VA loans help active duty, reserves, and veterans buy a house with no down payment and no mortgage insurance monthly making it one of the best loans out there while getting a low 30 year fixed rate loan based on market trends.

VA loans are not just for first-time home buyers, and they’re not restricted to low-income applicants. Here are the requirements you’ll need to meet to qualify for an VA loan

1. Consistent income and work history for last two years to support mortgage payment

In general, lenders want to see that you’ve worked for a year or two in the same field (if not the same employer). Consistent two year history needed, does not have to be same employer.

2. Debt to income ratio for VA loans.

The biggest factor in qualifying for an VA loan is whether you can afford the payment. As a rough guideline:

- your mortgage payment must not be more than 1/3 of your income (before taxes) and

- your mortgage payment PLUS other monthly debt payments (car loan, credit cards) must not be more than 43 percent of your income for a manual underwrite, or can go higher on the debt ratios if you get an automated approval through Desktop Underwriting AUS system.

- Car insurance, cell phone bills, utility bills are not included in the debt to income ratio just the monthly payments on the credit report and child support .

3. Zero Down Payment

There is no minimum credit score for VA loans, but in reality most lenders will wants a 620 score. However, we deal with some lenders that will go down to a 560 credit score but be prepared to get a lot of documentation to support your lower credit score.

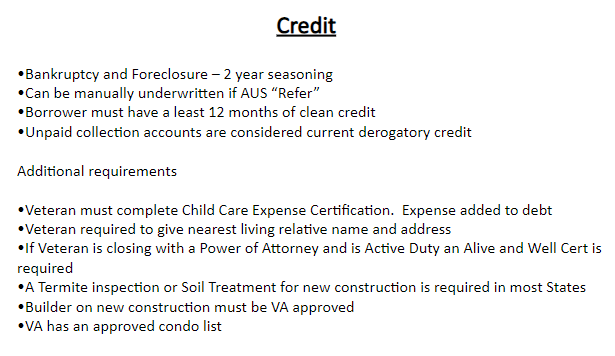

When Can I Get a VA Loan After Foreclosure, Bankruptcy, or Short Sale?

Every once in a while, bad things happen to good people. Whether credit issues result from financial mismanagement or other circumstances, VA home loan guidelines are very forgiving. So, how long after a foreclosure, short sale, or bankruptcy can you get a VA loan?

- Foreclosure seasoning = 2 years, 1 year if proven out of borrower’s control

- Short sale seasoning = Same as foreclosure, but if not lates prior to short sale then no seasoning required

- Bankruptcy waiting period = Chapter 7 seasoning is 2 years from discharge date. Chapter 13 seasoning is at least 12 months from filing

A key VA home loan requirement after major credit events like these is re-established credit. Therefore, showing on-time rent and other credit references may show recovery from a foreclosure, short sale, or bankruptcy.

Rent Verification for VA Loans With Low Scores

For lower credit scores on VA or any other type of mortgage loan, rent or mortgage history is very important. A previous housing history is a good indicator of how someone will pay a new house payment. So lenders take rent very seriously. The most weight is given to a rent history proven by cancelled checks. Then a buyer proving on time payment history through checks shows the buyer is the one who actually made the payments. Plus it shows they were made on time and there is no disputing this. Next, rent payments verified through a rental company is good. The weakest would be rental payments made to an individual. In cases where payments are made to individuals, additional documentation may be required. For instance, cancelled checks or proof of withdrawal from a bank account for 12 months would help.

Keep in mind, using alternative credit is not a way to ignore a bad credit report or score. Alternative credit is a way of proving a more solid or in depth payment history than the credit report shows.

VA Mortgage Loan Checklist

- Signed and dated Statement of Service Letter (Ask us if we need it though)

- DD214 (if no longer in the military)

- Current LES

- Most recent W2 and Tax Return

- Most recent bank statement (all pages of actual monthly statement)

- Photo identification

- Military transfer orders – if transferring to a new base

We will request your COE, status report, complete your application, and discuss your mortgage options. Our goal is to have educated, confident, and approved buyers!

You must be logged in to post a comment.