I have successfully originated over 200 VA Home loans in Kentucky. Put my experience to work for you. Call or text me today at 502-905-3708 or email me at Kentuckyloan@gmail.com-This website is not affiliated with the VA or any other government agency. NMLS #57916 Equal Housing Lender. Same Day Approvals, Fast Closings, and a Local Veteran offering VA Home Loans in Kentucky. Free Credit Report and Pre-Approvals NMLS# 57916 Joel Lobb Loan Originator, Company NMLS ID 1738461 . Equal Housing Lender

Category: kentucky va mortgage refinance guidelines

How to Calculate Residual Income for a Kentucky VA Home Loan Approval (2026)

Kentucky veterans using a VA home loan must meet minimum residual-income requirements. Residual income measures the monthly funds left over after housing costs, taxes, and all recurring bills. It is a core underwriting factor that determines whether a VA loan can be approved, especially when debt-to-income ratios are higher or credit depth is limited.

This guide breaks down how residual income works, how to calculate it correctly, and the 2026 minimums required for Kentucky VA buyers.

Residual income is the amount of money left after subtracting all monthly obligations from the borrower’s gross monthly income. The VA establishes region-based minimums to ensure borrowers have enough remaining funds to cover essentials such as food, transportation, clothing, utilities, and other living expenses.

Even if a borrower has a high credit score and a strong DTI ratio, the loan cannot be approved without meeting minimum residual-income thresholds.

How Kentucky Lenders Calculate VA Residual Income

Start with gross monthly income for all occupying borrowers.

Subtract federal, state, and local taxes based on paystubs/W-2 withholding tables.

Subtract the proposed housing payment (PITI): principal, interest, taxes, insurance, HOA, and any maintenance fees.

Subtract all recurring debts:

auto loans

student loans

credit card minimums

child support / alimony

personal loans or installment debt

Subtract estimated utilities/maintenance. Many lenders use approximately $0.14 per square foot of heated living space.

The figure remaining after all these deductions is the official VA residual income.

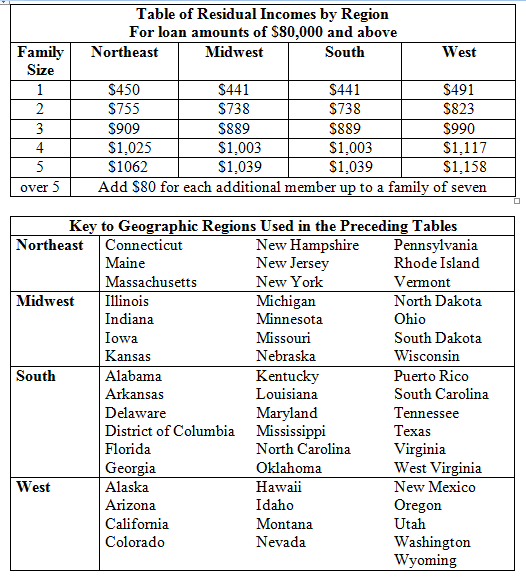

2026 VA Residual Income Requirements for Kentucky (South/Midwest Region)

Household Size

Minimum Residual Income

1 Person

$441

2 Persons

$738

3 Persons

$889

4 Persons

$1,003

5 Persons

$1,039

Each Additional Person

Add $80

If debt-to-income ratio exceeds 41 percent, underwriters typically require 20 percent more than the baseline residual number.

Why Residual Income Matters More Than DTI

Residual income is one of the strongest predictors of loan performance in the VA program. Borrowers who meet or exceed the residual-income benchmark show significantly higher repayment success rates — even when credit scores are less than perfect or DTI ratios appear high.

If the loan does not meet residual income, the file cannot be approved without compensating factors or structural changes to qualifying income or household composition.

Free Help Calculating Residual Income

If you want, I can run a complete residual-income analysis for you or your buyer using up-to-date 2026 VA guidelines.

Looking to buy a home in Kentucky? VA loans could be your ticket to affordable homeownership. These loans are available to veterans, active-duty service members, and even some surviving spouses.

