VA Refinance in Louisville Kentucky: Complete Guide to IRRRL, Cash-Out & Rate-and-Term Options

As a Kentucky mortgage lender with over 20 years of experience, I’ve helped more than 1,300 veterans and active military members refinance their VA home loans to save money, access home equity, and achieve better loan terms. If you’re a Louisville area veteran with an existing VA mortgage, understanding your refinance options could save you thousands of dollars over the life of your loan.

This comprehensive guide covers the three main VA refinance options available to Kentucky veterans: VA Interest Rate Reduction Refinance Loans (IRRRL), cash-out refinancing, and rate-and-term refinancing.

Ready to Explore Your Refinance Options?

Get a free pre-qualification and see your refinance options today. Same-day approvals on most applications.Call or Text: 502-905-3708Email: kentuckyloan@gmail.com

What is a VA Refinance Loan?

A VA refinance loan allows veterans who already have a VA mortgage to refinance their existing home loan into new terms. Unlike traditional cash-out refinancing, VA refinancing leverages your existing VA home loan entitlement, making the process faster and more affordable.

Why refinance your VA mortgage?

- Lower monthly payments through reduced interest rates

- Access home equity with cash-out refinancing for home improvements, debt consolidation, or other expenses

- Shorter loan terms to pay off your mortgage faster

- Convert ARM to fixed-rate mortgages for payment stability

- Eliminate PMI with no requirement for mortgage insurance

If you’re curious about whether refinancing makes sense for your specific situation, contact me at 502-905-3708 for a free, no-obligation consultation.

Understanding VA Loan Entitlement for Refinancing

Before exploring specific refinance programs, it’s important to understand your VA loan entitlement. Your entitlement is your “eligibility” to use the VA loan benefit.

Key entitlement facts:

- The basic entitlement available to each eligible veteran is $36,000

- If you’ve already used your entitlement for a previous VA purchase, you can reuse it for a refinance

- A Certificate of Eligibility (COE) from the VA proves you’ve used your entitlement before

- Lenders can verify entitlement status without requiring a new COE in some cases

For IRRRL refinances specifically: You only need to certify that you previously occupied the home—the occupancy requirements are different from purchase loans.

Uncertain about your entitlement status? I can help you determine your eligibility and available options at no cost. Call or text 502-905-3708 or email kentuckyloan@gmail.com.

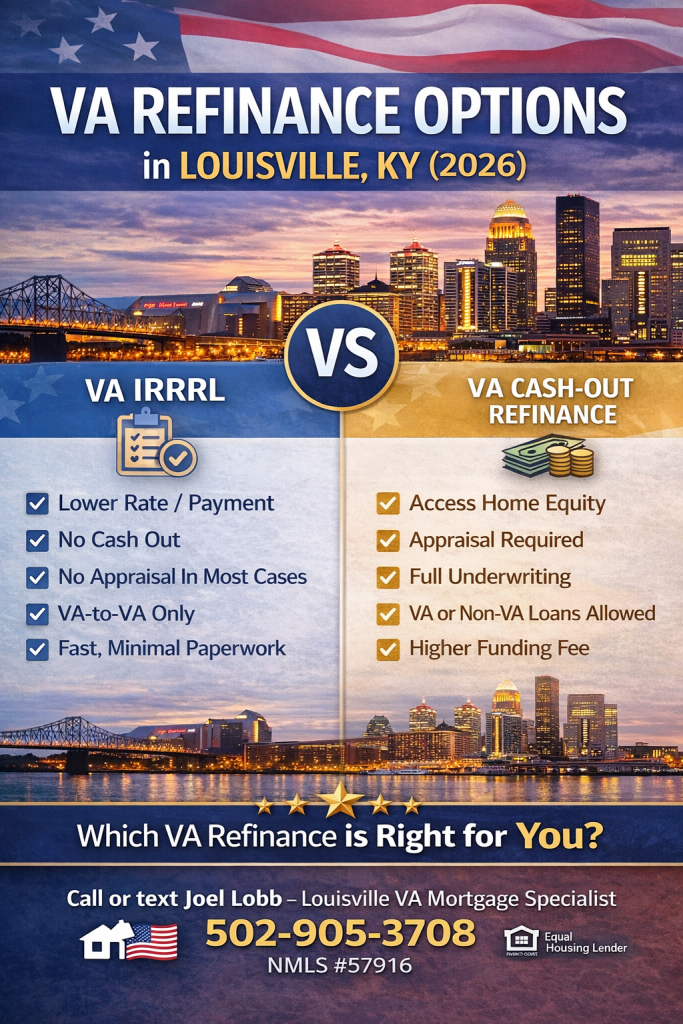

VA IRRRL Refinance (Interest Rate Reduction Refinance Loan) – The Streamline Option

The VA Interest Rate Reduction Refinance Loan (IRRRL), also called a VA streamline refinance, is the fastest and simplest way for veterans to lower their interest rate and reduce monthly payments.

