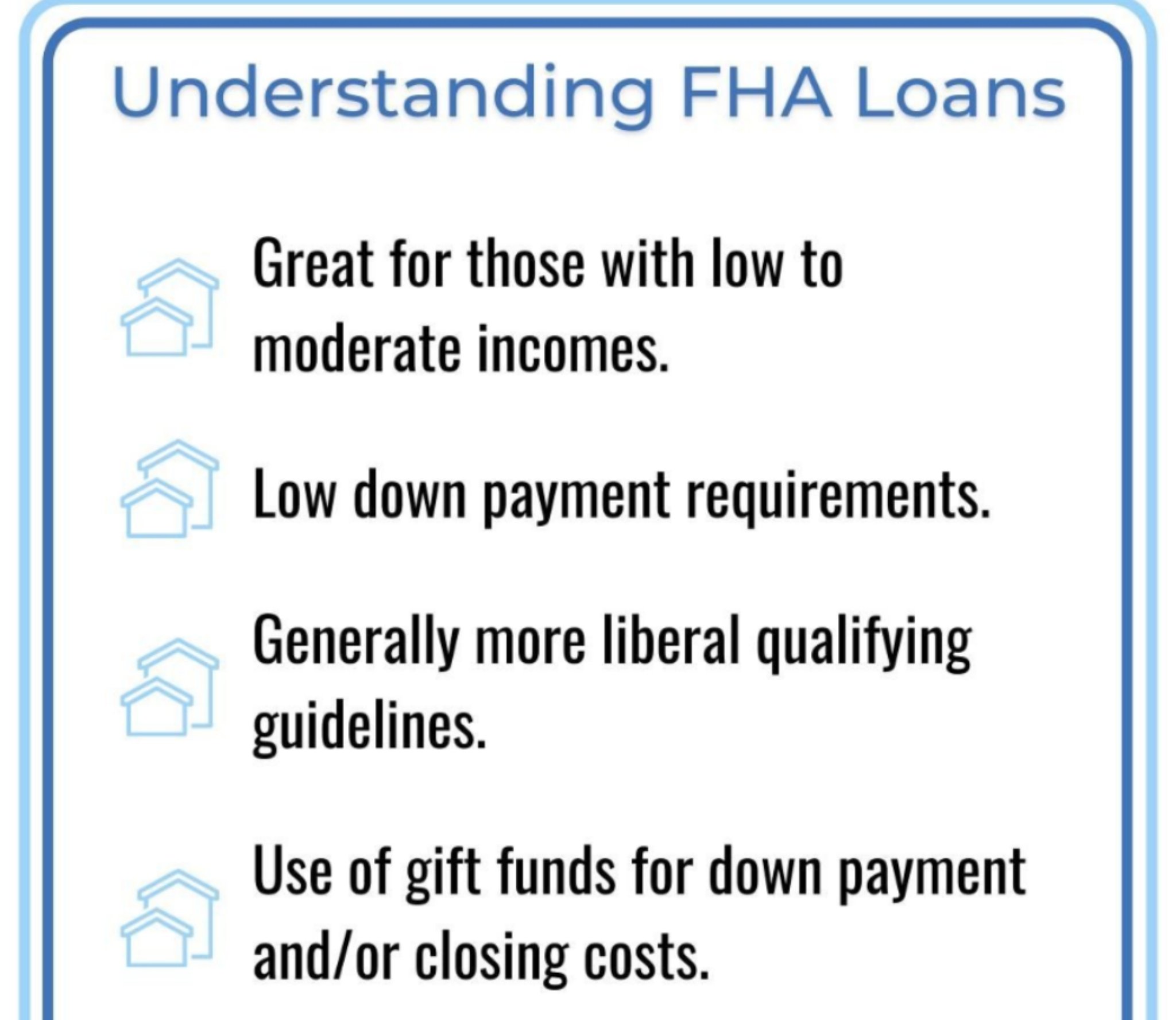

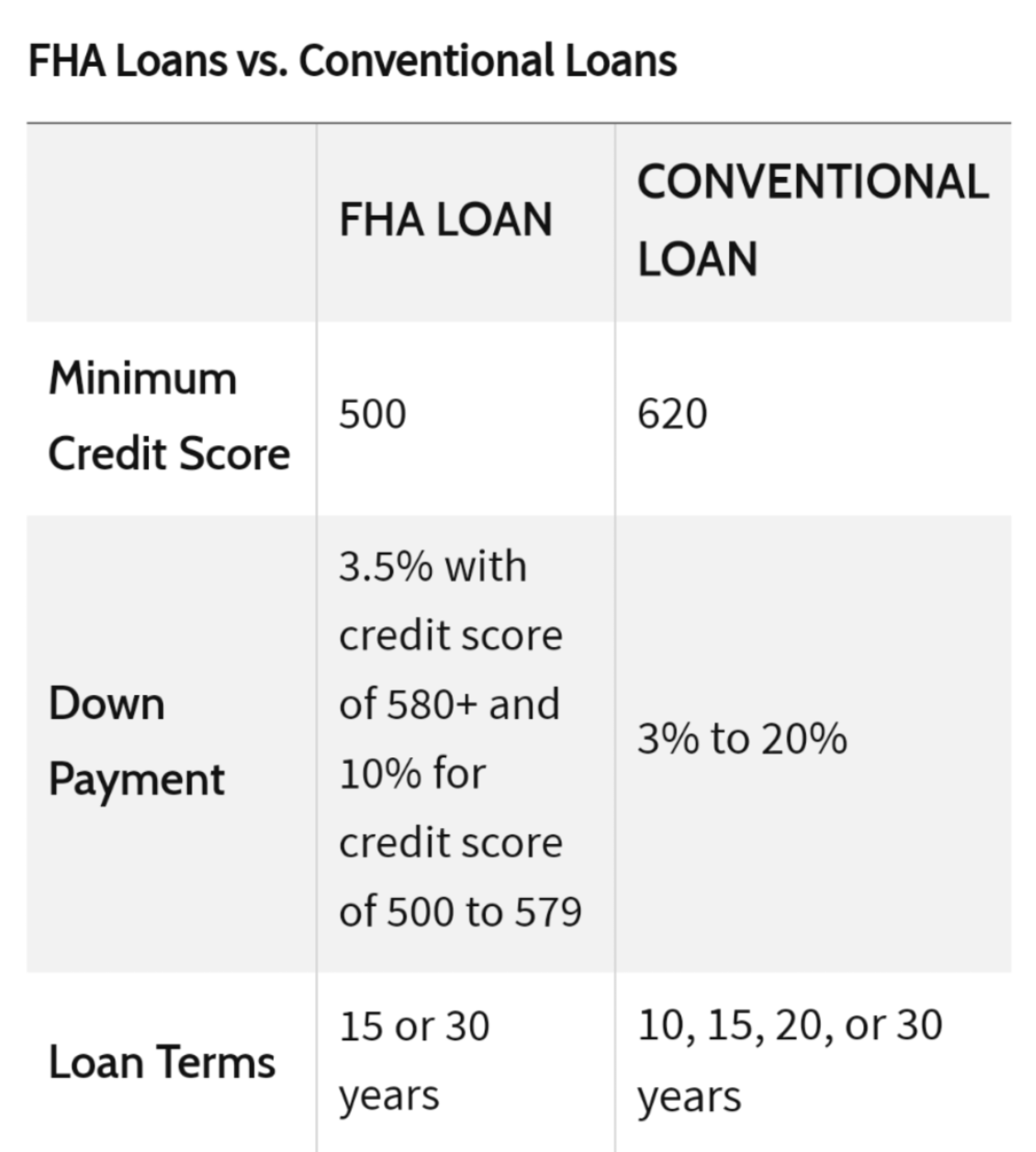

FHA Minimum Down Payment

Effective January 1, 2009, the minimum down payment required on an FHA loan is 3.5% of the purchase price.Any deposit (usually called earnest money) that you are required to give to your realtor at the time of an accepted purchase contract will count towards your 3.5% down payment. The appraisal fee collected at the time of inspection will also count towards your 3.5% down payment.

If, for example, you are purchasing a $100,000 house, your minimum down payment required would be $3,500. If your seller/realtor required you to put down $500 in earnest money on top of the $300 for your appraisal, your down payment would be lowered to $2,700 ($3,500 – $500 – $300 = $2,700).

Down Payment As A Gift

If a borrower does not have 3.5% of his or her own money to put down towards the home purchase, FHA allows that amount to be in the form of a gift to the borrower. The gift must be from a qualified source, such as a family member, employer or significant other. The source of the gift must be able to provide proof that they have the money in an account registered in their name prior to transfer to the borrower.

In some areas, this gift may also be grant money from a state or local municipality, if such funds are available.

