I have successfully originated over 200 VA Home loans in Kentucky. Put my experience to work for you. Call or text me today at 502-905-3708 or email me at Kentuckyloan@gmail.com-This website is not affiliated with the VA or any other government agency. NMLS #57916 Equal Housing Lender. Same Day Approvals, Fast Closings, and a Local Veteran offering VA Home Loans in Kentucky. Free Credit Report and Pre-Approvals NMLS# 57916 Joel Lobb Loan Originator, Company NMLS ID 1738461 . Equal Housing Lender

Are you a Kentucky veteran or active-duty service member dreaming of owning your own home in the Bluegrass State? The VA loan program is a powerful tool designed specifically to help you achieve that dream. With benefits like no down payment and no private mortgage insurance, it’s an incredible opportunity. But navigating the qualification process can feel overwhelming. That’s where I come in.

As your dedicated mortgage guide, I’ll break down what it takes to qualify for a VA loan in Kentucky and explain why working with me—Joel Lobb, Senior Loan Officer—will simplify your path to homeownership.

VA Loans in Kentucky: A Veteran’s Path to Homeownership

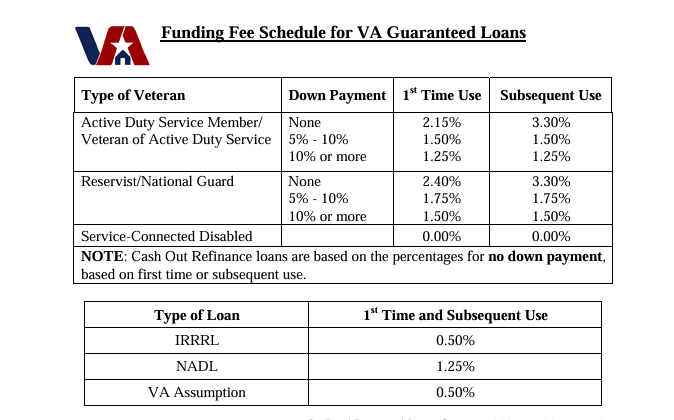

If you’re a veteran, active-duty service member, or eligible surviving spouse looking to buy a home in Kentucky, the VA loan program is one of the most powerful mortgage options available. Backed by the U.S. Department of Veterans Affairs, VA loans allow zero down payment, no monthly mortgage insurance, and competitive interest rates.

Who Is Eligible for a VA Mortgage Loan in Kentucky?

The VA does not have a minimum credit score requirement, but most Kentucky lenders typically look for a FICO score of 580–620+. That said, manual underwriting is available for scores as low as 500 with strong compensating factors.

Have bad credit, collections, or charge-offs? VA loans are more forgiving:

Medical collections are often excluded.

Charge-offs do not always need to be paid.

Student loans are handled differently than FHA or conventional.

Most lenders prefer a 2-year stable work history, but gaps or job changes are acceptable with a written explanation.

Residual Income Requirement:

VA loans use residual income instead of front-end housing ratios. You must have enough income left over after all monthly obligations to cover living expenses.

Debt-to-Income Ratio (DTI):

Max DTI: 41% (can go higher with strong residual income or DU/LP approval)

If you don’t qualify through DU or LP, manual underwriting is an option. This requires stronger documentation, compensating factors like low DTI or extra assets, and no major credit issues in the last 12 months.

Submit financial documents: pay stubs, W-2s, tax returns, bank statements

Get COE and credit report pulled

Start home shopping with a Realtor familiar with VA guidelines

Lock in your interest rate and complete the underwriting process

Close and move into your new home!

Why Work with Joel Lobb?

With over 20 years of mortgage experience and a Army Veteran and more than 1,300 families helped, Joel Lobb is a trusted mortgage advisor for Kentucky veterans. His team provides:

NMLS 57916 | The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

You must be logged in to post a comment.