I have successfully originated over 200 VA Home loans in Kentucky. Put my experience to work for you. Call or text me today at 502-905-3708 or email me at Kentuckyloan@gmail.com-This website is not affiliated with the VA or any other government agency. NMLS #57916 Equal Housing Lender. Same Day Approvals, Fast Closings, and a Local Veteran offering VA Home Loans in Kentucky. Free Credit Report and Pre-Approvals NMLS# 57916 Joel Lobb Loan Originator, Company NMLS ID 1738461 . Equal Housing Lender

How to Calculate Residual Income for a Kentucky VA Home Loan Approval (2026)

Kentucky veterans using a VA home loan must meet minimum residual-income requirements. Residual income measures the monthly funds left over after housing costs, taxes, and all recurring bills. It is a core underwriting factor that determines whether a VA loan can be approved, especially when debt-to-income ratios are higher or credit depth is limited.

This guide breaks down how residual income works, how to calculate it correctly, and the 2026 minimums required for Kentucky VA buyers.

Residual income is the amount of money left after subtracting all monthly obligations from the borrower’s gross monthly income. The VA establishes region-based minimums to ensure borrowers have enough remaining funds to cover essentials such as food, transportation, clothing, utilities, and other living expenses.

Even if a borrower has a high credit score and a strong DTI ratio, the loan cannot be approved without meeting minimum residual-income thresholds.

How Kentucky Lenders Calculate VA Residual Income

Start with gross monthly income for all occupying borrowers.

Subtract federal, state, and local taxes based on paystubs/W-2 withholding tables.

Subtract the proposed housing payment (PITI): principal, interest, taxes, insurance, HOA, and any maintenance fees.

Subtract all recurring debts:

auto loans

student loans

credit card minimums

child support / alimony

personal loans or installment debt

Subtract estimated utilities/maintenance. Many lenders use approximately $0.14 per square foot of heated living space.

The figure remaining after all these deductions is the official VA residual income.

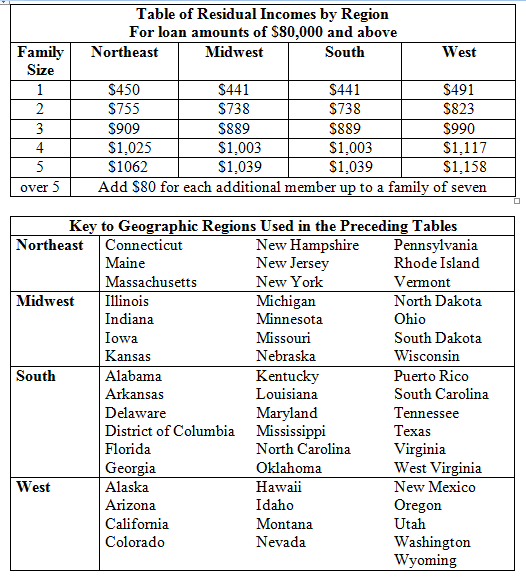

2026 VA Residual Income Requirements for Kentucky (South/Midwest Region)

Household Size

Minimum Residual Income

1 Person

$441

2 Persons

$738

3 Persons

$889

4 Persons

$1,003

5 Persons

$1,039

Each Additional Person

Add $80

If debt-to-income ratio exceeds 41 percent, underwriters typically require 20 percent more than the baseline residual number.

Why Residual Income Matters More Than DTI

Residual income is one of the strongest predictors of loan performance in the VA program. Borrowers who meet or exceed the residual-income benchmark show significantly higher repayment success rates — even when credit scores are less than perfect or DTI ratios appear high.

If the loan does not meet residual income, the file cannot be approved without compensating factors or structural changes to qualifying income or household composition.

Free Help Calculating Residual Income

If you want, I can run a complete residual-income analysis for you or your buyer using up-to-date 2026 VA guidelines.

KHC Eligibility and Credit Standards Overview offers crucial guidelines. These guidelines are for Kentucky home buyers seeking assistance through Kentucky Housing Corporation KHC Loan Programs(KHC) loan programs

The KHC Eligibility and Credit Standards Overview offers crucial guidelines. These guidelines are for Kentucky home buyers seeking assistance through Kentucky Housing Corporation KHC Loan Programs(KHC) loan programs. Here’s a summary of key points from the image:

Kentucky khc Home Buyer Eligibility

Available for first-time and repeat home buyers across Kentucky.

