VA Guidelines for Covid-19

Income Verification

Lenders may continue to use good judgement and flexibility when verifying a borrower’s income and determining whether that income is stable and reliable and will follow standard VA guidelines.

Third-party services may be used to provide employment and income verification (please note additional fees associated with these services cannot be charged to borrower).

Note: The VOE flexibilities previously announced by VA have not been extended and did expire 04/01/2021.

Income Analysis

VA’s guidelines generally require income to be stable and reliable for 2 years. However, borrowers’ income impacted by COVID-19 may continue to be reviewed as follows:

Any period in a borrower’s income (i.e. furlough, curtailment of income, etc.), should not be considered a break in employment or income provided they have returned or anticipated to return to work in the same capacity and income levels. In addition to standard verification documentation Borrower’s should provide furlough letters where applicable.

VA continues to encourage proactive measures in documenting and obtaining evidence of their analysis and justifications for all Borrower’s, especially borderline cases.

This may proactively address questions that VA may otherwise ask and prevent a loan level audit of a loan.

Remote Online Notarization (RON)

Additionally, ensure that the VA-guaranteed home loan is secured by a first lien on the property being used as collateral.

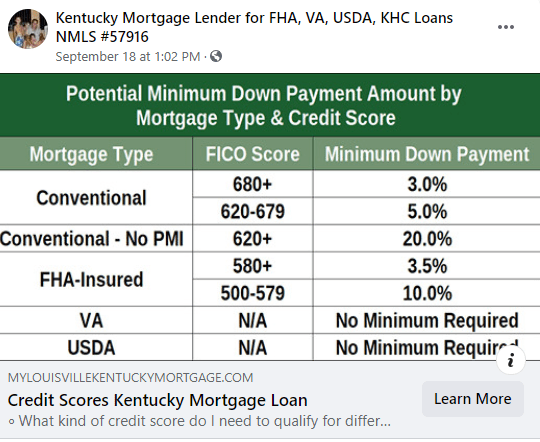

What is the minimum credit score I need to qualify for a Kentucky FHA, VA, USDA and KHC Conventional mortgage loan

What is the minimum credit score I need to qualify for a Kentucky FHA, VA, USDA and KHC Conventional mortgage loan

You must be logged in to post a comment.