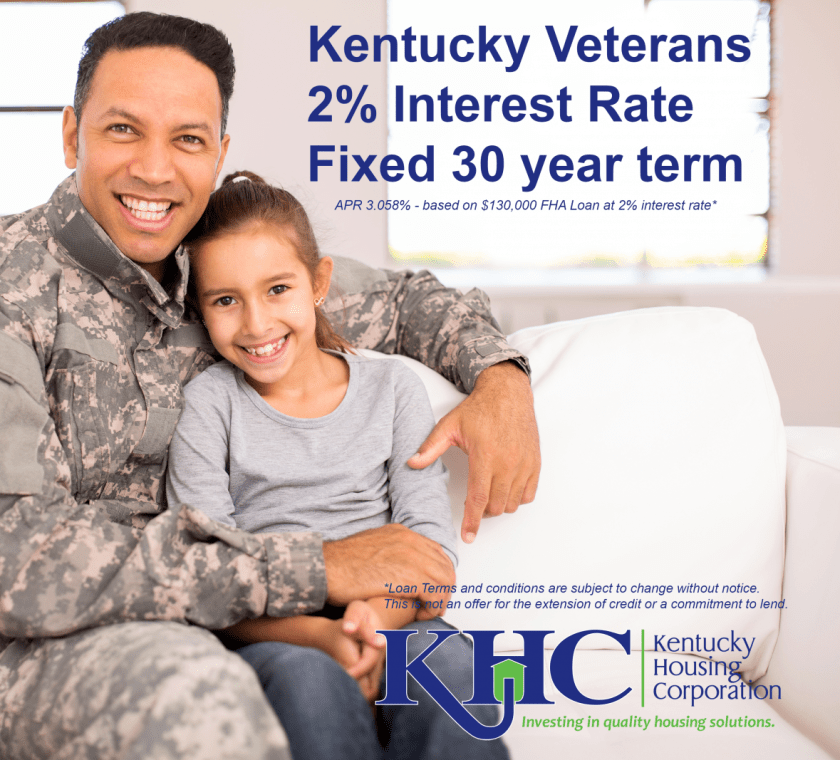

Kentucky Housing Corporation (KHC) has $3 million available in MRB, Special Funding, for active or non-active duty veterans at a 2 percent interest rate, fixed for 30 years. This special funding program is available on a first-come, first-served basis.

APR 3.058% – based on $130,000 FHA loan at 2% interest rate.

This program is targeted to:

Households whose gross annual income does not exceed $40,000.

An existing or new construction property (purchase price limit $130,000).

620 minimum credit score.

FHA, VA, or RHS first mortgage options.

Households that include active / non-active duty veterans or other persons receiving VA benefits.

Down payment Assistance Programs (DAP) available up to $6,000. Qualifications apply.

Documentation may include but not limited to:

Leave and Earnings Statement (LES)

DD214 – Discharge from Active Duty

VA Award Letter

Must meet insuring agency guidelines.

Available statewide.

Both Regular and Affordable DAP are available

2 percent interest rate, First time home buyer, fixed for 30 years, fort knox ky zero down loan, kentucky first time home buyer grant, kentucky housing corporation khc, khc, khc loans, khc rates ky, KHC’s (Kentucky Housing ) First Mortgage Government, ky first time home buyer, Louisville Kentucky First Time Home Buyer, mortgage rate, Real Estate, va loans ky, Zero down home loans

Call us today for a free pre-approval at 502-905-3708 or email your mortgage questions to kentuckyloan@gmail.com

—

Company ID #1364 | MB73346

Joel Lobb

Senior Loan Officer

(NMLS#57916)

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (

www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice. Manufactured and mobile homes are not eligible as collateral.

You must be logged in to post a comment.