How to Get a VA Home Loan With Bad Credit in Kentucky (2026)

Kentucky veterans with credit challenges still have a strong path to homeownership through VA loans. Even if you have experienced financial setbacks such as bankruptcy, foreclosure, collections, late payments, or a lower credit score, the VA mortgage program is designed to help you recover. This 2026 guide explains how Kentucky veterans can qualify for a VA home loan despite past credit issues.

Why VA Loans Work for Kentucky Veterans With Credit Issues

VA loans remain one of the most forgiving and flexible mortgage programs available to Kentucky veterans and active-duty service members. Because the loans are backed by the U.S. Department of Veterans Affairs, lenders can approve files that would not qualify under many conventional or even FHA rules.

Key advantages for credit-challenged Kentucky buyers include:

- Zero down payment required in most cases

- No monthly mortgage insurance (PMI)

- No official minimum credit score set by the VA

- Competitive interest rates even for borrowers below 620

- Flexible underwriting that looks at the whole financial picture, not just a score

For many veterans who are rebuilding after financial setbacks, VA loans create opportunities that other loan programs simply cannot match.

Credit Score Requirements for Kentucky VA Loans in 2026

The VA does not publish a minimum credit score requirement. Instead, individual lenders set their own guidelines, often called overlays. In the current Kentucky market, those overlays generally look like this:

- 580–599: Possible with manual underwriting and a strong recent history

- 600–619: Strong candidate for manual underwriting

- 620–639: Often eligible for automated underwriting approval

- 640 and higher: Easier approvals and stronger interest rate options

Some lenders may review scores in the low 500 range with strong compensating factors, but most successful approvals occur when the borrower is at least in the high 500s with improving credit and clean recent payment history.

What Counts as “Bad Credit” on a VA Loan?

Lenders look at both your credit score and your recent credit behavior. Typical categories are:

- 500–579: Poor

- 580–619: Fair

- 620 and higher: Preferred for automated approvals

The score alone does not tell the whole story. Recent activity frequently matters more. A borrower with a 615 score and a clean 12-month history can look stronger to an underwriter than a 660 score with recent late payments.

Automated vs. Manual Underwriting for Kentucky VA Loans

Automated Underwriting (AUS)

Automated underwriting systems (AUS) such as DU or LPA evaluate your file electronically. This is the preferred path when scores are 620 or higher. When AUS returns an Approve/Eligible finding:

- Approvals are typically faster

- Documentation can be somewhat lighter

- Rate pricing is often stronger

Manual Underwriting

Manual underwriting is used when AUS does not approve the file or when the lender chooses to underwrite the file by hand. This is often the path for Kentucky veterans with scores below 620.

Manual underwriting focuses on:

- Clean (or significantly improved) payment history in the last 12 months

- Stable income and employment

- Meeting or exceeding VA residual income guidelines

- Acceptable debt-to-income (DTI) ratios

- Reasonable explanations and documentation for past credit problems

Manual underwriting is not a second-class approval. When structured correctly, it is a powerful way for credit-challenged veterans to obtain a home loan.

Waiting Periods After Bankruptcy or Foreclosure in Kentucky

Major credit events do not permanently prevent you from using your VA home loan benefit. Typical VA waiting periods are:

- Chapter 7 bankruptcy: 2 years from discharge, sometimes 1 year with strong extenuating circumstances

- Chapter 13 bankruptcy: At least 12 months of on-time plan payments with court or trustee approval; fully eligible after discharge

- Foreclosure or short sale: 2 years from the date title transferred out of your name; possibly 1 year with documented extenuating circumstances

If a previous VA loan resulted in a foreclosure or loss, you may also need to address any remaining VA entitlement issues before using full benefits again.

How Collections and Other Credit Issues Are Viewed

Not all negative items carry the same weight in underwriting. In many Kentucky VA approvals:

- Medical collections are often not a major issue

- Older credit card collections may be acceptable if they are seasoned and no longer growing

- Recent mortgage or rent late payments within the last 12 months are usually serious red flags

- Child support, IRS, and student loan delinquencies typically must be resolved or in a documented repayment plan before closing

Underwriters pay close attention to whether negative credit is in the past and has been addressed, or whether it is still ongoing.