Borrower must be a U.S. citizen or legal resident.

Income eligibility is determined through the Secondary Market.

The property must be the borrower’s primary residence.

Borrowers cannot own any other residential property at the time of closing if using MRB Funding.

Down Payment Assistance is available for borrowers who meet both income and purchase price limits.

Non-taxable income can be grossed up, which helps borrowers qualify for higher loan amounts.

Property Eligibility for khc loan programs

Eligible properties include both new and existing homes.

Manufactured homes are eligible for both new and existing purchases.

RHS loans only allow new construction for manufactured housing.

Purchase price limit: HERE ➡️➡️for Secondary Market and MRB Loans.

Full appraisals are required for all KHC loans.

VA loans require a termite inspection for existing properties.

New construction properties (except conventional loans) must have a termite soil treatment certificate.

KHC credit and income qualifying guidelines

Flexible credit requirements: Borrowers with 620+ credit scores can qualify for FHA, VA, and RHS loans. On the other hand, Conventional loans require a 660+ credit score.

Debt-to-income ratio of up to 50% allows flexibility for borrowers with higher debt obligations.

Down Payment Assistance is available for those who meet income and price limits.

Manufactured housing is eligible, but new construction requirements apply for RHS loans.

Bankruptcy and foreclosure waiting periods range from 2-7 years, depending on the loan type.

Eligible KHC Mortgages

FHA, RHS, VA, HFA Preferred, HFA Preferred Plus 80, & Freddie HFA Advantage

Must be used with a KHC first mortgage

khc Eligibility Requirements

Summary of khc mortgage loan product

DAP funds are only available to home buyers obtaining a KHC first mortgage.

Offers affordable repayment terms (4.75% interest over 15 years).

No home buyer education required, which simplifies the process.

Can be used with various loan programs (FHA, VA, USDA, Conventional).

Debt-to-income ratios up to 50% are allowed with AUS approval.

This program makes homeownership more accessible by providing down payment assistance without requiring extensive upfront savings. Would you like help determining eligibility or applying for KHC mortgage assistance? Let me know!

To qualify for aVA loan in Kentucky, there are several key requirements and guidelines to consider, based on the information provided:

Credit Score : While the VA itself does not set a minimum credit score requirement, most lenders in Kentucky typically require a credit score of at least 580–620 for approval. Some lenders may accept scores as low as 580 , but a higher score improves your chances of approval

Bankruptcy

Bankruptcy must be discharged 2 years from Chapter 7 and 1 year for a Chapter 13 or if you have been in Chapter 13 for minimum of 12 months with no late pays and bankruptcy trustee allows, you can buy a home using your VA certificate of Eligibility

Inspections

VA loans require termite inspections but no home inspections

Work history and debt to income requirements

VA does not have a minimum income or maximum income on their loan programs

Work history needed for last 2 years. If you are out of military less than 12 months from new mortgage date, you must have a job lined up that typically matches your MOS in order to qualify. No part time or temp to hire jobs unless you have been out of Military for 2 years and working at them for the last two years. No set job time after you get of of military or job gaps as long as you can show stability in your income and previous work history

VA disability can be used for income qualifying purposes and can usually be grossed up 125% since non taxable, but for residual net income qualifying purposes you can gross up.

You can have more than one VA loan and in fact, if you have enough VA entitlement left on your COE, you can have two VA loans open at the same time. I have done many like this in my career

All VA lenders are not the same. Check around for second opinions.

VA lenders all have different sets of rates and will set there on rates and closing costs-Check around. You will be surprised .

VA loans with co-borrower that is not your spouse

If you are getting a VA loan and the co-borrower is not married to you, then you have to put down at least 12% down payment. One of those weird VA rules when it comes to non-borrowing spouse.

VA loan residency requirements

VA loans are only for primary residences and not to be used for rental homes.

You can turn a home that has a VA Mortgage into a rental after 12 months or if you get shipped to a different duty station

Typically takes about 30 days to close a VA loan with the home appraisal taking about 10 days from start to finish. It is the most lengthy part of the loan processing and closing process after you get a house under contract.

