I have successfully originated over 200 VA Home loans in Kentucky. Put my experience to work for you. Call or text me today at 502-905-3708 or email me at Kentuckyloan@gmail.com-This website is not affiliated with the VA or any other government agency. NMLS #57916 Equal Housing Lender. Same Day Approvals, Fast Closings, and a Local Veteran offering VA Home Loans in Kentucky. Free Credit Report and Pre-Approvals NMLS# 57916 Joel Lobb Loan Originator, Company NMLS ID 1738461 . Equal Housing Lender

Here are 10 facts about Kentucky Mortgage VA Loans you might not have known.

Kentucky Mortgage VA Loans do not have a maximum loan limit. The Veteran can qualify for up to $2-3 million they may need to put down payment in depending on the entitlement they have.

VA manual underwriting is 0 x 30 in the last 12 month on revolving and installment credit. We can ignore credit over 12 months old.

Kentucky Mortgage VA Loans DTI is up to whatever DU/LP will approve. On manual underwriting will do up to 50% with 120% residual income.

Kentucky Mortgage VA Loans does not have an identity of interest guideline. VA allows non-arm’s length transactions.

Kentucky Mortgage VA Loans does not have a flipping rule. If the value can be supported with an appraisal and there is no indication of inappropriate behavior ok to proceed.

Seller can pay more than 4% concession/closing costs.

Kentucky Veterans with entitlement that has been previously used can use their additional 25% to obtain 100% financing.

VA disability can be grossed up 125% Kentucky Mortgage VA Loans

VA allows no score with alt trades.

Kentucky VA Mortgage Loans require 2 years out of bankruptcy for Chapter 7 and 1 year for Chapter 13 bankruptcy

How Soon Can You Qualify for a VA Loan after a Chapter 7 or Chapter 13 Bankruptcy in Kentucky?

Kentucky VA mortgage guide for bankruptcy

As a reminder, these are the basic differences between bankruptcies which impact VA qualifying differently:

Chapter 7 Bankruptcy: you ask the bankruptcy court to discharge most of the debt you owe

Chapter 13 Bankruptcy: you file a repayment plan with the bankruptcy court to pay back all or a portion of your debts over time.

So, does the type of bankruptcy filed affect VA loan qualifying? The answer is YES, it most definitely does.

How soon can you qualify for a VA loan after a Chapter 7 Bankruptcy?

Chapter 7 Bankruptcies discharged more than two years ago from the date of closing for purchases and refinance, it may be disregarded.

If the bankruptcy was discharged within the last 1 to 2 years, it is probably not possible to determine that the applicant or spouse is a satisfactory credit risk unless both of the following requirements are met:

The applicant or spouse has obtained consumer items on credit subsequent to the bankruptcy and has satisfactorily made the payments over a continued period; and

The bankruptcy was caused by circumstances beyond the control of the applicant or spouse such as unemployment, prolonged strikes, medical bills not covered by insurance, and so on, and the circumstances are verified. Divorce is not generally viewed as beyond the control of the borrower and/or spouse.

Please note that additional factors can contribute towards granting an exception to the 2 year policy, but any and all factors considered would have to be reviewed on a case by case scenario prior to approval. Borrowers discharged for less than a year will not generally be accepted as a satisfactory credit risk.

How soon can you qualify for a VA loan after a Chapter 13 Bankruptcy?

A. For Chapter 13 Bankruptcies that are still in progress:

The applicant must document at least one year into the payout plan has elapsed along with satisfactory payment history

The applicant must obtain court permission to enter into the new mortgage

When the bankruptcy is still in repayment, the Chapter 13 payment will be counted in the debt ratios

B. Once the borrower has satisfactorily completed the repayment, the borrower is considered to have re-established credit

As you can see, the type of bankruptcy can drastically impact VA loan eligibility and the required waiting period.

