Today, with lending standards tightening up, VA loans are making a comeback! Here are some quick facts regarding a VA loan:

A VA loan is designed for veterans and active duty military personnel.

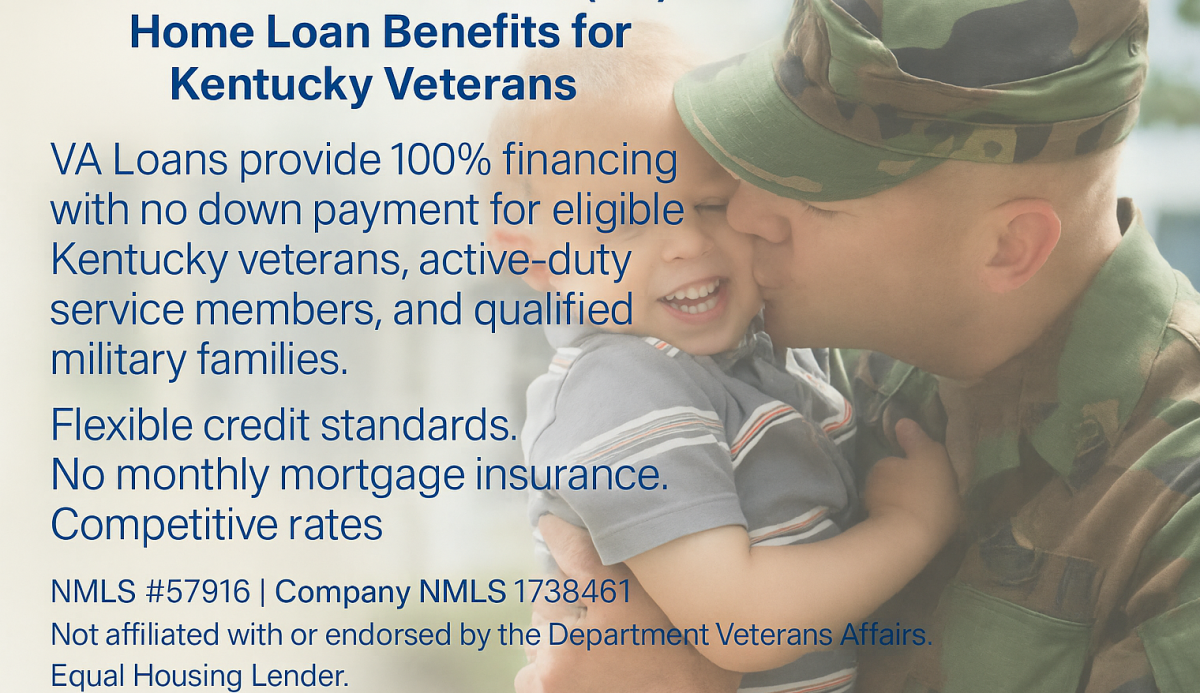

VA loans are federally guaranteed and require NO DOWN PAYMENT!

You can obtain a VA loan through private lenders such as banks, savings & loans, and mortgage companies.

VA offers competitive rates… sometimes the lowest around!

You may purchase any kind of residential property with your VA loan… but, it MUST be your primary residence at the time of purchase and for two years thereafter. You can choose to keep the property for rental purposes if you occupy the property for two consecutive years prior.

Generally speaking, the maximum amount you can borrow for a VA loan is $484,500. There are some “high cost” areas with higher loan limits. Contact a VA rep or your lender for more information.

There is NO PMI (Private Mortgage Insurance) on a VA loan!!! EVER!

There is a cost for using your VA loan. It’s called the VA Funding Fee. The first time you use your VA, the fee is 2.15% of the agreed purchase price, thereafter the fee increases to 3.3%. However, you can decrease the fee after your initial use by putting a down payment on the loan.

There are some individuals who are exempt from paying the VA funding fee. These include any vet receiving compensation for service-related medical issues, and surviving spouses of those who died in service or due to service-related disabilities.

Your VA funding fee CAN be added to your loan balance and factored into your monthly payment. In other words, if you qualify for the entire amount (cost of home + funding fee), you can finance the funding fee.

Allowable closing costs and fees are tightly structured in a VA loan in order to benefit and protect the vet.

It is possible to receive up to 4% in “seller concessions” (money back at closing from the seller) to use for things such as closing costs, payment of funding fee, paying points on the loan to lower the interest rate, etc.

Your lender cannot charge a penalty for early payment of the loan balance.

Have you ever been completely and utterly confused by the various types of financing in a real estate transaction? YES. It can be overwhelming! Here is info on one of the “comeback kids” in the mortgage market… the VA Loan!

During the height of the market, many buyers and sellers neglected the VA loan in large part because of the competitive nature of market at that time. Because we were in a seller’s market then, sellers dictated the types of financing that they would accept… VA was last on the list many times. This was because sellers did not want to pay the sometimes higher costs associated with the loans. Also, VA appraisers are known to be very particular.

During the height of the market, many buyers and sellers neglected the VA loan in large part because of the competitive nature of market at that time. Because we were in a seller’s market then, sellers dictated the types of financing that they would accept… VA was last on the list many times. This was because sellers did not want to pay the sometimes higher costs associated with the loans. Also, VA appraisers are known to be very particular.

Today, with lending standards tightening up, VA loans are making a comeback! Here are some quick facts regarding a VA loan:

- A VA loan is designed for veterans and active duty…

View original post 411 more words

You must be logged in to post a comment.