Kentucky VA Mortgage Loan Guide for Home Buyers

You’ve come to the right place if you’re a Kentucky veteran or an active military member. You are searching for VA loan information in Kentucky. VA loans offer unique benefits and flexibility, but many myths and misconceptions surround them. Let’s debunk these myths now. We will give precise information to help you make informed decisions when applying for a Kentucky VA mortgage loan.

Common Myths About Kentucky VA Loans

Myth #1: VA Loans Are Hard to Qualify For

Fact: VA loans have more flexible credit and income requirements than conventional loans. They allow higher debt-to-income (DTI) ratios and lenient credit score thresholds.

- No Minimum Credit Score: The VA does not set a minimum score, but most lenders require 620. Some go as low as 580, though approvals for lower scores can be more challenging.

Myth #2: VA Loans Need a Down Payment

Fact: VA loans do not require a down payment for loans at or below the local conforming limit.

- Jumbo Loans: For higher loan amounts, down payment requirements depend on your VA entitlement:

- Full Entitlement: No down payment required.

- Partial Entitlement: Down payment needed to meet the 25% guarantee.

Myth #3: VA Loans Require PMI (Private Mortgage Insurance)

Fact: Unlike conventional loans, VA loans do not require PMI.

- This means you save monthly on your house payment which would otherwise be added to your mortgage payment.

- Note: Kentucky VA loans do have a funding fee, which can be waived for eligible disabled veterans.

Kentucky VA Loan Refinancing Options

Myth #4: You Can’t Refinance a VA Loan

Fact: VA loans are easier to refinance compared to conventional loans, thanks to programs like:

- VA IRRRL (Streamline Refinance): Reduces your interest rate with minimal paperwork. No credit check or appraisal required.

- VA Cash-Out Refinance: Allows you to access your home’s equity, subject to an appraisal and credit check.

VA Loan Entitlement & Multiple VA Loans

Myth #5: You Can Only Have One VA Loan

Fact: You can have multiple VA loans as long as you have remaining entitlement.

- Entitlement Coverage:

- Loans under $144,000: VA guarantees up to $36,000.

- Loans over $144,000: VA guarantees up to 25% of the loan amount.

- Note: If you’ve used a part of your entitlement for another loan, you may need to make a down payment. This applies to extra loans.

Myth #6: You Can Only Use a VA Loan Once

Fact: You can use your VA loan benefits unlimited times throughout your life.

- To reuse the benefit, you must either:

- Pay off your current VA loan, or if enough entitlement is left on your COE, and you qualify with both house payments on the dti and residual income test, you may be able to have two va loans active at the same time

- Sell the property and restore your entitlement.

Assumability and Other Uses of VA Loans

Myth #7: VA Loans Are Not Assumable

Fact: VA loans are assumable, meaning another buyer can take over your VA loan.

- Benefits: This is especially valuable in a low-interest-rate environment.

- Requirements for Buyers:

- Acceptable credit history and DTI ratio.

- Residual income meeting VA guidelines.

Myth #8: You Can’t Buy Land with a VA Loan

Fact: While VA loans don’t cover land purchases alone, they allow you to:

- Buy land and immediately build a home on it with a VA construction loan.

- Use a conventional loan to buy land, then refinance into a VA loan after building your home.

Myth #9: You Can’t Build a House with a VA Loan

Fact: VA construction loans allow you to build a home, as long as the builder is VA-approved. Upon completion, you can refinance the loan into a permanent VA mortgage.

Myth #10: VA Loans Are Only for Home Purchases

Fact: VA loans can also be used for home improvement projects.

- The VA Energy Efficiency Mortgage Program allows you to add up to $6,000 for energy-efficient upgrades. These include solar heating, insulation, and storm windows.

Benefits of Kentucky VA Loans

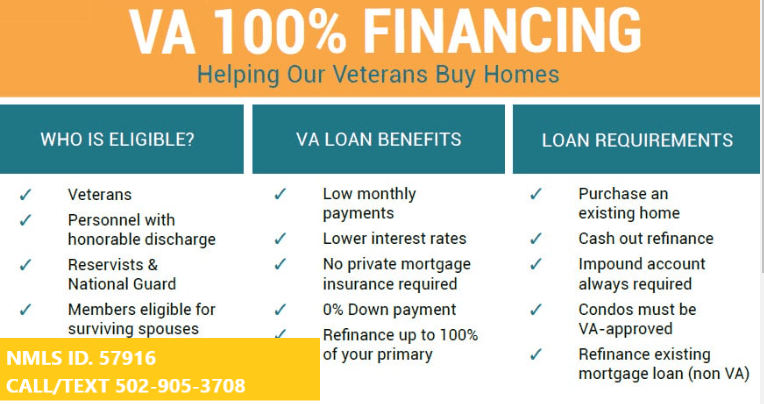

- 100% Financing: No down payment required.

- No PMI: Reduces your monthly mortgage payment.

- Low Closing Costs: Sellers can pay closing costs and prepaid, up to 4% and even payoff borrower’s debts to qualify for a mortgage loan above the 4% threshold for seller concessions

- Flexible Credit Guidelines: Perfect for veterans with past credit issues. No minimum credit score but wight most heavily the last two years on credit report. No foreclosure, Chapter 7 bankruptcies the last two years

- Assumability: Allows buyers to take over existing VA loans.

Get Started with Your Kentucky VA Loan Today!

As a mortgage loan officer, I have over 20 years of experience. I’ve helped more than 1,300 Kentucky families buy or refinance their homes. Whether you’re buying your first home, upgrading, or refinancing, I’m here to make the process smooth and stress-free.

Contact Information:

📞 Text/Call: 502-905-3708

📧 Email: kentuckyloan@gmail.com

🌐 Website: www.mylouisvillekentuckymortgage.com

Joel Lobb

Mortgage Loan Officer – Specialist in Kentucky VA, FHA, USDA, and KHC Loans

- NMLS ID: 57916

- Address: 10602 Timberwood Circle, Louisville, KY 40223

Let’s make your homeownership dreams a reality! Reach out today to learn more about VA loan options in Kentucky.

“VA loans in Kentucky,” “Kentucky VA mortgage,” and “VA home loans for veterans in Kentucky.”

You must be logged in to post a comment.