Debt-to-Income Ratio (DTI) : Although the VA does not impose a strict DTI cap, lenders generally prefer borrowers to have a debt-to-income ratio of less than 41% to qualify for a VA loan. However, some flexibility may exist depending on other financial factors.

Down Payment: One of the major benefits of a VA loan is that it requires no down payment in most cases, making homeownership more accessible for eligible borrowers

Proof of Income and Employment : Borrowers must demonstrate stable income and provide proof of employment. Lenders typically prefer at least two years of steady employment history

Certificate of Eligibility (COE) : To apply for a VA loan, you must obtain a Certificate of Eligibility (COE) , which verifies your eligibility based on your military service. Veterans will need to provide a DD Form 214 , while active-duty members and National Guard/Reserve members may need different documentation

VA Funding Fee : A VA funding fee is required at closing unless the borrower qualifies for an exemption (e.g., due to a service-connected disability). The fee amount varies depending on factors such as the type of veteran, down payment amount, and whether it’s the borrower’s first time using the VA loan benefit

Property Requirements : The property being purchased must meet the VA’s minimum property requirements (MPRs) to ensure it is safe, structurally sound, and habitable. Additionally, VA loans are only available for primary residences

Loan Limits : While the VA does not impose maximum loan limits, lenders who sell their loans in the secondary market may cap loan amounts. As of January 1, 2025 , the VA loan limit for all counties in Kentucky is $806,500

No Private Mortgage Insurance (PMI) : Unlike conventional loans, VA loans do not require private mortgage insurance (PMI) , even with no down payment, which can save borrowers significant money over time

By meeting these requirements, eligible veterans, active-duty service members, and surviving spouses can take advantage of the many benefits offered by VA loans in Kentucky

What are the steps to apply for a VA loan in Kentucky?

To apply for a VA loan in Kentucky, you can follow these steps based on the information provided:

1. Determine Your Eligibility

The first step is to confirm that you are eligible for a VA loan. Eligibility is typically extended to veterans, active-duty service members, National Guard/Reserve members, and certain surviving spouses 1. You will need to obtain a Certificate of Eligibility (COE) , which verifies your eligibility based on your military service. Veterans typically need to provide a copy of their DD Form 214 (discharge or separation papers), while active-duty members may need different documentation 8.

2. Apply for Your Certificate of Eligibility (COE)

VA loans are issued by private lenders (banks, credit unions, or mortgage companies) but are guaranteed by the Department of Veterans Affairs. It’s important to select a lender that specializes in VA loans, as they will be familiar with the process and requirements

Additionally, lenders generally look for a DTI ratio of less than 41% , though some flexibility may exist depending on other factors if you have a higher residual income, a large down payment, or a lot of reserves or a higher credit score of say over 740

5. Property Appraisal and Underwriting

The lender will order aVA appraisalto ensure the property meets the VA’s minimum property requirements (MPRs). These requirements ensure the home is safe, structurally sound, and habitable . You may also choose to have a separate home inspection to identify any potential issues with the property

6. Pay the VA Funding Fee (If Applicable)

Most borrowers are required to pay a VA funding feeat closing, unless they qualify for an exemption (e.g., due to a service-connected disability). The fee amount varies depending on factors such as the type of veteran, down payment amount, and whether it’s the borrower’s first time using the VA loan benefit

7. Close on the Loan

Once the appraisal and underwriting processes are complete, you’ll move to the closing stage. At closing, you’ll sign all necessary documents to finalize the loan. Since VA loans do not require a down payment, you won’t need to bring funds for that purpose, but you will need to cover closing costs, which may include the funding fee (if applicable) –Seller can pay up to 4% of the sales price toward buyers closing costs and prepaids and even payoff VA borrower’s debt to qualify. This is the only type of loan that offers seller concessions whereas the seller can pay off buyer’s debts to qualify on debt to income ratio purposes or residual income requirements

Evo Mortgage Company NMLS# 1738461 Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans and Down Payment Assistance Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

VA Mortgage Loan Guide for Kentucky (2025–2026)

Kentucky veterans and active-duty service members continue to use the VA home loan program as one of the most powerful financing tools available. This guide is designed to reflect current VA policy, practical lender requirements, and Kentucky market realities, so you are working with accurate information instead of outdated rules or generic national advice.

