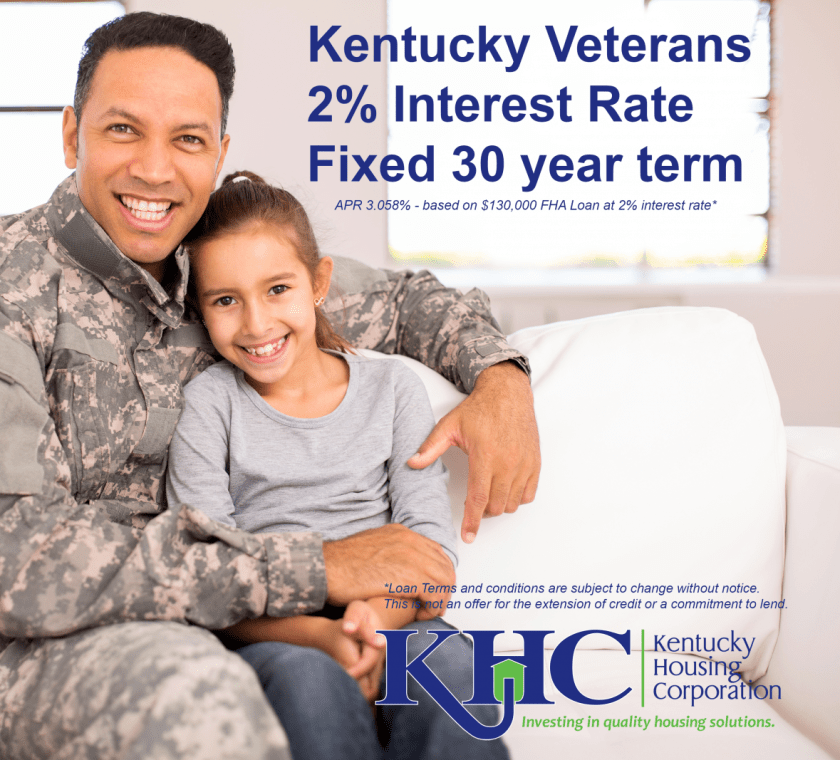

Home Loans for Kentucky’s Military Veterans

Kentucky Housing Corporation (KHC) has $3 million available in Mortgage Revenue Bond (MRB), special funding, for active or non-active duty veterans at 2 percent interest rate, fixed for 30 years. This special funding program is available on a first-come, first-served basis starting Wednesday, September 6, 2017, with new reservations.

FIND A KHC-APPROVED LENDER TO APPLY

This homeownership program is targeted to:

- Households whose gross annual income does not exceed $40,000.

- An existing or new construction property (purchase price limit $130,000).

- 620 minimum credit score.

- FHA, VA, or RHS first mortgage options.

- Households who include active duty or non-active duty veterans. Documentation may include but not limited to:

- Leave and Earnings Statement (LES)

- DD214 – Discharge from Active Duty

- VA Award Letter

- Must meet insuring agency guidelines.

- Available statewide.

Down payment Assistance Programs (DAP) available up to $6,000. Qualifications apply.

How to Apply

For all KHC loans, a home buyer must apply through a KHC-approved lender. We partner with approved lenders across the state to provide you with the best mortgage loan options. By doing this, the buyer will know how much house they can afford based on income and debts. KHC’s loans are subject to certain restrictions that the lender will see if meet the qualifying guidelines. Additionally, the lender will be able to recommend any KHC down payment assistance for which you may qualify.

APR 3.058% – based on $130,000 FHA loan at 2% interest rate.

|

Operation KY Home – MRB Special Funding Program

KHC has $1.8 million available in MRB, Special Funding, for active or non-active duty veterans at a 2 percent interest rate, fixed for 30 years. This special funding program is available on a first-come, first-served basis.

More information is available at www.OperationKYHome.com.

|

You must be logged in to post a comment.