How Does a VA IRRRL Streamline Refinance Work?

The IRRRL is designed specifically to refinance an existing VA-to-VA mortgage into better terms. The VA guarantees the new loan just as it did your original mortgage, which means lenders can approve IRRRLs with minimal paperwork.

The streamline advantage:

- No appraisal required

- No underwriting/credit check required

- No Certificate of Eligibility (COE) needed (though you can provide one)

- Loan can be approved in as few as 7-10 business days

- All closing costs can be rolled into the new loan amount

- Minimal documentation needed

IRRRL Eligibility Requirements

To qualify for a VA IRRRL streamline refinance, you must meet these basic criteria:

- You already have a VA loan – The IRRRL is only for refinancing an existing VA mortgage

- VA-to-VA refinance – You’re refinancing a VA loan into another VA loan (you cannot use IRRRL to refinance into a conventional or FHA loan)

- You previously occupied the home – Unlike purchase loans, you don’t need to occupy the property now; you just need to certify you did in the past

- Your entitlement must be available – If you’ve used your full entitlement for another property without paying off the original loan, you may have limited options

Subordination requirement: If you have a second mortgage (home equity line of credit, second lien, etc.), the holder must agree to subordinate (place) that loan below your new VA mortgage. If they won’t, the IRRRL may not be possible.

IRRRL Closing Costs & Funding Fee

One of the biggest advantages of IRRRL refinancing is the ability to do it with “no money out of pocket” by rolling all costs into the new loan amount.

Typical IRRRL costs include:

- VA funding fee (reduced for IRRRL – typically 0.55% of the loan amount)

- Title insurance and title search

- Recording fees and transfer taxes (varies by county)

- Appraisal fee (if lender requires one, though not mandatory)

- Loan origination fee

VA Funding Fee Exemptions

You do NOT pay a funding fee if you are:

- A veteran receiving VA compensation for a service-connected disability

- A veteran entitled to receive compensation for a service-connected disability (even if receiving military retirement pay)

- A surviving spouse of a veteran who died in service or from a service-connected disability

Real-world example: On a $200,000 IRRRL refinance, a typical VA funding fee of 0.55% equals $1,100. If closing costs total $3,500, the entire amount can be rolled into your new loan, meaning zero cash at closing.

IRRRL Rate Reduction Rule – Do You Have Enough Savings?

The VA doesn’t require a minimum rate reduction for an IRRRL, but lenders do. Most lenders require a “net tangible benefit,” which typically means:

- At least 0.5% rate reduction, though

- 1% or more is ideal to ensure meaningful monthly savings

Important warning: Some lenders promote the IRRRL as a way to reduce your loan term from 30 years to 15 years. This can dramatically increase your monthly payment, even with a lower interest rate. For example:

- Current: 30-year loan at 4.5% on $200,000 = $1,013/month

- Refinance: 15-year loan at 3.5% on $200,000 = $1,428/month (a $415 monthly increase!)

While you’d save interest over time, this payment increase might not be affordable. Always run the numbers carefully before pursuing a shorter loan term.

IRRRL Application Process – Timeline & Steps

- Submit application – Basic loan application (NMLS Form 1003 or lender-specific form)

- Verification – Lender confirms previous VA entitlement use (may contact VA directly)

- Appraisal (if required) – Most lenders skip this; if needed, typically 3-5 days

- Processing – Lender prepares documents and underwriting report (3-5 business days)

- Approval – Clear to close, no conditions (typically days 7-10)

- Closing – Sign documents and fund the loan

- Funding – New loan funds and existing mortgage is paid off

Fast approval: Most IRRRLs receive approval in 7-14 days with my office.

VA Cash-Out Refinance Loans – Access Your Home Equity

A VA cash-out refinance allows you to refinance your existing VA mortgage for more than you currently owe and receive the difference in cash. This is ideal for home improvements, debt consolidation, education expenses, or other major financial needs.

How Does a VA Cash-Out Refinance Work?