They’re especially popular because they offer perks like no down payment and competitive interest rates. Whether you’re eyeing a property in Louisville, Lexington, or near Fort Knox, a VA loan can make the process smoother. Plus, Kentucky’s got some great regional benefits for veterans that you might want to check out. Let’s dive into what makes Kentucky VA mortgage lenders a top choice for many.

Key Takeaways

VA loans in Kentucky offer no down payment options, making homeownership more accessible.

Veterans and active-duty members can benefit from competitive interest rates and flexible credit requirements.

Kentucky offers regional benefits for veterans, enhancing the appeal of VA loans in areas like Louisville and Lexington.

Understanding the eligibility criteria, including service and credit score requirements, is crucial for a successful application.

Working with a VA-approved lender simplifies the loan process, ensuring veterans get the most out of their benefits.

Understanding Kentucky VA Mortgage Lenders

Key Features of VA Loans in Kentucky

VA loans in Kentucky come with some pretty sweet perks. First off, there’s the zero down payment. You can get into a home without having to save up a big chunk of cash. Plus, you don’t have to worry about private mortgage insurance (PMI), which is a relief on your monthly bills. Interest rates are generally lower too, which is always a win. These loans are backed by the government, giving lenders more confidence to offer better terms.

How VA Loans Differ from Conventional Loans

VA loans differ from conventional loans in several ways. The most obvious is the no down payment requirement, which is a game-changer for many. Conventional loans usually need at least 3-5% down. VA loans also have more lenient credit score requirements, which means you might qualify even if your credit isn’t perfect. On the flip side, VA loans come with a funding fee. This fee helps keep the program running. However, there are exemptions for some veterans.

Benefits of Choosing a Kentucky VA Lender

Picking a Kentucky VA lender has its own set of benefits. Local lenders understand the state’s housing market, which can be a big help in finding the right home. They’re also familiar with any state-specific requirements or benefits, like tax exemptions for disabled veterans. When you work with someone who knows the local scene well, the whole process becomes smoother. It also becomes less stressful.

Kentucky VA lenders offer a unique blend of local expertise and specialized loan products that can make homeownership more accessible for veterans and their families.

Eligibility Criteria for VA Loans in Kentucky

Service Requirements for Veterans

To qualify for a VA loan in Kentucky, veterans and active-duty service members need to meet certain service requirements. Typically, this involves a minimum period of active duty service, which varies depending on when you served. For those who served during wartime, at least 90 consecutive days of active service is required. During peacetime, the requirement extends to 181 days. National Guard members and reservists must have completed six years of service. If they were called to active duty, the same active duty requirements apply.

Credit Score and Financial History

While the VA does not set a minimum credit score, lenders often have their own requirements. In Kentucky, many lenders look for a credit score of at least 620. However, some may require a higher score depending on other financial factors. It’s crucial to maintain a solid financial history, including timely bill payments and manageable debt levels. A strong credit profile can significantly enhance your loan approval chances.

Necessary Documentation for Application

When applying for a VA loan, you’ll need to gather several key documents. These include:

Certificate of Eligibility (COE): This is a must-have document that verifies your eligibility for a VA loan. You can obtain it through the VA or with the help of your lender.

Proof of Income: Lenders will need evidence of your income. You can show this through pay stubs, Last two years tax returns, and last two years W-2 forms.

Identification: A valid driver’s license or government-issued photo ID is necessary.

Preparing these documents ahead of time can streamline your application process, making it easier to secure your VA loan.

Remember, VA loans are specifically for primary residences, so they can’t be used for vacation homes or investment properties. Ensure all your paperwork is accurate and up-to-date to avoid any delays.

Exploring VA Loan Options in Kentucky

VA Purchase Loans for First-Time Buyers

If you’re a first-time homebuyer in Kentucky, the VA Purchase Loan might just be your ticket to homeownership. This loan is specifically designed for veterans and service members. It offers competitive rates. The big perk is no down payment. It’s a great way to get into a new home without the usual financial hurdles.