What Is a VA Mortgage Loan?

A VA mortgage is a home loan backed by the U.S. Department of Veterans Affairs. The VA does not lend money directly. Instead, private lenders fund the loan and the VA guarantees a portion of it. That guarantee allows qualified Kentucky veterans and service members to access more flexible guidelines and better terms than most other loan programs can offer.

Key Benefits of a Kentucky VA Mortgage

Zero down payment required for most eligible buyers

No monthly private mortgage insurance (PMI)

More flexible credit standards than many conventional loans

Competitive fixed interest rates

Higher allowable debt-to-income ratios when residual income is strong

Streamlined refinance options, including IRRRL (Interest Rate Reduction Refinance Loan)

Assumable loans, subject to lender approval and buyer qualification

Basic VA Eligibility for Kentucky Borrowers

You may qualify for a VA home loan if you meet one of these service requirements:

At least 90 days of active-duty service during wartime, or

At least 181 days of active-duty service during peacetime, or

At least 6 years in the National Guard or Reserves, or

You are an eligible surviving spouse of a veteran who died in service or from a service-connected cause

A Certificate of Eligibility (COE) confirms your entitlement. Most lenders can obtain your COE electronically in a few minutes.

Credit Score Requirements (What Actually Matters)

The VA itself does not publish a minimum credit score requirement. Instead, lenders use their own credit overlays. In Kentucky, many lenders look for a minimum score in the 580 to 620 range, with the best pricing typically starting around 620 and above.

The real focus is on your overall credit profile and recent payment history, not just a single score. A strong record of on-time payments, limited recent derogatory items, and responsible use of credit can offset a lower score in some cases.

Bankruptcy, Foreclosure, and Derogatory Credit

Chapter 7 bankruptcy: Generally at least 2 years from discharge

Chapter 13 bankruptcy: At least 12 months of on-time plan payments, with trustee approval

Foreclosure or short sale: Typically a 2-year waiting period

Late payments: Isolated older lates can be acceptable, but recent serious delinquencies may require additional documentation or a manual underwrite

Income, Debt-to-Income, and Residual Income

Many borrowers focus only on debt-to-income ratio (DTI), but VA underwriting heavily emphasizes residual income. Both work together.

Debt-to-Income Ratio (DTI)

There is no hard maximum DTI in the VA program. A 41 percent DTI ratio is a common benchmark, but approvals above that level are allowed when the file is otherwise strong, especially if residual income and credit history are solid.

Residual Income

Residual income is the amount of money left over each month after paying your major obligations, including the new housing payment, taxes, insurance, and recurring debts. VA uses regional residual income tables based on household size. Kentucky is in the South Region.

Strong residual income can help offset higher DTI ratios, limited cash reserves, or a lower credit score, and it is one of the main reasons VA loans have historically low default rates.

Property Requirements for Kentucky VA Loans

Occupancy Rules

The property must be used as your primary residence

Occupancy is generally required within about 60 days after closing

A spouse can often satisfy the occupancy requirement if you are deployed or temporarily away

Eligible Property Types

Single-family homes

VA-approved condominiums

Townhomes

Two- to four-unit properties when you live in one of the units

Some manufactured homes, if they meet VA and lender guidelines

Pure investment properties, short-term vacation rentals, or homes that you do not plan to occupy as a primary residence are not eligible.

VA Minimum Property Requirements (MPRs)

VA MPRs focus on safety, soundness, and sanitation. Examples include:

No major structural issues or unsafe conditions

Roof and mechanical systems in acceptable condition

Functioning heating, electrical, and plumbing systems

No active termites or severe wood-destroying insect damage

Safe access to the property and acceptable water and waste disposal

Peeling lead-based paint corrected on older homes

Loan Amounts, Down Payment, and Funding Fee

Loan Limits and Entitlement

If you have full VA entitlement, there is no formal VA loan limit. In that situation, the amount you can borrow in Kentucky is mainly driven by your income, debts, and the property value, not a published county loan limit.

