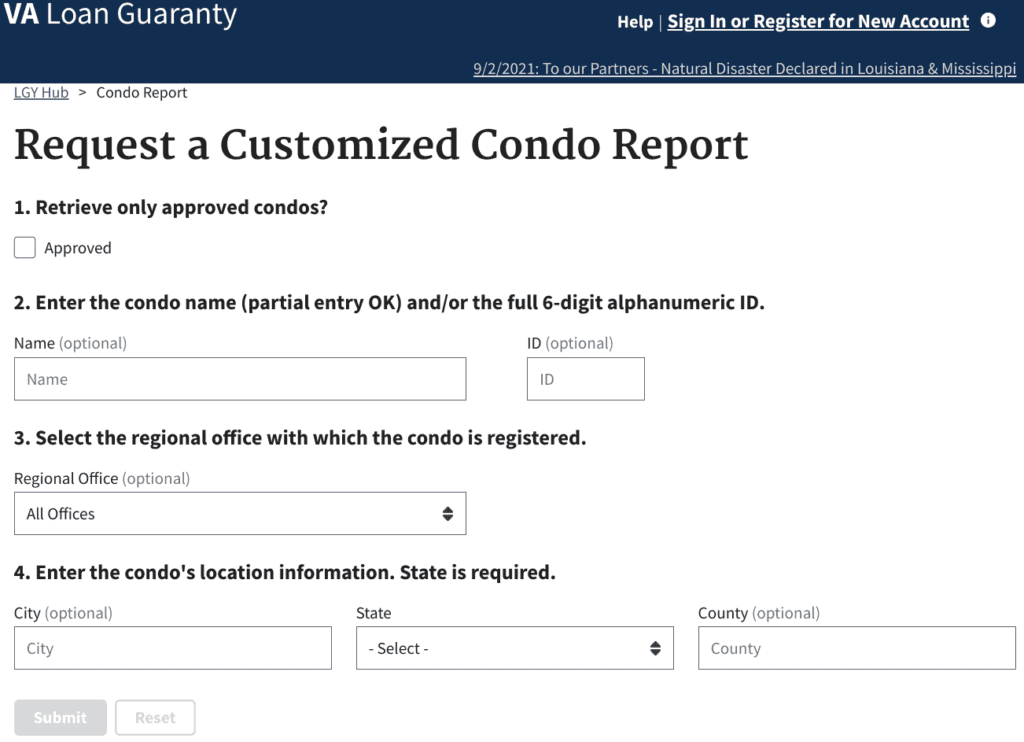

Before writing an offer on a condo, verify the project using the VA condo report or have your lender check it for you. The official VA condo report can be accessed here: VA Condo Report Search.

The list below is based on the Jefferson County KY VA-approved condo results provided for Louisville-area VA mortgage loan research. Condo approval status should always be re-verified before contract, appraisal, or final loan approval because records can change.