When you do a cash-out refinance, your new VA loan amount includes:

- The balance you owe on your existing mortgage

- Plus additional funds you’re borrowing (the “cash-out” amount)

- Closing costs (which can be rolled into the loan)

Example: If your home is worth $250,000 and you owe $150,000, a VA cash-out refinance could allow you to borrow up to $200,000 or more, receiving $50,000+ in cash while refinancing your original debt.

The new loan is still a VA loan with the same benefits: no down payment, no PMI, and VA guarantee protection.

VA Cash-Out Refinance Eligibility

Cash-out refinancing has slightly stricter requirements than IRRRL:

- You must have a VA loan to refinance

- Loan-to-Value (LTV) limits apply – Generally, lenders allow cash-out up to 80% LTV (meaning your loan can be 80% of your home’s current value)

- Your home must appraise – Unlike IRRRL, appraisals are required for cash-out loans

- Income verification – Full underwriting including employment verification, credit review, and income documentation

- Debt-to-income ratio – Your total monthly debt (including the new mortgage) cannot typically exceed 43-50% of gross income

- Credit score – Minimum 580-620 FICO score (though better rates with 660+)

VA Cash-Out Refinance Uses & Benefits

Common uses for cash-out refinancing:

- Home improvements – Roof repairs, additions, kitchen remodels, HVAC systems

- Debt consolidation – Pay off credit cards, personal loans, or medical debt at a lower rate

- Education expenses – Fund college tuition or vocational training

- Emergency expenses – Major home repairs or family emergencies

- Investment – Real estate investments or business opportunities

- Vehicle purchase – Consolidate auto loans into one lower-rate mortgage

The math of consolidation: If you have $25,000 in credit card debt at 18% APR ($450/month), refinancing into a VA cash-out loan at 6% APR could drop your payment to $150/month while rebuilding your credit faster.

VA Cash-Out Refinance Loan Limits by County

VA doesn’t cap how much you can borrow, but lenders set limits based on:

- Your VA entitlement and available entitlement

- Your home’s appraised value

- Your income and credit qualifications

Jefferson County (Louisville) Loan Limits: For 2026, contact me for exact loan limits in your county, as they update annually. Generally, standard VA loans have no cap on borrowing, with limits applied based on your entitlement and the property value. To maximize your borrowing without a down payment, ensure you have sufficient available entitlement.

VA Cash-Out Timeline & Process

Cash-out refinancing takes longer than IRRRL because:

- Appraisal required – 7-10 days

- Full underwriting – 5-10 days

- Verification of employment/income – 2-5 days

- Clear to close – 2-5 days

Total timeline: 21-30 days, though my office frequently closes cash-out loans in 18-21 days.

VA Rate-and-Term Refinance – Traditional Refinancing

A rate-and-term refinance is a middle ground between IRRRL and cash-out refinancing. You refinance your existing loan without borrowing additional cash, but at a better interest rate or different term.

How Does Rate-and-Term Refinancing Work?

In a rate-and-term refinance:

- Your new loan amount is approximately equal to what you currently owe (plus closing costs)

- You’re not taking cash out

- Your loan term can change (e.g., 30 years to 20 years)

- Your interest rate is refinanced at current market rates

When to use rate-and-term refinancing:

- You need a better rate than IRRRL allows

- You’re converting an ARM (adjustable-rate) to a fixed-rate mortgage

- You want to shorten your loan term without taking cash out

- You prefer not to go through full cash-out underwriting

Rate-and-Term Eligibility

Rate-and-term refinancing sits between IRRRL and cash-out in terms of underwriting:

- Some lenders require simplified underwriting (not full)

- Appraisals may or may not be required

- Income verification typically required

- Credit check is standard

- Debt-to-income limits apply (usually 43-50%)

When to Choose Rate-and-Term vs. IRRRL

| Factor | IRRRL | Rate-and-Term |

|---|---|---|

| Rate reduction required | Usually 0.5%+ | Can refinance at higher rate if needed |

| Underwriting | Minimal – streamlined | Moderate – some verification |

| Timeline | 7-14 days | 15-25 days |

| Closing costs | ~$2,500-3,500 | ~$3,500-5,000 |

| Best for | Faster, easier refis | More flexibility, specific goals |

| ARM to fixed | Yes | Yes |

Comparison: IRRRL vs. Cash-Out vs. Rate-and-Term

| Feature | IRRRL | Cash-Out | Rate-and-Term |

|---|---|---|---|

| No appraisal | ✓ | ✗ (required) | ~ (varies) |

| No underwriting | ✓ | ✗ (full) | ~ (simplified) |

| Access cash | ✗ | ✓ | ✗ |

| Fastest approval | ✓ (7-10 days) | ✗ (21-30 days) | ~ (15-25 days) |

| Best rate | ✓ (usually) | ~ | ~ |

| Flexibility | Limited | High | Moderate |

| Funding fee | 0.55% | 0.55%+ | 0.55%+ |

| Occupancy requirement | Previous only | Current property | Current property |

VA Funding Fees Explained – What You’ll Pay

All VA refinances include a funding fee (unless you’re exempt due to service-connected disability):