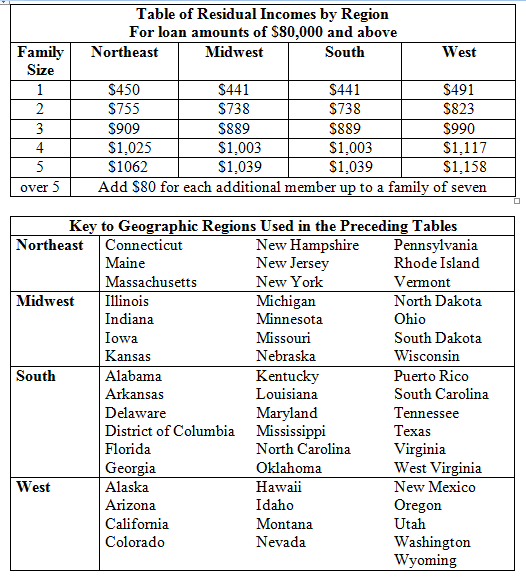

Residual Income and Compensating Factors

VA loans use residual income as a key measure of affordability. Residual income is the money left over after all major obligations, including the new mortgage payment and recurring debts, are paid each month.

Kentucky falls in the South region on VA residual income charts. For many manually underwritten files, lenders prefer residual income that is at least 20 percent above the minimum table requirement. This can offset a lower score or higher DTI.

Additional compensating factors that strengthen a credit-challenged file include:

- Significant liquid reserves or savings

- Long-term employment history in the same field

- Only a small payment increase compared with current rent

- VA disability or retirement income that is stable and likely to continue

- Documented 12-month history of on-time rent or housing payments

Steps to Improve Your VA Approval Odds in 30–60 Days

You do not have to spend years rebuilding credit before looking at a VA loan. Many Kentucky veterans see improvement within a few months by focusing on the right steps:

- Pay down credit cards so balances are below 30 percent of limits

- Check all three credit bureaus for errors and dispute any inaccuracies

- Avoid opening new loans or credit cards during the loan process

- Eliminate overdrafts and non-sufficient funds activity

- Make every payment on time for at least 12 months before applying

- Gather documentation for any medical or job-related hardships that contributed to past problems

These actions can move a file from borderline to approvable without dramatically changing the score itself.

VA Loans With Little or No Traditional Credit History

Some Kentucky veterans have little or no traditional credit. In these cases, VA guidelines allow the use of non-traditional or alternative credit.

Acceptable alternative credit lines can include:

- Rent payments with a 12-month on-time history

- Utility bills such as electric, gas, or water

- Auto insurance payments

- Cell phone or internet bills

Most lenders will look for at least three alternative trade lines with a 12-month history to build a sufficient picture of credit behavior.

Common Myths About VA Loans and Bad Credit

Several myths keep veterans from exploring a VA loan when they should.

-

Myth: No minimum score means everyone is approved.

Reality: Lenders still apply their own standards to protect borrowers and ensure loans are affordable.

-

Myth: Being current now means recent late payments no longer matter.

Reality: Underwriters pay close attention to the most recent 12 to 24 months.

-

Myth: All negative credit items are treated the same.

Reality: A medical collection is not viewed the same way as a recent mortgage late.

Related Kentucky Mortgage Guides

Talk Through Your Situation With a Kentucky VA Loan Specialist

Bad credit does not automatically mean you cannot buy a home in Kentucky. With VA’s flexible guidelines, manual underwriting, and a structured plan to strengthen your file, many veterans qualify much sooner than they expect.

Joel Lobb – Kentucky VA Mortgage Specialist

NMLS 57916 | Company NMLS 1738461

Call or text: 502-905-3708

Email: kentuckyloan@gmail.com

Website: www.kentuckymortgageblog.com

Online application: Apply Now for VA Pre-Approval

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval, property approval, and underwriting guidelines. Programs, terms, and guidelines are subject to change without notice.

Why Work With Me? Local Expertise: I know the ins and outs of Kentucky’s housing market and loan programs. Fast Approvals: I offer free mortgage applications with same-day approvals to keep the process moving quickly. Customized Loan Solutions: Whether you’re buying a home or refinancing, I’ll find the right loan program to fit your needs. Personalized Service: I treat every client like family, ensuring you’re supported and informed throughout the process. About My Website Visit my website for a wealth of resources tailored to Kentucky homebuyers. You’ll find: Step-by-step guides for first-time homebuyers. Information on loan programs like FHA, VA, USDA, and KHC. Tools to help you calculate potential payments and affordability. Blog posts with tips and updates on the Kentucky housing market. A secure portal to start your loan application and upload documents. Please Note: My website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist homebuyers with expert advice and accessible tools.

You must be logged in to post a comment.