Condo Name

VA Condo ID

Record Type

ANDERSON PARK CONDOMINIUM

000004

Condo

ARBOR CREEK CONDOMINIUMS

H00212

Condo

ARBOR CREEK CONDOS II

H00306

Condo

AUTUMN TRACE CONDOMINIUM

H00282

Condo

BAXTER PLACE CONDOMINIUMS

H00309

Condo

BRADFORD COMMONS CONDO

H00319

Condo

BRADFORD COMMONS CONDOS

000001

Condo

BRITTANY POINTE CONDOMINI

005775

Condo

BROWNSBORO VILLAGE COURT

H00398

Condo

CARRINGTON GREENE COURTYARD

000012

Condo

CHAMBERLAIN SQUARE CONDO

H00614

Condo

COPPERSHIRE CONDOMINIUM

005613

Condo

COTTONWOOD CONDOMINIUM

H00053

Condo

CREEKWOOD TERRACE

H00095

Condo

CRESCENT CONDOS

VAC028

Condo

CROSSINGS @ COOPER CHAPEL

H00155

Condo

DARNELL MANOR CONDOMINIUM

H00368

Condo

DONARD PARK CONDOMINIUMS

000003

Condo

DORSEY HILLS CONDOMINIUM

H00199

Condo

DORSEY VILLAGE

005601

Condo

EAST HAMPTON

H00693

Condo

EVERETT PLACE CONDOMINIUM

005724

Condo

EVERGREEN POINT CONDO

H00637

Condo

FOREST PARK CONDOS

H00096

Condo

FOX HOLLOW CONDOMINIUM

H00634

Condo

GARDENS AT BAY RUN CONDO

H00639

Condo

GLENVIEW EAST

005674

Condo

GRAYSTONE MANOR

H00070

Condo

HARRODS LANDING CONDOMINI

H00464

Condo

HAWTHORNE POINTE CONDOS

H00134

Condo

HIGHWOOD

H00211

Condo

HIKES PARK TOWNHOMES

H00066

Condo

HITE AVENUE GARDENS

005801

Condo

INDIAN RIDGE CONDOMINIUMS

H00358

Condo

LAKEVIEW

VAC010

Condo

MAGNOLIA PLACE

005597

Condo

MANNER POINTE

000013

Condo

MERCANTILE GALLERY LOFTS

000015

Condo

MOSS CREEK CONDOMINIUM

H00294

Condo

PARK CENTRAL

VAC101

Condo

PARK LANE CONDOMINIUM

H00179

Condo

PINNACLE GARDENS

H00111

Condo

REGENCY THREE CONDOMINIUM

005892

Condo

RIVER POINTE PATIO HOMES CONDO

000017

Condo

SALEM SQUARE CONDOMINIUM

H00067

Condo

SHELBY CROSSING CONDOMINI

H00344

Condo

SHELBY CROSSING CONDOMINIUMS

000006

Condo

SOUTH HALL CONDOMINIUMS

005723

Condo

SPRING DRIVE CONDO

005656

Condo

SPRINGS OF GLENMARY

H00217

Condo

SPRINGS OF GLENMARY VLLGE

005612

Condo

ST ANTHONY'S LANDING

H00194

Condo

STONEHENGE CONDO

005602

Condo

SWAN POINTE CONDOMINIUMS

H00586

Condo

THE CLIFF VIEW TERRACE CO

H00587

Condo

THE COTTAGES @ MEADOWVIEW

H00182

Condo

THE FOUNTAINS CONDOMINIUM

H00171

Condo

THE GARDENS OF GLENMARY

H00272

Condo

THE GARDENS OF MONTICELLO

H00609

Condo

THE PARKVIEW CONDOMINIUMS

H00258

Condo

THE VILLAGE @ WILDWOOD

H00088

Condo

THE VILLAGE @INDIAN FALLS

H00143

Condo

THE VILLAGE OF WHITE OAKS

H00531

Condo

THE VILLAS OF STONY FARM

H00288

Condo

THE WOODS OF CRESCENT HIL

H00031

Condo

THE WOODS OF CRESCENT HIL

H00030

Condo

TIMBERWOOD II

000005

Condo

TREIS CONDOMINIUMS

H00058

Condo

VALHALLA VISTA CONDOMINIUMS

000024

Condo

VALLEY FARMS PATIO HOMES

000021

Condo

VILLAGE AT PRESTON CROSSI

H00504

Condo

VILLAGE AT WILDWOOD

H00125

Condo

WEMBERLY HILL GARDEN HOME

VAC143

Condo

WESTPORT GARDENS

000008

Condo

WESTPORT RIDGE CONDO

H00629

Condo

WINDSOR GATE CONDOMINIUM

H00262

Condo

WISTERIA LANDING CONDO

H00535

Condo

WOODMONT

H00156

Condo

WOODRIDGE LAKE PATIO HMS

H00092

Condo

WOODRIDGE LAKE TOWNHOMES

H00093

Condo

WOODS OF ST. ANDREWS

H00139

Condo

WOODSPOINTE

VAC074

Condo

WORTHINGTON GLEN CONDOS

H00162

Condo

WYNDEMERE

H00213

Condo

WYSTERIA LANDING CONDOMIN

H00351

Condo

YORKWOOD CONDO I

VAC013

Condo

YORKWOOD CONDO II

VAC016

Condo

How to Use This VA Condo List

Find the condo project name in the list.