If you have partial entitlement because of an existing VA loan or a prior loss, then the standard Federal Housing Finance Agency (FHFA) conforming loan limits apply. For most Kentucky counties, that limit is currently around the mid-800 thousand range for one-unit properties, and lenders will calculate your maximum loan based on remaining entitlement and the purchase price.

Down Payment

Most Kentucky VA buyers purchase with zero down payment. A down payment may be required if you have reduced entitlement, are purchasing above certain price points with partial entitlement, or choose to put money down to lower the payment or funding fee.

VA Funding Fee

The VA funding fee helps keep the program self-sustaining. It is a one-time cost paid at closing or financed into the loan. The amount depends on your service history, down payment, and whether this is your first or subsequent use of VA eligibility.

Common examples include:

First-time use with zero down: typically a little over two percent of the loan amount

Subsequent use with zero down: typically a little over three percent of the loan amount

Many veterans do not pay the funding fee at all. If you receive qualifying VA disability compensation, hold certain Purple Heart or surviving spouse statuses, you may be exempt.

Kentucky VA Loan Process

Initial conversation and prequalification – Review your goals, income, credit, and service history.

COE request – The lender pulls your Certificate of Eligibility from the VA portal.

Full application and documentation – Collect pay stubs, W-2s, LES statements, tax returns, bank statements, and award letters as needed.

Automated underwriting – The file runs through an automated underwriting system to generate an Approve/Eligible or Refer finding.

Appraisal and property review – A VA appraiser confirms value and checks Minimum Property Requirements.

Underwriting review – The underwriter verifies income, assets, employment, credit, and residual income.

Clear to close – Final conditions are met and closing documents are prepared.

Closing and move-in – You sign your closing package, the loan funds, and you receive the keys.

Common VA Loan Myths in Kentucky

Myth: You need perfect credit to qualify. Reality: VA guidelines are often more flexible than conventional or even FHA in many areas.

Myth: VA loans always take longer. Reality: With a complete file and responsive parties, VA loans can close on the same timeline as other programs.

Myth: Sellers should avoid VA offers. Reality: VA buyers are often strong, and the VA’s lower default rates can be a positive signal.

Myth: VA loan amounts are capped at the county limit. Reality: Full entitlement borrowers are not bound by traditional loan limits.

How VA Compares to FHA, USDA, and Conventional in Kentucky

Program

Down Payment

Monthly Mortgage Insurance

Credit Flexibility

Geographic Restrictions

VA

0 percent for most buyers

None

High

No rural requirement

FHA

3.5 percent minimum

Required (MIP)

High

No rural requirement

USDA

0 percent

Required (guarantee fee)

Medium

Must be in eligible rural areas

Conventional

3 to 5 percent or more

PMI required below 20 percent down

Medium to high

No rural requirement

Who Is a Good Fit for a Kentucky VA Loan?

Eligible veterans and service members who want zero down financing

Borrowers with moderate credit who have strong residual income

Homebuyers planning to live in the property as a primary residence

Veterans with a qualifying VA disability rating who can benefit from a funding fee exemption

Ready to explore your VA loan options in Kentucky or see how your eligibility, credit, and income line up with current guidelines?

Contact Joel Lobb, Mortgage Loan Officer (NMLS 57916) to review your situation, run numbers, and map out your next steps toward homeownership.

This is not a commitment to lend. All loans are subject to credit approval, property approval, and underwriting guidelines. Programs, terms, and guidelines are subject to change without notice.

{

“@context”: “https://schema.org”,

“@graph”: [

{

“@type”: “LocalBusiness”,

“@id”: “https://kentuckyvamortgage.com/#localbusiness”,

“name”: “Joel Lobb – Kentucky VA Mortgage Loan Officer”,

“image”: “https://kentuckyvamortgage.com/wp-content/uploads/joel-lobb-photo.jpg”,

“url”: “https://kentuckyvamortgage.com/”,

“telephone”: “+1-502-905-3708”,

“priceRange”: “$$”,

“description”: “Mortgage loan officer specializing in VA, FHA, USDA, KHC and conventional home loans for veterans, first-time homebuyers and move-up buyers across Kentucky.”,

“address”: {

“@type”: “PostalAddress”,

“streetAddress”: “10602 Timberwood Cir STE 3”,

“addressLocality”: “Louisville”,

“addressRegion”: “KY”,

“postalCode”: “40223”,

“addressCountry”: “US”