Here’s what makes the VA Purchase Loan stand out:

No Down Payment Required: This is a major advantage, making homeownership more accessible.

Competitive Interest Rates: VA loans often have lower rates compared to conventional loans.

Limited Closing Costs: This keeps the upfront costs much lower.

Streamline Refinance Options

The Streamline Refinance is a fantastic option for those already with a VA loan. Known as IRRRL, it stands for Interest Rate Reduction Refinance Loan. It’s all about reducing your interest rate and monthly payments with minimal hassle.

Benefits of the Streamline Refinance include:

No Appraisal Required: This speeds up the process significantly.

No Income Verification: Makes it easier to qualify.

Little to No Out-of-Pocket Costs: You can often roll the costs into the loan.

Cash-Out Refinance Opportunities

The VA Cash-Out Refinance is perfect if you need to tap into your home’s equity. This loan allows you to refinance your mortgage. You can use it for home improvements, paying off debts, or unexpected expenses. It helps you access cash when needed.

Key features of the Cash-Out Refinance:

Up to 100% of Your Home’s Value: This allows more flexibility in how much cash you can access.

Refinance Any Existing Loan: Not just limited to VA loans.

Great for Home Improvements: Use the funds to increase your home’s value or tackle necessary repairs.

Considering a VA loan option? If you’re facing challenges with your home loan payments, reach out to a VA loan technician. They can assist you in finding the best path forward. They’re just a call away at 50-905-3708.

Navigating the Kentucky VA Loan Process

Steps to Secure a VA Loan

Getting a VA loan in Kentucky isn’t as complicated as it might seem. Here’s a quick rundown of the steps you’ll need to take:

Get Your Certificate of Eligibility (COE): This is your golden ticket. You’ll need to grab this from the VA to prove you’re eligible. You can apply online, through your lender, or by mail.

Find the Right Lender: Not all lenders are created equal. Make sure you pick one that’s VA-approved and has experience with VA loans.

Pre-Qualification: Sit down with your lender and figure out how much you can borrow. This will help you narrow down your home search.

House Hunting: With your pre-qualification in hand, start looking for your new Kentucky home. A real estate agent can be a big help here.

Appraisal and Underwriting: The lender will order a VA appraisal to ensure the property is worth the purchase price. Then, they’ll underwrite your loan to check everything is in order.

Closing the Deal: Once everything checks out, you’ll close on your loan and get the keys to your new home.

Working with a VA-Approved Lender

Choosing a lender who knows the ins and outs of VA loans is crucial. They’ll guide you through the process and help avoid any potential hiccups. Guidance through the VA loan process is key to a smooth experience, especially for first-timers.

Understanding the Appraisal Process

The VA appraisal is not just a formality. It ensures the house is safe, sound, and worth the money you’re borrowing. An appraiser, assigned by the VA, will check the property’s value and condition. If issues arise, you might need to renegotiate with the seller or find another property.

The VA loan process, while detailed, offers a structured path to homeownership for veterans and active-duty members in Kentucky. With zero-down payment options and competitive rates, it’s a fantastic route to owning a home.

Regional Insights: VA Loans Across Kentucky

VA Loan Opportunities in Louisville and Lexington

In the bustling cities of Louisville and Lexington, veterans have access to a variety of VA loan opportunities. These areas boast a vibrant housing market with a range of options from historic homes to modern condos. VA loans are particularly beneficial here due to their no-down-payment requirement, making homeownership more accessible. Veterans seeking to settle in these urban hubs can enjoy the cultural amenities and economic opportunities these cities offer.

Fort Knox and Fort Campbell Housing Options

VA loans offer a practical solution for those stationed at or near Fort Knox. They also assist those near Fort Campbell in finding suitable housing. These military installations are surrounded by communities that understand the unique needs of military families. Housing options range from on-base facilities to nearby suburban neighborhoods. A VA loan can simplify the transition for military personnel. It ensures they have a stable and supportive environment for their families.