Confirm the condo ID and project status in the VA condo report.

Ask the listing agent or HOA for current condo documentation if needed.

Have the lender verify borrower eligibility, residual income, credit, assets, and occupancy.

Do not order the VA appraisal until the condo eligibility path is clear.

What If the Louisville Condo Is Not on the VA Approved List?

If a condo project is not showing as VA approved, it does not automatically mean the buyer is dead in the water. It does mean the deal needs to be reviewed carefully before you assume VA financing will work. The lender may need to determine whether the project can be submitted for VA review and whether the timeline still works for the buyer, seller, agents, and closing date.

The practical reality is simple: if the condo is already VA approved, the transaction is usually cleaner. If the condo is not already approved, the file may need more documentation, more time, and more cooperation from the HOA or management company.

Important Questions Before a Veteran Writes an Offer on a Condo

Is the condo project currently VA approved?

Does the condo name match exactly in the VA condo report?

Is the project in Jefferson County, Louisville, or another Kentucky county?

Are there pending lawsuits, insurance issues, budget problems, or high delinquency rates?

Will the HOA or management company provide documents quickly?

Does the buyer qualify for the VA loan based on income, credit, residual income, and debts?

Is the unit intended as the buyer’s primary residence?

Topical Kentucky VA Loan Resources

For more Kentucky mortgage guidance, review these related resources:

Need Help Buying a VA-Approved Condo in Louisville KY?

If you are a Kentucky veteran looking at a condo in Louisville or Jefferson County, get the condo checked before you waste time, money, or appraisal fees. I can review the condo project, your VA eligibility, credit, income, and cash-to-close numbers before you write the offer.

Frequently Asked Questions About VA Approved Condos in Louisville KY

Can I buy a condo in Louisville with a VA loan?

Yes. Eligible veterans, service members, and qualifying surviving spouses may use a VA mortgage loan to buy a condo when the borrower qualifies and the condo project is acceptable for VA financing.

Does a Louisville condo have to be VA approved?

The condo project should be checked through VA resources before relying on VA financing. If the project already appears as approved, that can help reduce the risk of loan delays.

Are FHA-approved condos automatically VA approved?

No. FHA condo approval and VA condo approval are not the same. Always verify the project through VA resources before assuming it works for a VA loan.

What are the biggest VA loan benefits for Kentucky condo buyers?

Major VA loan benefits may include no down payment, no monthly private mortgage insurance, competitive loan terms, and limited closing costs. Borrowers must still meet VA and lender requirements.

Who should verify the VA condo status?

The lender should verify the VA condo status early. Real estate agents should also confirm the project name and HOA contact information as soon as the buyer shows interest in a condo.

Joel Lobb, Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae. EVO Mortgage. Helping Kentucky Homebuyers Since 2001. NMLS #57916 | Company NMLS #1738461.

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval, VA eligibility, property approval, underwriting, and program requirements. This site is not endorsed by or affiliated with FHA, VA, USDA, KHC, or any government agency.

We recognize that our veterans provide an invaluable service. As such, we fully support home loan programs guaranteed by the U.S. Department of Veterans Affairs that are specifically designed to support veterans and their families. Although there are many perks that come with a VA versus conventional loan, a conventional loan offers some benefits that are not available through a VA loan. Let’s compare both of these loans to determine which type is best for you.

What Is a VA Loan?

A VA loan is a great benefit for those who have contributed to their country by serving in a military capacity. It is intended to give veterans access to home loans with advantageous terms. The federal government guarantees a portion of the loan, enabling veterans to qualify for more favorable terms when working with private lenders. The VA loan program was designed to offer long-term financing to eligible American veterans or their surviving spouses (provided they do not remarry). In addition to helping veterans buy, build, repair, retain or adapt a home for their own personal occupancy, it was also created to help veterans purchase properties with no down payment.