},

“geo”: {

“@type”: “GeoCoordinates”,

“latitude”: 38.243,

“longitude”: -85.560

},

“areaServed”: [

{

“@type”: “State”,

“name”: “Kentucky”

}

],

“openingHoursSpecification”: [

{

“@type”: “OpeningHoursSpecification”,

“dayOfWeek”: [

“Monday”,

“Tuesday”,

“Wednesday”,

“Thursday”,

“Friday”

],

“opens”: “09:00”,

“closes”: “18:00”

}

],

“sameAs”: [

“https://www.mylouisvillekentuckymortgage.com/”,

“https://kentuckyfirsttimehomebuyer.com/”,

“https://www.facebook.com/joellobbmortgage”,

“https://www.linkedin.com/in/joellobb”

]

},

{

“@type”: “FAQPage”,

“@id”: “https://kentuckyvamortgage.com/2025/02/25/va-mortgage-loan-guide-for-kentucky/#faq”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “What credit score do I need for a VA mortgage in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “The VA program itself does not set a minimum credit score. Most Kentucky lenders look for scores in the 580 to 620 range, with stronger pricing typically starting at 620 and above. Final approval also depends on your overall credit history, income, debts and residual income, not just the score.”

}

},

{

“@type”: “Question”,

“name”: “Can I buy a home in Kentucky with zero down using a VA loan?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes. Most eligible VA borrowers in Kentucky can buy with zero down payment. A down payment may only be needed if you have reduced entitlement, if you are purchasing far above standard limits with partial entitlement, or if you choose to put money down to lower your payment or funding fee.”

}

},

{

“@type”: “Question”,

“name”: “Does a VA loan require monthly mortgage insurance?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “No. VA mortgages do not have monthly private mortgage insurance. Instead, there is usually a one-time VA funding fee at closing, which can often be financed into the loan amount. Some veterans with qualifying VA disability benefits and certain other categories are exempt from the funding fee.”

}

},

{

“@type”: “Question”,

“name”: “How long after bankruptcy or foreclosure can I get a VA loan?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “For most Kentucky VA borrowers, the typical waiting period is at least two years after a Chapter 7 bankruptcy discharge or a foreclosure. For a Chapter 13 bankruptcy, you may be eligible after at least 12 months of on-time plan payments with trustee approval. Exact timelines can vary by lender and overall file strength.”

}

},

{

“@type”: “Question”,

“name”: “What types of properties are eligible for VA financing in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Eligible properties generally include primary residence single-family homes, VA-approved condominiums, townhomes, certain manufactured homes that meet VA and lender guidelines, and two- to four-unit properties where you live in one unit. Investment properties and short-term rentals that you do not occupy as your primary home are not eligible.”

}

},

{

“@type”: “Question”,

“name”: “How important is residual income for a VA loan approval?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Residual income is a key part of VA underwriting. It represents the amount of money left over each month after your major expenses and debts are paid. The VA uses regional residual income tables based on family size, and Kentucky is in the South Region. Strong residual income can support approvals at higher debt-to-income ratios and is one reason VA loans tend to perform well.”

}

},

{

“@type”: “Question”,

“name”: “How does a Kentucky VA loan compare to FHA, USDA and conventional financing?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “VA loans typically offer zero down payment, no monthly mortgage insurance, flexible credit guidelines and strong protections for eligible veterans and service members. FHA loans require a minimum down payment and include mortgage insurance. USDA loans offer zero down but are limited to eligible rural areas and include a guarantee fee. Conventional loans can be attractive for high-credit borrowers with larger down payments. The best choice depends on your eligibility, location, credit profile and goals.”

}

},

{

“@type”: “Question”,

“name”: “Who can help me start a VA mortgage in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Borrowers can work with a lender or mortgage loan officer experienced with Kentucky VA loans. Joel Lobb is a mortgage loan officer based in Louisville, Kentucky who focuses on VA, FHA, USDA and KHC programs and can review your eligibility, run payment scenarios and guide you from preapproval through closing.”

}

}

]

}

]

}

{kind=link}

You must be logged in to post a comment.