VA home loans can be used to:

– Buy a home, a condominium unit in a VA-approved project

– Build a home

– Buy a manufactured home and/or lot

VA Home loan is a government guarantee for a portion of the home loan, it is not a guarantee that you will receive a loan. You still need to have:

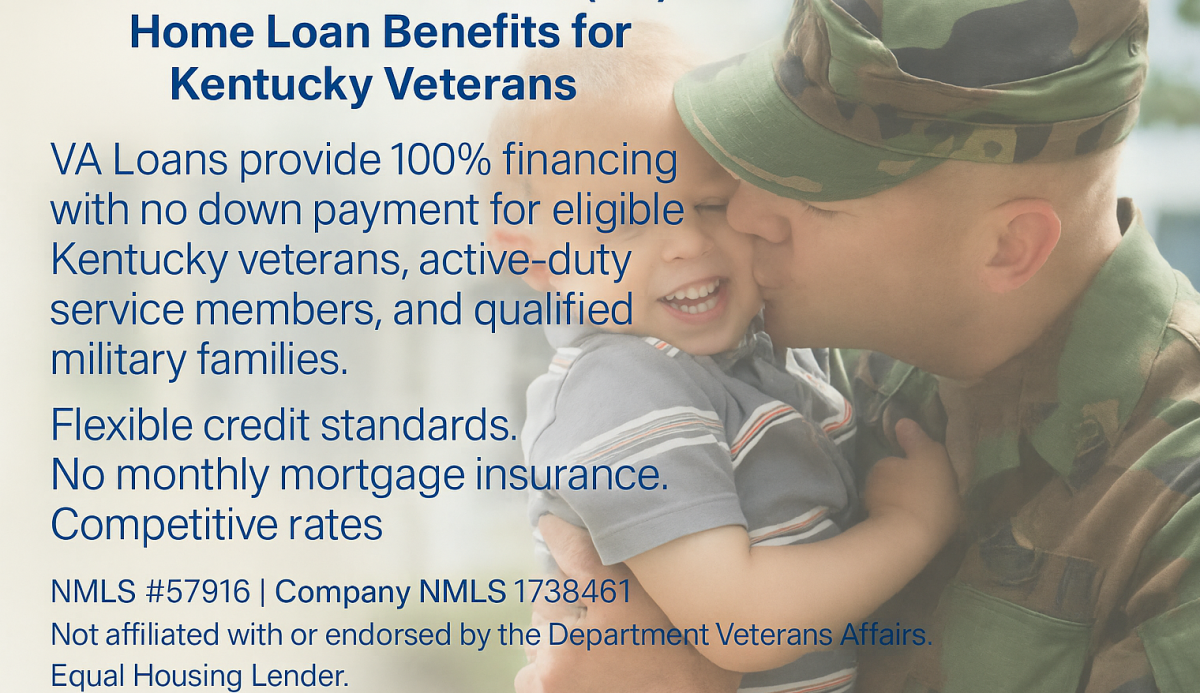

Suitable Credit. Due to the government guarantee for a portion of the loan, this allows lenders greater flexibility on credit scores. In today’s lending climate, most VA lenders require a score of at least 620. If your spouse will be obligated on the loan, he or she will need to hit the same benchmark.

The average FICO score for VA borrowers is 708, compared to 750 to 770 scores for conventional loans backed by Fannie Mae and Freddie Mac, respectively,

Sufficient Income to qualify for the amount you are requesting.

In order to apply for the VA Loan one needs to get ” A certificate of Elgibilty” This verifies to the lender that you qualify for a VA backed home loan.

Many lenders will help get the Certificate for you or you can apply for it online by going to the veterans affairs portal. You will need your DD 214 or if you are still on active duty you will need a statement of service.

The home that is being purchased must be occupied by the veteran/active duty member.

Veteran Must have been discharged under conditions other than dishonorable and meet the service requirements below

Each era has its own specific requirement, so be careful to match your service dates with eligibility requirement.

If one is still on active duty or are currently serving in the Reserve or national guard the below are the requirements.

If one is on active duty in order to qualify you need to have served at least 90 continuous days

As a Reservist or National Guard member one needs to have at least 90 days active duty. Another way to become eligible is to have served at least 6 years as a reservist or national guardsman and been honorably discharged. There are several other ways that one can qualify as outlined below.

VA website has more detail eligibility guidelines. go to benefits.va. gov

The VA Home Loan program is one of the better benefits we as veterans receive. I should know, I have used this program to purchase my own home.

This is just one in series of information videos that details the VA Home Loan Program. I hope that the information in this one has been helpful.

As Always, If you have any questions, regardless of your location feel free to call or contact me. Thank you and God Bless.

You must be logged in to post a comment.