What Are the Pros and Cons of a VA Loan?

There are a myriad of reasons why a veteran would want to choose a VA Loan. A VA loan is federally backed. It also offers lower interest rates and fees than are usually associated with home lending costs. The only cost required by VA loans is a funding fee of one-half of one percent of the total loan amount. And that may be paid in cash or rolled into the loan amount. However, there are some factors you will want to take into consideration when deciding if a VA Loan fits your home buying needs.

No Private Mortgage Insurance (PMI) or Down Payment Necessary. Eliminating these costs can significantly reduce total housing expenses. Typically, a lender requires a 20% down payment. Borrowers who are unable to put down 20% are considered riskier and as a result must pay a PMI, which is typically 0.58% to 1.86% of the original loan amount per year on a conventional home loan. Because VA loans are federally backed, lenders do not have to worry about the house going into foreclosure and are able to offer a mortgage plan that does not require a PMI without a down payment.

Interest Rate Reduction Refinance Loan (IRRRL): IRRRL loans are typically used to reduce the borrower’s interest rate or to convert an adjustable rate mortgage (ARM) to a fixed rate mortgage. Veterans may seek an IRRRL only if they have already used their eligibility for a VA loan on the same property they intend to refinance. However, your lender can use the VA’s email confirmation procedure for interest rate reduction refinance in lieu of a certificate of eligibility. Additionally, an IRRRL can reduce the term of your loan from 30 years to 15 years. An IRRRL offers great potential refinancing benefits for vets, but be sure to check the facts to fully understand IRRRL stipulations and avoid an increase in other expenses.

Native American Direct Loan (NADL) Program: This program was designed to help Native American veterans or spouses of Native American veterans buy, build, or improve a home on federal trust land. This loan also qualifies veteran home buyers for the benefits listed above, in addition to limited closing costs and a low-interest, 30-year, fixed mortgage. Plus, this is a reusable benefit, which means you can get more than one NADL to buy, build or improve another residence in the future.

Adapted Housing Grants. To qualify for an adapted housing grant, veterans must own or will own the home they are looking to buy, and have a qualifying service-connected disability. This loan is a great option for veterans who are seeking to make home modifications to accommodate a disability. Currently, if you qualify for a grant, you can get up to a maximum of $100,896.

Funding Fee and Closing Fees. A VA loan funding fee may vary depending on whether you put a down payment on a house. Depending on if you are a first-time VA loan borrower or making a subsequent loan purchase, a funding fee can range from roughly 1.5% on a down payment of 10% or more to 3.5% on downpayment of 5% or less. Closing fees on a house can range from 2–5%. These are definitely costs you will want to consider when determining how much home you can afford.

Property Eligibility. A VA loan may not be applied to purchasing a farm, property in a foreign country, land or an investment property/second home.

What Is a Conventional Loan and How Does It Compare to a VA Loan?

Conventional mortgage loans are some of the most commonly used housing loans. However, they are not guaranteed by the federal government, so borrowers who are not putting 20% on a down payment will likely incur the costs of a PMI. Unlike government-backed loans, conventional loans are not limited by geographic constraints. They can offer more flexibility than a government-insured loan but may be harder to qualify for and require a higher credit score (at least 620).

For veterans, the main advantage of this loan compared to a VA loan is that it provides options that may fit a wider range of home-buying needs. Here are some benefits of conventional loans:

Usable for purchases, rate and term refinances and cash-out refinances

Allow cash out up to 80% of your home’s value

Debt to income ratios allowable up to 50%

Usable for primary, secondary or investment properties

Applicable for condos, single family homes and up to 1–4 unit properties

First-time home buyer programs with as little as 3% down payments

Options both with and without escrows or impounds

Request a Customized VA Approved Condo Report for Kentucky VA Mortgage Loans. See link below

{kind=link}