Benefits for Veterans in Northern Kentucky

Northern Kentucky offers a quieter lifestyle with the benefit of proximity to Cincinnati, Ohio. Veterans in this region can use the VA loan program. They can purchase homes in areas known for their scenic beauty. These areas also have a lower cost of living. The community support for veterans in Northern Kentucky is strong, with various programs aimed at easing the home buying process. Navigating the VA loan process in this area can be straightforward with the right guidance. This allows veterans to enjoy both financial and community benefits.

Kentucky’s diverse regions offer unique opportunities for veterans considering a VA loan. The lively city life in Louisville provides excitement. The peaceful suburbs near Fort Knox offer tranquility. There’s a place for every veteran to call home.

Financial Considerations for Kentucky VA Loans

Understanding VA Loan Limits and Entitlements

In Kentucky, VA loan limits aren’t really limits anymore if you’ve got your full entitlement. This means you can borrow as much as your lender thinks you can handle without needing a down payment. But if you don’t have your full entitlement, those limits still matter. As of now, the limit is $806,500 for all counties in Kentucky. So, if you’re buying a home and lack full entitlement, you must cover the gap with a down payment.

Impact of Property Taxes on VA Loans

Property taxes can be a big deal for VA loan holders in Kentucky. If you’re a veteran who’s totally disabled, you might get a property tax exemption up to $39,399 on your main home. Veterans over 65 years old also qualify for this exemption. That’s a nice chunk of change saved. But if you’re not exempt, property taxes will be part of your monthly mortgage payment, and that can add up.

Funding Fees and Exemptions for Veterans

Most veterans will have to pay a funding fee in Kentucky, but there are some exceptions. If you’re a veteran receiving compensation for a service-related disability, you might be off the hook for this fee. It’s a good idea to check with your loan officer to see what applies to you. This fee helps keep the VA loan program going, but it’s definitely something to factor into your budget.

For veterans, understanding the financial ins and outs of a VA loan in Kentucky can make homebuying a smoother ride. Knowing about loan limits, property taxes, and funding fees can help you plan better and avoid surprises.

Also, when lenders look at your financial profile, they don’t just zero in on your credit score. They consider your whole financial picture, including your debt-to-income ratio and credit history. This can be a real advantage if traditional financing has been a challenge.

Support and Resources for Kentucky Veterans

State Benefits for Veterans and Active Duty

Kentucky offers a wide range of benefits for veterans and active-duty service members. From financial assistance to housing benefits, the state ensures that those who have served are well-supported. Veterans can access benefits counseling to understand what they’re eligible for and how to apply. Additionally, Kentucky provides tax exemptions for disabled veterans, helping ease the financial burden.

Housing Assistance Programs

Finding a home can be challenging, but Kentucky has several programs to assist veterans in securing housing. The state offers skilled long-term care at veterans centers, ensuring that those who need it have access to quality care. Furthermore, veterans can benefit from programs that help with home loans and property tax exemptions, making homeownership more accessible.

Educational and Employment Resources

Education and employment are crucial for veterans transitioning to civilian life. Kentucky offers educational benefits, including tuition assistance and scholarships for veterans and their families. Employment resources are also available, providing job training and placement services to help veterans find meaningful work. These resources aim to support veterans in building a stable and fulfilling post-military career.

Kentucky is committed to honoring its veterans by providing comprehensive support and resources. Whether it’s through housing assistance, educational opportunities, or employment services, the state strives to ensure that veterans can thrive in their communities.

So, there you have it. If you’re a veteran or active-duty service member in Kentucky, a VA loan could be your ticket to homeownership. With no down payment and flexible credit requirements, it’s a pretty sweet deal. Just make sure you have your paperwork in order, like your Certificate of Eligibility and proof of income. Remember, the process might seem a bit daunting at first. However, many resources and lenders are ready to help you. Homeownership is a big step, but with the right support, it’s totally doable. Good luck on your journey to finding that perfect Kentucky home!