2026 VA Funding Fee Rates for Refinancing

For IRRRL (streamline) refinances:

- First-time refinancers, no down payment: 0.55% of loan amount

- Subsequent refinancers, no down payment: 0.55% (same as IRRRL)

- National Guard/Reserve: Slightly higher (about 0.575%)

For cash-out and rate-and-term refinances:

- First-time, no down payment: 2.3% of loan amount

- Subsequent users, no down payment: 3.6% of loan amount

- National Guard/Reserve: Higher percentages apply

Funding Fee Example:

• $200,000 IRRRL with 0.55% fee = $1,100

• $200,000 cash-out with 2.3% fee = $4,600

The good news? You can finance the funding fee into your new loan, so you don’t need to pay cash at closing.

Funding Fee Exemptions – You Might Not Pay

You’re exempt from the VA funding fee if you:

- Receive VA disability compensation for a service-connected disability (any percentage)

- Are entitled to receive compensation for service-connected disability but receive military retirement/active duty pay instead

- Are a surviving spouse of a veteran who died in service or from service-connected disability

If you’re exempt, provide VA documentation (VA letter of eligibility, DD Form 214, or similar) to your lender.

VA Loan Entitlement & Limits for Louisville, Kentucky

Your VA entitlement determines how much you can borrow without a down payment. The basic entitlement is $36,000, but if you have significant available entitlement, you can borrow much more.

How Entitlement Works

Example:

• Basic entitlement: $36,000

• If your home value is $250,000 and you’re fully qualified:

• You can borrow up to 4x your available entitlement without a down payment

• $36,000 × 4 = $144,000 maximum

• So lenders would typically fund up to $144,000 without requiring a down payment

However, if you have a higher purchase price or the property appraises for more, you may need to put money down.

For refinancing: Your available entitlement is what matters. If you have restored entitlement (paid off a previous VA loan), you have more borrowing capacity.

Jefferson County, Kentucky Loan Limits (2026)

Contact me for exact loan limits in your county, as they update annually. Generally:

- Standard VA loans: No cap on borrowing

- Loan limits apply based on your entitlement and income qualification

- To maximize your borrowing without a down payment, ensure you have sufficient available entitlement

Common VA Refinance Questions Answered

Do I Need a Certificate of Eligibility for an IRRRL?

No, a new Certificate of Eligibility (COE) is not required for IRRRL refinances. Your lender can verify entitlement through the VA’s online system. However, if you have your COE handy, you can provide it to speed up verification.

Can I Refinance an ARM (Adjustable-Rate Mortgage) with VA?

Yes! Converting an ARM to a fixed-rate VA mortgage is a common and smart use of IRRRL or rate-and-term refinancing. When interest rates are low, this can lock in predictable payments for 30 years.

How Much Will My Monthly Payment Drop?

The payment reduction depends on:

- Interest rate reduction – Each 1% lower rate saves roughly $215/month per $100,000 borrowed

- Loan term – Shorter terms = higher payments but less total interest

- Loan amount – Larger loans have proportionally larger payment changes

Quick calculation: Refinancing $150,000 from 5% to 4% typically saves ~$165/month.

Can I Refinance if I Have Bad Credit?

Yes, VA refinancing is more flexible than conventional financing:

- IRRRL: No credit check required

- Cash-out/Rate-and-term: Minimum credit score typically 580-620

- Even with recent delinquencies, many veterans qualify

If you have credit concerns, discuss them with me. I’ve helped veterans with bankruptcies, foreclosures, and late payments refinance successfully.

How Long Does Refinancing Take?

- IRRRL: 7-14 days (fastest)

- Rate-and-term: 15-25 days

- Cash-out: 21-30 days

My office often beats these timelines with efficient processing.

What Happens to My Current Mortgage During Refinancing?

Your old mortgage remains active until the new loan funds and pays it off. Once the new loan closes:

- The new lender sends funds to the old lender

- Old mortgage is paid off in full

- Your home title is transferred to the new lender

- You begin payments on the new mortgage

There’s no gap in coverage or risk of losing your home.

