How to Request a VA Home Loan COE

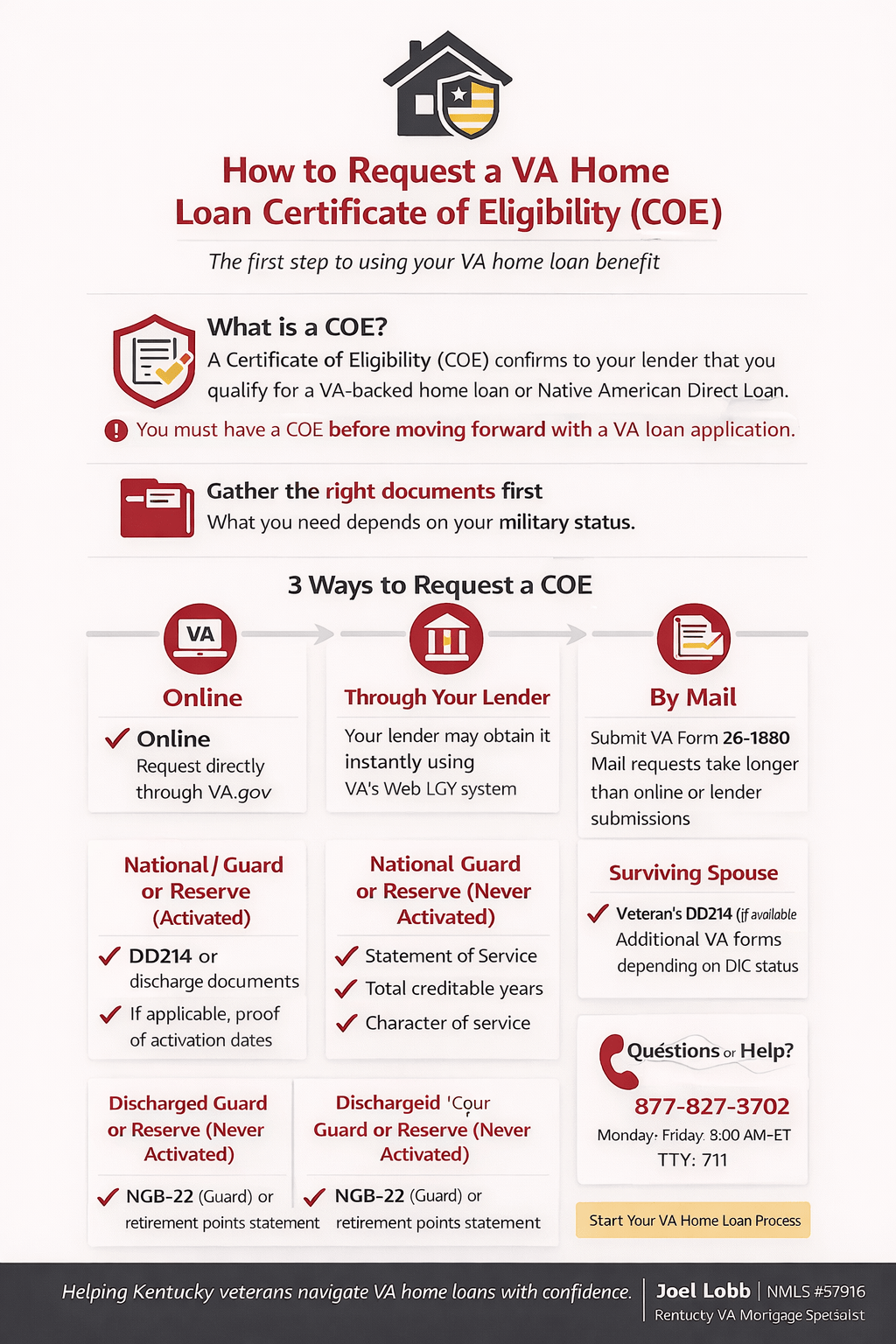

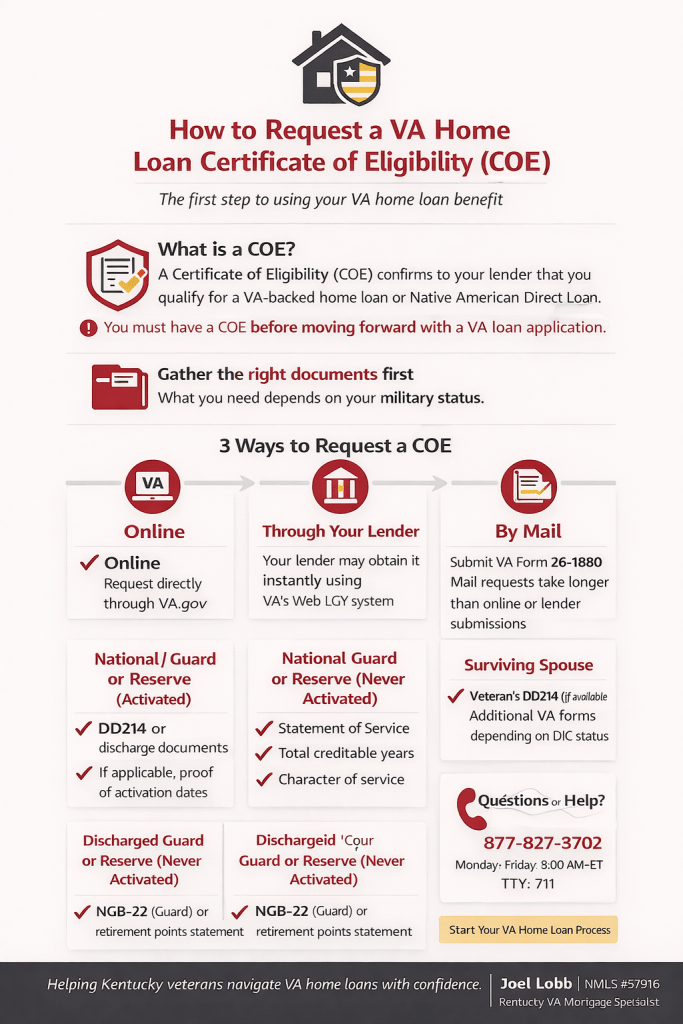

How to Request a VA Home Loan Certificate of Eligibility (COE)

A Certificate of Eligibility (COE) is the first step in getting a VA-backed home loan or Native American Direct Loan. The COE confirms to your lender that you qualify for the VA home loan benefit and are eligible to move forward with a VA mortgage.

