Farm Loans: Kentucky VA Home Loans Overview

Kentucky VA Home Loans

Can You Buy a Farm in Kentucky With a VA Home Loan?

Yes, in many cases. The VA Home Loan benefit can be used to purchase a farm property in Kentucky when there is a residence on the land and the Veteran will live in that home as a primary residence. VA loans are for residential purposes and cannot be used to buy a business.

Kentucky eligibility rules for “farm” properties

- There must be a residential dwelling on the land.

- The Veteran must occupy the home as their primary residence.

- The loan must be primarily for a residence, not for purchasing a business or commercial operation.

- Properties that are primarily commercial farms (business-first) may not qualify.

Practical Kentucky example: A home on acreage in areas like Oldham County, Shelby County, Spencer County, Hardin County, or rural Warren County can be workable when comps support residential use and the home is the primary purpose of the purchase.

Appraisal, acreage, and outbuildings in Kentucky

- VA does not set a maximum number of acres.

- Acreage typically isn’t an issue if comparable sales in the area sold primarily for residential use.

- Outbuildings and improvements like barns, sheds, corrals, stables, and pastures may be considered in value as residential-related improvements.

- The VA valuation must not include livestock, crops, or farm equipment/supplies.

This is why “comps” matter in Kentucky: if the closest comparable sales are residential-with-acreage (not commercial ag sales), underwriting is usually more straightforward. :contentReference[oaicite:1]{index=1}

Using farm income to qualify

If some or all of the income needed to qualify comes from farming operations, the VA requires verification that the Veteran has the ability and experience to operate the farm. :contentReference[oaicite:2]{index=2}

- Expect documentation similar to self-employment (history, consistency, and ability to continue).

- We’ll focus on stable, documentable qualifying income—not one-time or speculative income.

VA vs FHA vs USDA acreage comparisons (Kentucky)

The real-world issue usually isn’t a hard acreage cap. It’s whether the property is primarily residential, whether comps support the value, and whether there are income-producing features that make the property look like a business purchase.

| Program | Does it have a strict acreage limit? | What underwriters/appraisers care about | Common Kentucky “deal killers” |

|---|---|---|---|

| VA | No stated acre limit. | Primary residence requirement, residential comps, no value for livestock/crops/equipment; residential-only valuation for farmland portion. | Property is primarily a working commercial farm; comps are commercial ag sales; value tied to business assets. :contentReference[oaicite:3]{index=3} |

| FHA | No universal acre cap; must be typical for the area and primarily residential. | Residential highest-and-best use, marketability, and appraisal support; avoid properties that function like a commercial operation. | Commercial ag use dominates; unique specialty improvements without residential market support. |

| USDA (Guaranteed) | No specific site size/acreage limit, but it must be predominantly residential. | Predominantly residential character; the property must not include buildings principally used for income-producing purposes. | Income-producing land or facilities used primarily for ag/commercial enterprise; property fails rural eligibility mapping. :contentReference[oaicite:4]{index=4} |

Steps to a VA home loan (including farm properties)

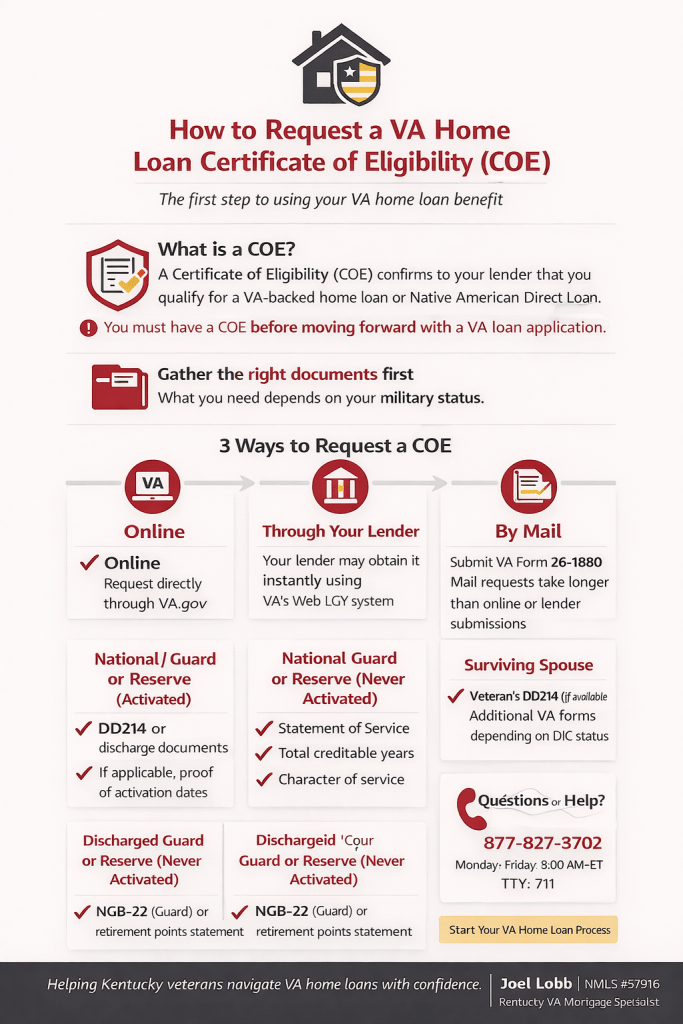

- Get your Certificate of Eligibility (COE). Lenders can typically retrieve this electronically.

- Get preapproved with a VA-experienced lender and connect with a Realtor.

- Choose a home and sign a purchase agreement that includes a VA financing contingency.

- Order the VA appraisal and clear final underwriting conditions for closing.

If you’re looking at acreage properties in Kentucky, send the listing early. The earlier we evaluate comps and “residential vs business” risk, the fewer surprises you’ll have later.

FAQ: Kentucky VA farm properties

Often, yes, if the property is primarily residential and the improvements contribute to residential market value. The VA valuation cannot include livestock, crops, or farm equipment. :contentReference[oaicite:5]{index=5}

No stated acreage limit. The focus is on residential use and comparable sales support. :contentReference[oaicite:6]{index=6}

Potentially, yes. VA requires documentation and verification of ability/experience as a farm operator when farming income is used to qualify. :contentReference[oaicite:7]{index=7}

When it’s primarily a business purchase (commercial farm), or value depends on business assets like livestock, crops, or equipment.

One-page guide

VA Farm Property Eligibility (Kentucky)

Use this checklist before writing an offer on acreage property.

Primary residence required Residential purpose only Acreage not capped- Home on the land

- Veteran occupies as primary residence

- Property is primarily residential

- Comparable sales support residential-with-acreage value

- Livestock

- Crops

- Farm equipment or supplies

- Barns, sheds, corrals, stables

- Pastures and typical rural improvements

- Farm income, if documentable and experience is verified

- Commercial farm operation is the main purpose

- Value relies on business assets

- No good residential comps (only ag/commercial sales)

You must be logged in to post a comment.