VA Refinance Success Stories from Louisville Veterans

Over 20+ years, I’ve helped thousands of Kentucky veterans refinance. Here are real-world examples:

Example 1 – IRRRL Streamline Savings

Jim’s Story: Jim, a Louisville veteran, had a VA mortgage at 5.5% on $180,000. When rates dropped to 4.25%, he did an IRRRL refinance in just 10 days. His monthly payment dropped from $1,022 to $886—saving him $136/month or $1,632/year. No appraisal, no underwriting. Clean and simple.

Example 2 – Cash-Out for Home Improvement

Maria’s Story: Maria, a Fort Knox-area veteran, had $280,000 owed on her home valued at $380,000. She refinanced with a $300,000 VA cash-out loan, receiving $20,000 to renovate her kitchen and update the home’s electrical system. Her payment only increased $150/month while adding home value and equity.

Example 3 – ARM to Fixed-Rate Security

David’s Story: David’s VA ARM mortgage was set to adjust upward from 3.8% to 5.2%. Before the adjustment, he refinanced into a 30-year fixed VA loan at 4.3%, locking in stability. His payment actually decreased while eliminating the risk of rising rates.

Why Work With Me for Your VA Refinance?

I’m Joel Lobb, NMLS #57916, and I’ve spent 20+ years specializing in Kentucky VA mortgages. Here’s what sets my service apart:

- ✓ Local expertise – I know Louisville, Jefferson County, Fort Knox, and all 120 Kentucky counties

- ✓ Fast approvals – Same-day pre-approval on most applications; average close in 18-21 days

- ✓ Transparent guidance – I explain all options without pressure and help you choose what’s best for YOUR situation

- ✓ Personal service – I answer my phone and attend most closings personally

- ✓ 1,300+ families helped – Over two decades of proven success

- ✓ Free pre-qualification – No hidden fees, no commitment

- ✓ 24/7 accessibility – Call or text me anytime

Your Next Steps

Ready to explore your refinance options?

- Call or text me at 502-905-3708 – I’ll discuss your current mortgage and goals

- Send your information to kentuckyloan@gmail.com – I’ll analyze your situation and options

- Complete a free pre-qualification – Same-day approvals on most applications

- Lock in your rate – Secure the best rate available

No pressure. No obligation. Just honest guidance from a Kentucky veteran mortgage expert.

Ready to Start Your VA Refinance?

Get a free pre-qualification today and discover how much you could save with VA refinancing.📞 Call or Text: 502-905-3708📧 Email: kentuckyloan@gmail.com🌐 Visit: http://www.kentuckyvamortgage.com

Important Disclaimers

This website and content are not endorsed by the VA, FHA, USDA, or any government agency. They are provided for educational purposes only.

Loan qualification: All loans are subject to:

- Income verification and credit approval

- Property appraisal and valuation (when required)

- Sufficient equity (LTV requirements)

- Debt-to-income ratio limits

- Final underwriting approval

Rate changes: Interest rates are subject to market conditions and change daily. Rates mentioned are examples only.

Equal Housing Opportunity: I am an Equal Housing Lender. I serve all applicants fairly regardless of race, color, national origin, religion, sex, familial status, or disability.

No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant. Equal Opportunity Lender.

NMLS#57916 | http://www.nmlsconsumeraccess.org/

Contact Information

Joel Lobb

Senior Loan Officer – Kentucky VA Mortgage Specialist

NMLS #57916 | Company NMLS #1738461

American Mortgage Solutions, Inc.

📞 Call/Text: 502-905-3708 (available 7 days a week)

📧 Email: kentuckyloan@gmail.com

🌐 Website: www.kentuckyvamortgage.com

Serving all 120 counties in Kentucky – Louisville, Lexington, Bowling Green, Owensboro, Covington, and beyond.

Same-day pre-approvals | Fast closings | Personal service | Expert guidance

Reblogged this on Kentucky First Time Home Buyer Programs for 2016 FHA, VA, KHC, USDA, RHS, Fannie Mae Loans in Kentucky and commented:

LOUISVILLE KENTUCKY VA REFINANCE FOR CASH OUT, RATE AND TERM, AND IRRRL STREAMLINE VA REFINANCE MORTGAGE”

LOUISVILLE KENTUCKY VA REFINANCE FOR CASH OUT, RATE AND TERM, AND IRRRL STREAMLINE VA REFINANCE MORTGAGE”