Yes, Kentucky offers many benefits for veterans, including housing assistance, financial aid programs, and educational opportunities.

Do veterans have to pay a funding fee in Kentucky?

Most veterans need to pay a VA funding fee, but there are exceptions. It’s best to check with your loan officer for specific details.

Does Kentucky offer VA loans to surviving spouses?

Yes, surviving spouses who meet certain qualifications can apply for VA loans in Kentucky.

Is it hard to get approved for a VA loan in Kentucky?

VA loans are designed to be accessible for eligible veterans and their families. They often have more flexible credit requirements and no down payment, making approval easier than some other loans.

1 – 📅 Email – kentuckyloan@gmail.com

📞 Call/Text – 502-905-3708

Joel Lobb Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

NMLS 57916 | The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

VA loans in Kentucky, Kentucky VA mortgage, and VA home loans for veterans in Kentucky.

Kentucky VA Mortgage Loan Guide for Home Buyers

You’ve come to the right place if you’re a Kentucky veteran or an active military member. You are searching for VA loan information in Kentucky. VA loans offer unique benefits and flexibility, but many myths and misconceptions surround them. Let’s debunk these myths now. We will give precise information to help you make informed decisions when applying for a Kentucky VA mortgage loan.

Common Myths About Kentucky VA Loans

Myth #1: VA Loans Are Hard to Qualify For

Fact: VA loans have more flexible credit and income requirements than conventional loans. They allow higher debt-to-income (DTI) ratios and lenient credit score thresholds.

No Minimum Credit Score: The VA does not set a minimum score, but most lenders require 620. Some go as low as 580, though approvals for lower scores can be more challenging.

Myth #2: VA Loans Need a Down Payment

Fact: VA loans do not require a down payment for loans at or below the local conforming limit.

Jumbo Loans: For higher loan amounts, down payment requirements depend on your VA entitlement:

Fact: You can havemultiple VA loans as long as you have remaining entitlement.

Entitlement Coverage:

Loans under $144,000: VA guarantees up to $36,000.

Loans over $144,000: VA guarantees up to 25% of the loan amount.

Note: If you’ve used a part of your entitlement for another loan, you may need to make a down payment. This applies to extra loans.

Myth #6: You Can Only Use a VA Loan Once

Fact: You can use your VA loan benefits unlimited times throughout your life.

To reuse the benefit, you must either:

Pay off your current VA loan, or if enough entitlement is left on your COE, and you qualify with both house payments on the dti and residual income test, you may be able to have two va loans active at the same time

Use a conventional loan to buy land, then refinance into a VA loan after building your home.

Myth #9: You Can’t Build a House with a VA Loan

Fact: VA construction loans allow you to build a home, as long as the builder is VA-approved. Upon completion, you can refinance the loan into a permanent VA mortgage.

Myth #10: VA Loans Are Only for Home Purchases

Fact: VA loans can also be used for home improvement projects.

TheVA Energy Efficiency Mortgage Programallows you to add up to $6,000 for energy-efficient upgrades. These include solar heating, insulation, and storm windows.

Benefits of Kentucky VA Loans

100% Financing: No down payment required.

No PMI: Reduces your monthly mortgage payment.

Low Closing Costs: Sellers can pay closing costs and prepaid, up to 4% and even payoff borrower’s debts to qualify for a mortgage loan above the 4% threshold for seller concessions

Flexible Credit Guidelines: Perfect for veterans with past credit issues. No minimum credit score but wight most heavily the last two years on credit report. No foreclosure, Chapter 7 bankruptcies the last two years

Assumability: Allows buyers to take over existing VA loans.

Get Started with Your Kentucky VA Loan Today!

As a mortgage loan officer, I have over 20 years of experience. I’ve helped more than 1,300 Kentucky families buy or refinance their homes. Whether you’re buying your first home, upgrading, or refinancing, I’m here to make the process smooth and stress-free.

You must be logged in to post a comment.