Once your COE is issued, you can choose a loan type and continue through the rest of the VA loan application process.

How to Prepare Before You Request a COE

Before starting your COE request, gather the documents you’ll need. The required paperwork depends on your military service status.

Veteran

- Copy of your discharge or separation papers (DD214)

Active-Duty Service Member

You’ll need a Statement of Service signed by your commander, adjutant, or personnel officer. The statement must include:

- Your full name

- Your Social Security number

- Your date of birth

- The date you entered active duty

- The duration of any lost time

- The name of the command providing the information

Current or Former Activated National Guard Member

- Copy of your DD214 or other discharge documents

-

If applicable, proof of activation dates, such as:

- DD214 showing qualifying 32 USC activation sections

- An annual retirement points statement

- DD220 with accompanying orders

Current or Former Activated Reserve Member

- Copy of your DD214 or other discharge documents

Current National Guard or Reserve Member Who Has Never Been Activated

You’ll need a Statement of Service signed by your commander, adjutant, or personnel officer showing:

- Your full name

- Your Social Security number

- Your date of birth

- The date you entered duty

- Your total number of creditable years of service

- The duration of any lost time

- The name of the command providing the information

Discharged National Guard Member Who Was Never Activated

- Report of Separation and Record of Service (NGB Form 22) for each period of service

- Retirement Points Statement (NGB Form 23) and proof of character of service

Discharged Reserve Member Who Was Never Activated

- Copy of your latest annual retirement points statement

- Proof of honorable service

Surviving Spouse

If you qualify as a surviving spouse, you’ll typically need the Veteran’s DD214 (if available). Additional VA forms may be required depending on whether you receive Dependency and Indemnity Compensation (DIC).

How to Request a COE

You can request a Certificate of Eligibility in one of three ways.

Option 1: Online

Request your COE directly through VA.gov. This is often the fastest option.

Option 2: Through Your Lender

Your lender may be able to obtain your COE instantly using the VA’s Web LGY system. Ask your lender if they can request the COE on your behalf.

Option 3: By Mail

Complete VA Form 26-1880 (Request for a Certificate of Eligibility) and mail it to the address listed on the last page of the form. Mail requests typically take longer than online or lender submissions.

What Happens After You Request a COE?

- The VA reviews your request and issues a decision

- You can check the status of your COE request online

Next Steps After Your COE Is Issued

Requesting a COE is only part of the VA loan process. After your COE is issued:

- Your lender orders a VA appraisal to assess market value

- Your lender reviews your income, credit, and documentation

- If approved, a title company is selected and closing is scheduled

Questions About the VA Loan Process?

If you have questions your lender can’t answer, you can contact a VA home loan representative at 877-827-3702 (TTY: 711), Monday through Friday, 8:00 a.m. to 6:00 p.m. ET.

Kentucky VA Loan Assistance

If you’re buying a home in Kentucky, I can help you determine which documents apply to your service history and coordinate with your lender to request the COE when eligible.

Text or call: 502-905-3708

Joel Lobb – NMLS #57916

Informational only. Not affiliated with or acting on behalf of the U.S. Department of Veterans Affairs. Not a commitment to lend. Subject to credit approval and program guidelines. Kentucky only.

How to request a VA home loan Certificate of Eligibility (COE)

Learn how to request a VA home loan Certificate of Eligibility (COE). This is the first step in getting a VA-backed home loan or Native American Direct Loan. It confirms for your lender that you qualify for the VA home loan benefit.

1 How do I prepare before I start a COE request?

Select the description here that matches you best to find out what you’ll need.

You’ll need a copy of your discharge or separation papers (DD214).

You’ll need a statement of service—signed by your commander, adjutant, or personnel officer—showing:

- Full name & Social Security number

- Date of birth & Date you entered duty

- Duration of any lost time

- Name of the command providing the information

You’ll need a copy of your DD214 or other discharge documents.

Note: If you have 90+ days of active service (with 30 consecutive), provide a document showing activation date (DD214, annual point statement, or DD220 with orders).

You’ll need the Veteran’s discharge documents (DD214) if available.

If receiving DIC:

Submit VA Form 26-1817 (Request for Determination of Loan Guaranty Eligibility).

If NOT receiving DIC:

Submit VA Form 21P-534EZ, Marriage License, and Veteran’s Death Certificate.

2 How do I request a COE?

Online

The fastest way to apply through the VA.gov portal.

Via Lender

Most lenders can access “Web LGY” to get it for you instantly.

By Mail

Fill out VA Form 26-1880 and mail to your regional center.

What happens next?

The VA will review your request and notify you of the decision. Once you have your COE, the lending process typically follows these steps:

VA Appraisal

The lender requests an assessment to estimate the house’s market value.

Review & Underwriting

Lenders review your credit, income, and the appraisal report.

Closing

Ownership is transferred at a title company or similar entity.

You must be logged in to post a comment.