Louisville Kentucky Mortgage Loans

FHA Minimum Down Payment

Effective January 1, 2009, the minimum down payment required on an FHA loan is 3.5% of the purchase price.

Any deposit (usually called earnest money) that you are required to give to your realtor at the time of an accepted purchase contract will count towards your 3.5% down payment. The appraisal fee collected at the time of inspection will also count towards your 3.5% down payment.

If, for example, you are purchasing a $100,000 house, your minimum down payment required would be $3,500. If your seller/realtor required you to put down $500 in earnest money on top of the $300 for your appraisal, your down payment would be lowered to $2,700 ($3,500 – $500 – $300 = $2,700).

Down Payment As A Gift

If a borrower does not have 3.5% of his or her own money to put down towards the home purchase, FHA allows that amount to…

View original post 77 more words

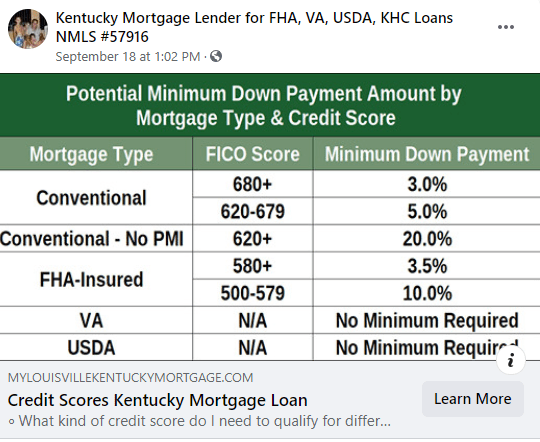

What is the minimum credit score I need to qualify for a Kentucky FHA, VA, USDA and KHC Conventional mortgage loan

What is the minimum credit score I need to qualify for a Kentucky FHA, VA, USDA and KHC Conventional mortgage loan

You must be logged in to post a comment.