If you have filed for chapter 7 or chapter 13 bankruptcy, then you can still qualify for a mortgage just one day out of bankruptcy. Today, there are thousands of people who are trying to find a mortgage after filing for bankruptcy. In the past, finding a mortgage after a bankruptcy was not the easiest thing to do. The good news is that today you can get a mortgage just one day out of bankruptcy.

How Long after a Bankruptcy Can I Qualify for a Mortgage?

There are bankruptcy lenders who can help with your mortgage even just one day out of chapter 7 or chapter 13 bankruptcy. You will likely need a larger down payment and show that you are taking steps to improve your credit.

Below, we will take you through some mortgage after bankruptcy options and then connect you with some of the best bankruptcy lenders. We understand that you area dealing with a lot and having a bankruptcy is not easy. Let us help guide you through this process.

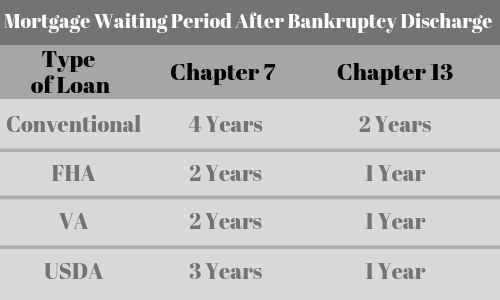

Type of Loan

Chapter 7

Chapter 13

Conventional

4 years

2 years

FHA

2 years

1 year

VA

2 years

1 year

USDA

3 years

1 year

Subprime

1 day

1 day

How Long Must You Wait To Qualify for a Mortgage After Filing for Bankruptcy

Every type of loan has different waiting period requirements. Here are some of the basics:

No down payment in most cases for purchase loans (up-front money toward your home purchase), and easier borrower credit requirements.

No monthly mortgage insurance premiums or private mortgage insurance (PMI).

Lower homebuyer closing costs, and limits to what borrowers can be charged.

The opportunity to roll your “VA funding fee” into your mortgage.

The ability to refinance a non-VA loan into the VA mortgage program.

The opportunity to: ask a home seller to contribute up to 4 percent of the mortgage amount to cover some of the closing costs; ask your lender to cover some of the closing costs; seek closing cost assistance through state homebuying programs created for veterans and first-time buyers.

The right to become a VA borrower for life. In most cases you can use VA mortgage programs forever, and sometimes you can have more than one VA loan.

Eligibility of financing for spouses of service-members who died in the line of duty or from a service-related disability.

You can review all types of Kentucky VA Home Loans here, including purchase mortgages, refinance mortgages (called Interest Rate Reduction Refinance Loans or IRRRLs), and cash-out refinance loans.

To qualify for a Kentucky VA Home Loan, usually a military veteran or service-member must have 90 consecutive days of active service during wartime, or 181 straight days of service during peacetime, or six years in the national guard or reserves of a particular military branch. You can find out if you’re eligible here.

Kentucky VA mortgage comes with an additional closing cost called a “VA funding fee” of between 1.4 to 3.6 percent on the amount borrowed (depending on your circumstance). This special fee that non-VA borrowers never have to pay helps partially fund the “government backed” part of the VA borrower program, and many VA borrowers can roll it into their mortgage.

VA Loan Quick Facts

0% Down

Minimum Down Payment

620 Credit

Minimum Credit Score

41% DTI

Max Debt-to-Income Ratio

What is a VA Loan?

VA Loans are designed to assist veterans purchase a home. Active duty military and veterans across the nation will enjoy the desirable loan terms and low interest rates that often come with a VA loan. Additional benefits like no down payment requirement help make home buying an affordable and cost-effective reality for those who have served and continue to serve our country.

What are the benefits of a VA Loan?

VA Loan benefits and features:

Zero down payment

Buyers may finance the funding fee into the loan

Closing costs may be covered

Buyers may use gifts and seller contributions to cover closing costs

Who may benefit from a VA Loan?

A VA Loan may the right fit for you if:

You’re an eligible veteran or active-duty military

You’re buying a first home or are a repeat homebuyer

You must be logged in to post a comment.